Maybe your flat is now a little roomy after the children have grown up and moved out, or you’re looking for a place that’s closer to them so you can help take care of the grandchildren. Or perhaps you‘re looking for a change in environment, a new home where you can enjoy your golden years. Whatever the reason, there are housing options, schemes, and grants that seniors can tap on when buying a flat. Here’s a senior’s guide to flat buying:

Housing Options for Seniors

For those looking for a cozy space that’s easy to maintain, you could consider a 2-room Flexi flat. If you and your spouse are aged 55 and above, you can also opt for a shorter lease. You can choose a lease of between 15 and 45 years in 5-year increments, as long as it covers you and your spouse up to the age of at least 95 years. The price of the flat will also be adjusted based on the lease chosen.

These senior-friendly short-lease flats come installed with grab bars. You can also opt for additional senior-friendly fittings in the flat under the Optional Components Scheme (OCS). These include built-in kitchen cabinets with induction hobs and cooker hood, kitchen sink, and a built-in wardrobe.

Schemes and Grants

Seniors can also tap on schemes and grants either to help improve their chances of being balloted for a new flat during sales exercises or to help finance the flat purchase.

If you are selling your current flat and buying a 3-room or smaller flat, you may be eligible for the Silver Housing Bonus. If eligible, you could receive a cash bonus of up to $30,000 when you top-up your CPF Retirement Account (RA) with your sales proceeds and join CPF LIFE, CPF’s life annuity scheme that provides monthly payouts for as long as you live.

If you’re buying a new flat, you may also qualify for one of our Priority Schemes, which improve your chances when balloting for a flat. If you are buying a new flat near your married children, you may qualify for the Married Child Priority Scheme. If you’re looking specifically to buy a 2-room Flexi flat that is either near your current flat to age-in-place in a familiar environment or near your married child, you may qualify for theSeniors Priority Scheme.

If you’re buying a resale flat near your children, you may qualify for theProximity Housing Grantof $20,000.

From housing options designed with your needs in mind, to schemes and grants to help in your flat buying journey, there is plenty of support for seniors when buying a flat.

Thinking of buying a resale flat, but not sure what to look out for? Here are the 3Ls to consider when looking at potential resale flats – location, lease and layout.

1. Location

One of the advantages of purchasing a resale flat is the variety of HDB flats available on the open market. How then do you choose the location that suits you best?

For a start, it might be useful to think about what is important to you and your lifestyle. If you love being close to nature, you might want to look for a flat located near a park, for instance. If you have school-going kids, you may need to check out nearby schools. If living near your parents or in-laws is important, consider looking at resale flats near them. For this, you may also want to check if your potential home would qualify you for a Proximity Housing Grant.

Transport options are also important to consider. While living near an interchange, main road or major transport node would bring convenience, fringe neighbourhoods provide respite from the hustle and bustle.

2. Lease Length

Unlike BTO flats, resale flats sold on the open market come with varied leases. This is important to consider since the length of lease remaining on the flat would impact the amount of CPF money you can tap on to finance your flat purchase. It can also impact the Enhanced Housing Grant amount you can enjoy (if eligible). Both the CPF usage limit and the grant amount will be pro-rated based on the extent the remaining lease of the flat can cover the youngest buyer up to the age of 95.

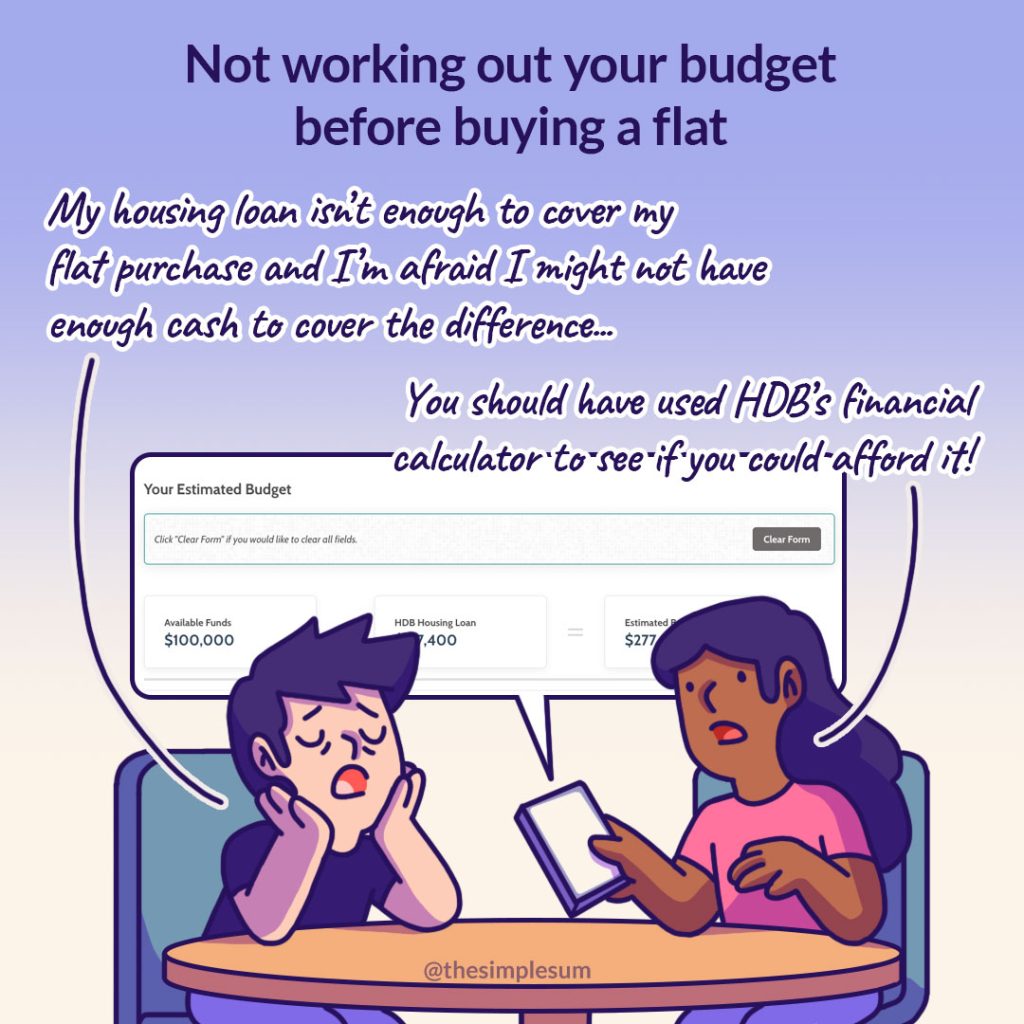

Don’t worry if that sounds like too much math for you – the budget calculator on the HDB Flat Portal is a great resource to consider when purchasing a resale flat.

3. Layout

Finally, resale flats come in a variety of layouts, so it can be daunting to evaluate all the options. Again, ask yourself – what fits your lifestyle? If you’re a family with kids, you may prefer a bigger flat, but if you’re a senior looking for a comfortable place to retire, consider cosy spaces that are easier to maintain.

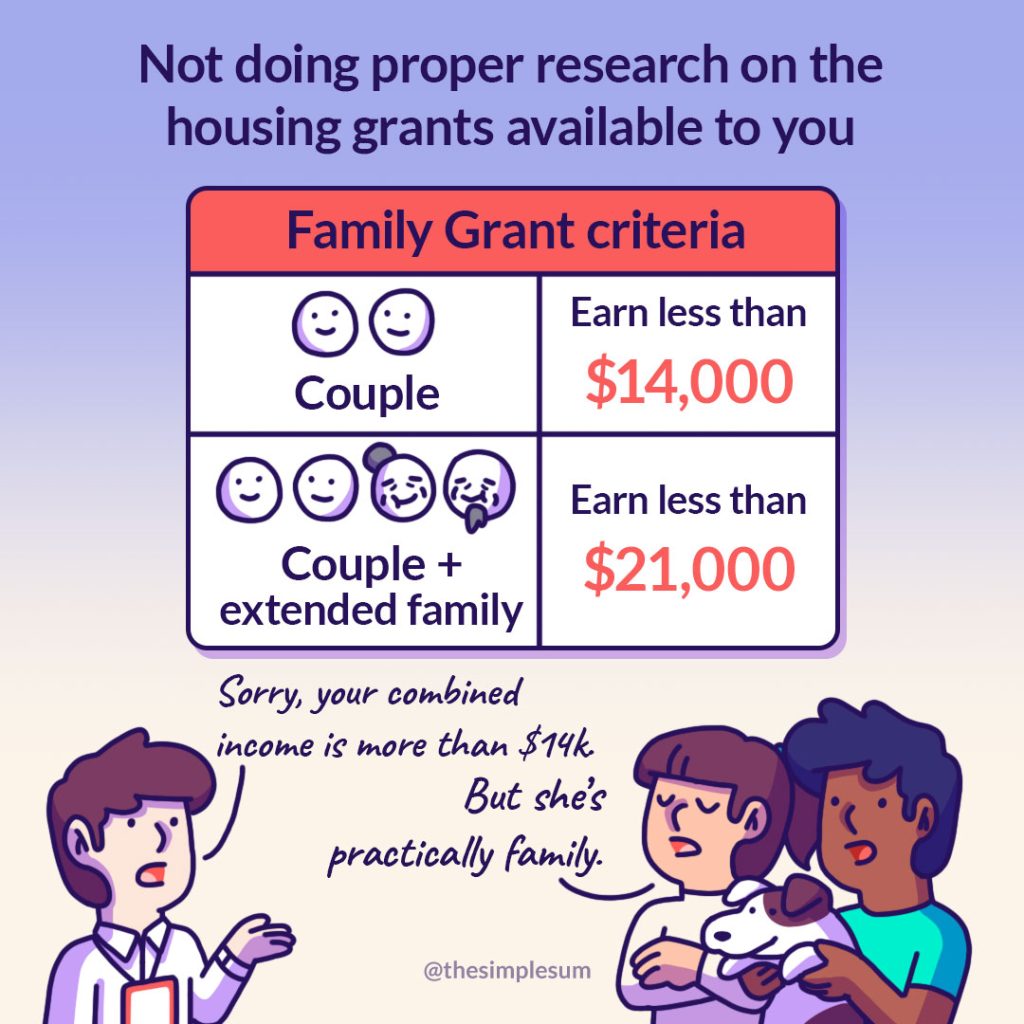

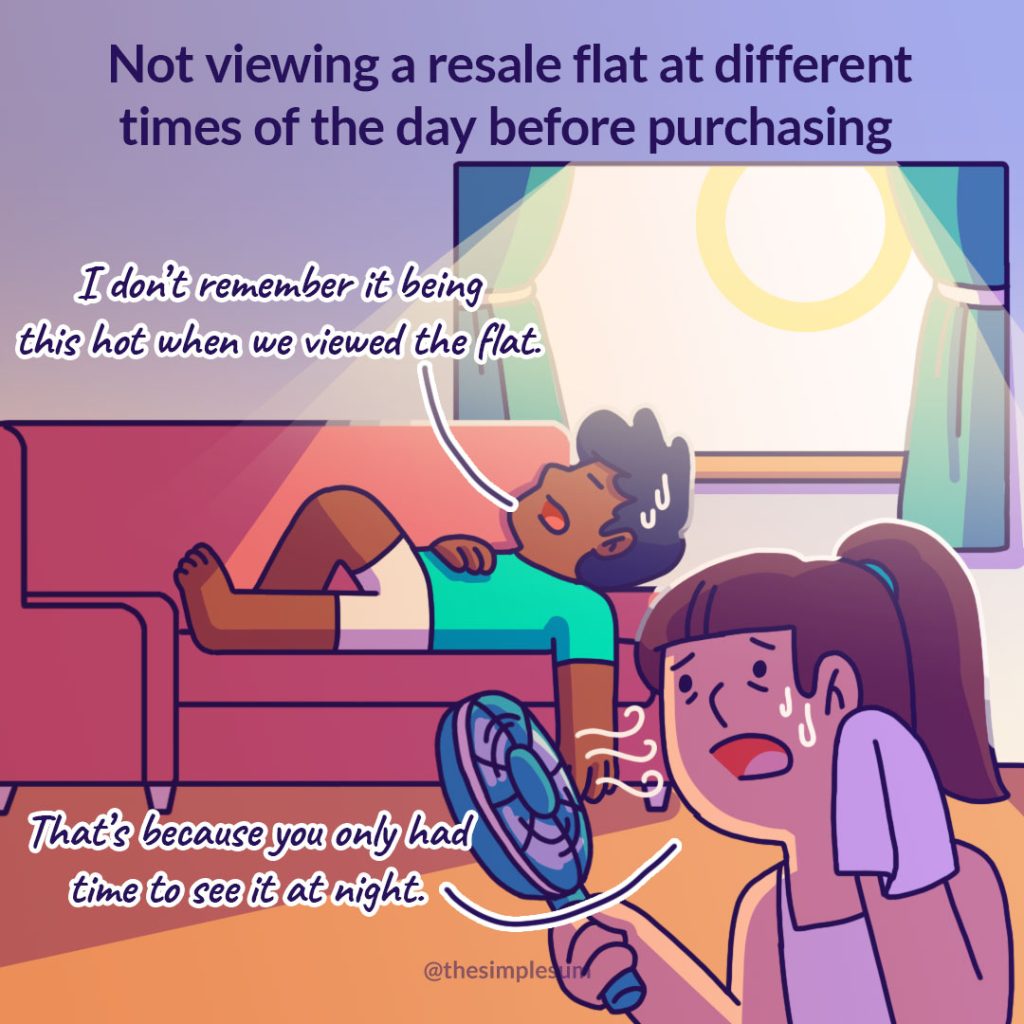

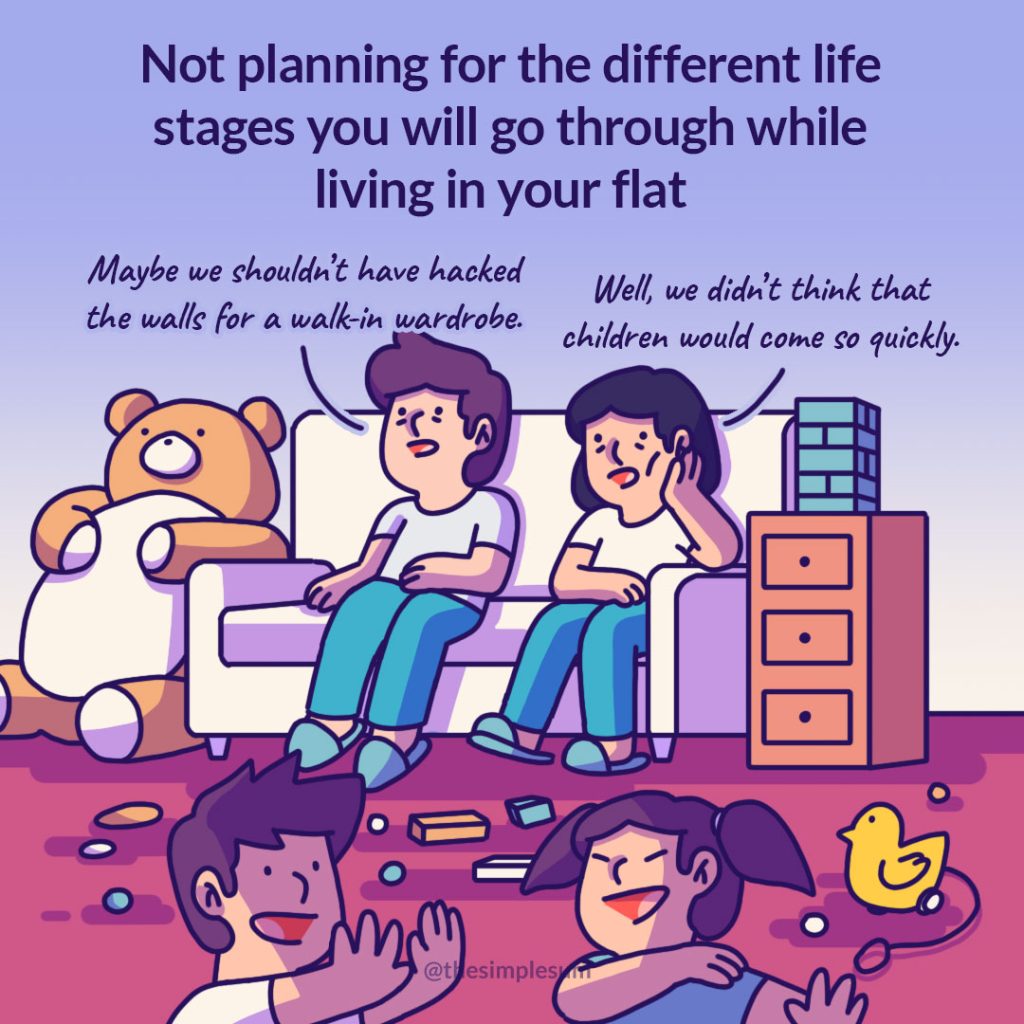

Financing Pitfalls to Avoid When Making Your First HDB Flat Purchase

Did you know that eligible first-timers can enjoy housing grants of up to $80,000 for a BTO flat and $160,000 for a resale flat? From working out a budget beforehand, to researching on the available housing grants, here are some tips from The Simple Sum for purchasing your HDB flat.

Home Tours: Heritage Home with a Contemporary Twist

With its local-inspired décor, Peranakan accents and mid-century modern furnishings, Ridzwan and Nadiah’s BTO flat in Kallang is reminiscent of a shophouse – but with a contemporary touch.

Purchasing Their First Home

“We opted for a 3-room flat as we wanted to be comfortable in terms of the space and budget,” Nadiah explains. “We applied for housing grants and made the downpayment with our CPF. This freed up our cash savings for other home-related costs such as renovation works and furnishings.”

Home owners Nadiah and Ridzwan

“Our home reflects our modern take on a heritage shophouse – perfect for old souls,” laughs Ridzwan.

A Personality-Driven Home

Ridzwan and Nadiah wanted the space to incorporate their lifestyles and personalities. In the living room for instance, the couple demarcated a space for their book collection. “Both Nadiah and I love reading – one of the first things we talked about when we met was our shared love for Enid Blyton books when we were children,” Ridzwan smiles.

In addition to their book collection, the feature shelf also houses the couple’s collection of trinkets, including a vintage clock and tingkats. Family heirlooms such as a typewriter and sewing machine also double as home décor, adding to the nostalgic vibes that carry throughout the space.

The patterns of the semi partition are reminiscent of Peranakan-inspired prints

When asked to describe the overall look and feel of their home, Ridzwan says, “It’s a combination of mid-century modern and influences from local heritage – in a way, our home design is our classy take on a traditional Singapore shophouse.”

Space Planning

One of the home owners’ priorities is to have a flexible space that can adapt to their changing lifestyle needs.

For example, a sliding glass door replaces the wall between one of the bedrooms and the living room, resulting in a semi-open space. While the space is currently being used as the dining area and (?) Ridzwan’s home office, the room can be converted into a nursery once the couple starts a family.

The kitchen and service yard were combined to accommodate an extended kitchen counter.

“We enjoy cooking together, so we wanted a spacious layout that allows us to move about freely as we do so,” says Nadiah. “We love how we could also fit a full-sized pantry while allowing sufficient space for our laundry area.”

The black and white mosaic floor tiles in the kitchen are also found in the common bathroom The porcelain sink is a statement piece that the couple chanced upon online

One uncommon feature is that the couple did away with a wardrobe in the bedroom. On this decision, Nadia explains, “We wanted to place a vanity table, which is a family heirloom, in the bedroom instead. We figured that having a storage bed and large cabinets in the common areas will meet our storage needs.”

The retro look of the customised rattan headboard perfectly complements the overall aesthetics of the flat

In the en suite, the sink was relocated to the right side of the bathroom, to accommodate an L-shaped counter. “With the fixtures and fittings flushed to the right, the space feels bigger.”

Similar to the common bathroom, black and white mosaic tiles were chosen for the en suite while jade green subway wall tiles are used to add a pop of colour

“With the current work-from-home arrangement, we have come to appreciate our home a lot more,” the couple laughs. “We usually work in the dining area, so during lunch time, we’d prepare and have our meals and get back to work. In the evenings, the communal area will be transformed to an exercise area for our workouts. We’re really happy with how our home is perfect for both work and play.”

The article was adapted from a version first published on Qanvast.

My Resale Flat Journey: First Property is 30-Year Old Resale Flat

Thinking of buying a resale flat? Read about how Mr Wong found the right unit for him and his family!

The post ‘My Resale Journey: First Property is a 30-Year Old Resale Flat’ appeared first on the MoneySmart blog

Mr Wong, 32, and his wife, Madam Lai, 31, are on the cusp of moving into a resale flat in Jurong West with their child, as well as Madam Lai’s brother and sister-in-law.

The couple’s 5-room flat has just been renovated, and they are now putting the finishing touches to their new home.

In this second part of a 3-part series in which we present the stories of resale flat buyers, we spoke with Mr Wong on his new home and the process he went through to purchase his resale flat.

About The Flat

Owner: Mr Wong Bin Hao, 32, married with 1 kid

Location

Jurong West

Flat Price

$335,000 (after $40,000 housing grants)

Year of Purchase

2018

Flat Type & Size

5-room flat/ 121 sqm

Remaining Length of Lease

69 years (as of May 2019)

Monthly Mortgage Amount & Loan Tenure

About $1,600

18 years

Renovation Cost

About $35,000

When we visited Mr Wong’s flat at Jurong West Avenue 5, workmen were finishing up their final renovations.

But the flat already looked cosy and inviting, with a comfy couch and a pile of Hello Kitty cushions beckoning us as we entered.

MoneySmart (MS): Mr Wong, how did you and your wife decide to buy a flat in Jurong West?

My wife and I both work in the Jurong area. For a period of time, we rented in nearby neighbourhoods and moved around.

I have been living in Jurong West for about three to four years. I’ve always found this area quite lively and naturally, wanted to buy a home here.

MS: Besides the fact that it’s lively, what else about this place appealed to you?

My two-year-old kid goes to the childcare centre in this block. You can also see the playground from here so it’s perfect and convenient for us. There are some primary schools close by that my child can attend in the future.

There are also two malls nearby, Pioneer Mall and Gek Poh. When the future Jurong Region Line is up, we will be within walking distance to an MRT station, so I think it was worth the buy.

MS: You started out renting a flat. What made you decide to take the plunge and buy your own place?

For me, having that sense of ownership is important.

When you rent, you might need to move from time to time, like what happened to us in the past. I found it tiring to be moving from house to house every year or so.

Some landlords are also not prepared to accept tenants who keep different hours or lifestyles. At the start they may say everything is okay, then suddenly they become fussy and impose curfews on the tenants.

There are uncertainties when you rent a place with friends too – they may need to move elsewhere and you will need to find another flat mate.

When I rented a place, I had to pay the landlord rent in cash every month, and could not make use of my CPF savings. Now, I can pay my housing loan instalments using CPF, so I don’t really need to fork out cash. For all these reasons, I feel it is good to have my own flat.

MS: We understand that your flat is about 30 years old. Was its age a concern for you?

One reason why I bought a resale flat is that it is more spacious for my family. This flat is about 120 sqm and the kids have more space to run around. Sometimes my parents or my wife’s parents will visit. So it’s better to have more space.

We still have 69 years left on the lease which is good enough for us. Our children and future generations are likely to buy their own homes anyway, so we don’t need to worry about leaving this flat for them. As we are planning to use this flat as a home, I think it’s good enough. For the next generation, you don’t need to bother as the kids will buy their own homes.

Although this is an old estate, the area is well taken care of by the Town Council and HDB also carries out upgrading of the flats.

MoneySmart Tip: Use this online map service to get lease information, resale prices, and even season parking information for each housing block. You can filter through nearby amenities to see where to dine and shop.

MS: Do you see your flat as an investment?

When we were weighing the pros and cons of buying a 30-year-old flat compared to a newer one, we did think about this issue. However, we feel that a house is for the long-term and one that would see us through our old age. Instead of hoping to make a profit from moving houses, we would rather stay in one flat and finish paying our housing loan sooner, so that we can free up our finances for other things.

MS: How was the purchase process? Did you go through an agent or DIY?

We initially tried to DIY by using a property website, but later on we received calls from estate agents offering their services and we engaged an agent eventually. He asked us what sort of attributes we wanted in a flat, and helped us to look for suitable flats that were within our budget.

Everyone has different interests and needs, so it’s important to know what your own needs are, before you decide whether to engage an estate agent for your resale transaction.

MoneySmart Tip: We asked Mr Wong if he knows about HDB’s Resale Portal, and he says he doesn’t. The HDB Resale Portal could have guided him in the buying journey. It takes buyers and sellers through the buying and selling process in a step-by-step manner online and allows them to DIY their transaction if they choose not to engage an estate agent.

MS: How is your flat being financed?

We went for an HDB loan as we found it less complicated than going for a bank loan. For bank loans, the interest rate is a bit uncertain.

Although the HDB loan interest rate is currently higher than for bank loans, the difference is not that much after you do the math.

Initially we indicated that we wanted to settle the loan in 10 years. Then HDB called us to ask whether we wanted to reconsider. Based on our salary, they recommended an 18-year loan tenure so that we can buffer for things like employment changes or if we suddenly need cash for urgent reasons. They explained that we can make partial capital repayment or even redeem the loan earlier if our finances permit. We found the advice useful. My wife and I are planning to settle the loan earlier to incur less interest and save more for retirement.

MoneySmart Tip: Find out how you can make partial capital repayment or fully redeem your HDB loan and save on housing loan interest.

MS: Did you get to enjoy any grant?

We got the housing grant for first-time buyers, which was a really attractive sum. We initially set aside a bigger budget as we thought we would not be eligible for grants. So for us, getting the grant was a bonus.

We spent about $35,000 on renovations, mainly for works in the kitchen and for furnishings around the house. This includes $16,000 paid to our contractor, who was flexible to work with.

We did not hire interior design firms as we found their prices quite high. Since we wanted to save money, we thought it was better to work directly with contractors. For example, the rewiring cost quoted by the contractor was cheaper than market rate!

MS: Any advice for aspiring homebuyers?

You don’t really need to look for flats with fanciful fittings, because you will probably have to do your own renovations anyway. For example, even if the flat comes with nice flooring, the colour of the tiles may be uneven after the previous flat owner has removed all their furniture. So you might still need to replace the floor tiles.

MoneySmartTip: Planning your renovations for your HDB flat? Know what’s important to note and familiarise yourself with the guidelines.

Mr Ismail shares his experience of moving from one resale flat to another!

The post ‘My Resale Journey From West to East’ appeared first on the MoneySmart blog

This article was updated on 25 May 2021.

Conversations around public housing usually revolve around affordability, value, and financing. Beyond the dollars and cents, it’s hard to get a tangible sense of what owning a flat means to people, and the significance of having a home to call their own.

We spoke to different homeowners, specifically those who had bought resale flats, to get their thoughts about their home and flat buying journey. In the first of our 3-part series, we speak to Mr Ismail, who has lived on both sides of the island.

About The Flat

Owner: Mr Ismail bin Hamid, 41, Married with 4 kids

Location

Tampines

Flat Price

$410,000 (after $20,000 Proximity Housing Grant)

Year of Purchase

2018

Flat Type & Size

4-room flat/ 104 sqm

Remaining Length of Lease

63 years (as of Apr 2019)

Monthly mortgage amount & loan tenure

Nil (fully paid after selling previous flat)

Monthly mortgage amount & loan tenure

About $38,000

MoneySmart (MS): Mr Ismail, this is an amazing looking house. Tell us a little bit about why you chose to buy a flat here.

Mr Ismail: Tampines has been my home for the past 7 years. This flat is located 2 blocks away from where I grew up in, so this is a neighbourhood I am very familiar with. In fact, one of my primary school classmates still lives in the next block with his own family!

When I was growing up, there was only Bedok Interchange. There was no Tampines Interchange, and the Downtown Line certainly didn’t exist at that time, so you can imagine that getting around was very different from how it is now.

MS: Tell us a bit about your housing journey.

Mr Ismail: After I got married, my wife and I moved to Bukit Batok, which was near her family. It was a very different area from where I grew up, so that was something new. We then moved to a resale flat in Bukit Panjang. With convenience and proximity to family being a key consideration, we decided not to wait for a suitable BTO flat. At that time, the only available BTO flats were in Sengkang and Punggol, so we chose to buy a resale flat.

Due to family circumstances, we eventually moved back to the East, a few streets away from where we are currently staying now.

MoneySmart Tip: Interested flat buyers can get information on upcoming BTO projects 3 months before sales exercises for better planning. In the meantime, you can visit HDB InfoWEB for details on the upcoming BTO sales exercise.

MS: We also understand that you moved from a 5-room to a 4-room flat?

Mr Ismail: We felt that it was a much better idea to move to a 4-room flat because there was a lot of unused space in our previous 5-room flat. Even though we have four kids (aged 12, 9, 8, and 3), we felt that this current place suits our needs perfectly.

As you can see, the amenities around this place are great for our kids. We also considered the fact that there was a park that was very accessible and our kids wouldn’t have to cross any major roads to get there.

At this point, Mr Ismail’s wife also chimes in, highlighting the fact that the 4-room flat is much easier to clean than their previous home. They also managed to completely pay off their housing loan after moving, but more on that later.

MS: Tell us about your home buying process. Did you engage an agent or do it on your own?

Mr Ismail: We decided to go with an agent, and the reason was that our housing agent was also my friend from reservist! He also helped us to sell our previous home. I would say when it comes to engaging an agent, it definitely helps to have someone who knows his stuff.

It was an easy decision to buy our current home because we knew what we wanted, and the opportunity presented itself. I would say our only regret is that we missed out on a flat that is near the newly built Our Tampines Hub. There was nothing there at that point in time and we had no idea they were going to build an integrated community hub there!

MoneySmart Tip: Besides going through an agent, buyers and sellers can use the HDB Resale Portal to perform their own resale transactions. The portal will guide you on the buying journey and help you track the progress of your transaction. The resale process takes approximately 8 weeks to complete from the date of HDB’s acceptance of the resale application.

MS: How did you plan your finances? What were your goals or considerations?

Mr Ismail: For me, I chose to pay off this flat fully. I know it might seem a little “old school”, but we believe that we should just keep our money in CPF and use that for retirement.

For our previous homes, we also chose to take a loan from HDB. My wife works in a bank, so we understand that there are benefits and risks to taking a bank loan, and we ultimately settled on getting an HDB loan. Now that we’ve paid off this flat, we don’t have to worry about a mortgage anymore, and we can focus on planning for retirement.

MS: And what sort of grants did you get for your home?

Mr Ismail: At the start when we got our first place after we got married, we were eligible for a grant for first time buyers, and of course we were aware that we could get $20,000 in Proximity Housing Grant for this flat as we were moving near my parents.

MS: Your home looks really nice and comfortable. Did you have to renovate it a lot, and how much did you spend?

Mr Ismail: We spent about $38,000 on our renovations. We did have to do quite a bit of work, which included your regular maintenance such as repainting the place and redoing the flooring and doors. The main issue with the place was that the wiring wasn’t done properly so we had to redo everything because they were crossed all over the place. The kitchen was also rather old so we gave it a refresh.

MS: Can you share with us some thoughts around owning a home in Singapore?

Mr Ismail: For me, I never intended to buy a flat to profit from it. I plan to stay here with my wife till we pass on. Some people talk about leases expiring, but my perspective is that you are probably not even going to be alive when that lease expires, so why worry about it? As for my children, they will probably move out and buy a flat of their own, so I am not too worried about what happens with the lease.

There are many things that might change in the future which you have no idea about, so you plan for what you can. Other than that, I feel blessed to be able to say that I own a home, which is more than what many other people in other developed countries can say.

MS: Any other words of advice for homebuyers?

Mr Ismail: Go with what you are comfortable with. At the end of the day, you can overthink, but when you step into a neighbourhood, just ask yourself whether you feel like you belong there . Are you comfortable with the place and its surroundings? Is it a place you feel your children can grow up in?

Convenience is another factor. It might be more important for you to be near a supermarket than an MRT station. Whatever the case, understanding your needs is important. Small inconveniences can become a big deal over the course of a few years.

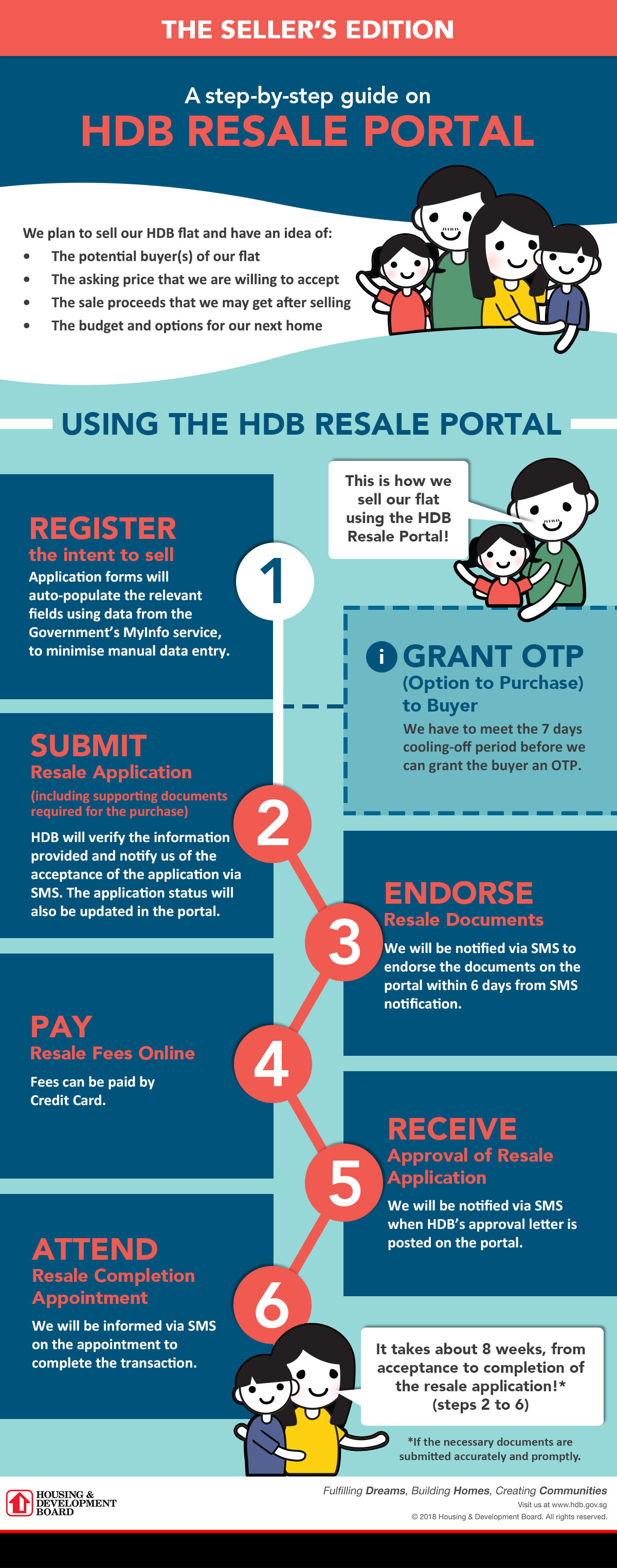

Buying or selling an HDB resale flat? Find out how to use the Resale Portal!

HDB resale flat buyers and sellers can now use the new HDB Resale Portal, launched on 1 January 2018.

The HDB Resale Portal streamlines all the resale of flats processes into a single platform, and provides a step-by-step guide for flat buyers and sellers throughout the resale transaction.

Using the HDB Resale Portal will benefit you in many ways:

– Shortens resale transaction time by up to 8 weeks

– Reduces manual entry of personal information

– Integrates all resale-related services

– Reduces number of appointments with HDB (Only 1 appointment required!)

With this portal, you can get instant results on your eligibility to buy a flat, housing grants, and HDB concessionary housing loan. Other important information, such as the Ethnic Integration Policy quota, upgrading status, upgrading costs billing status, and recent resale flat transactions nearby, have also been included in the HDB Resale Portal.

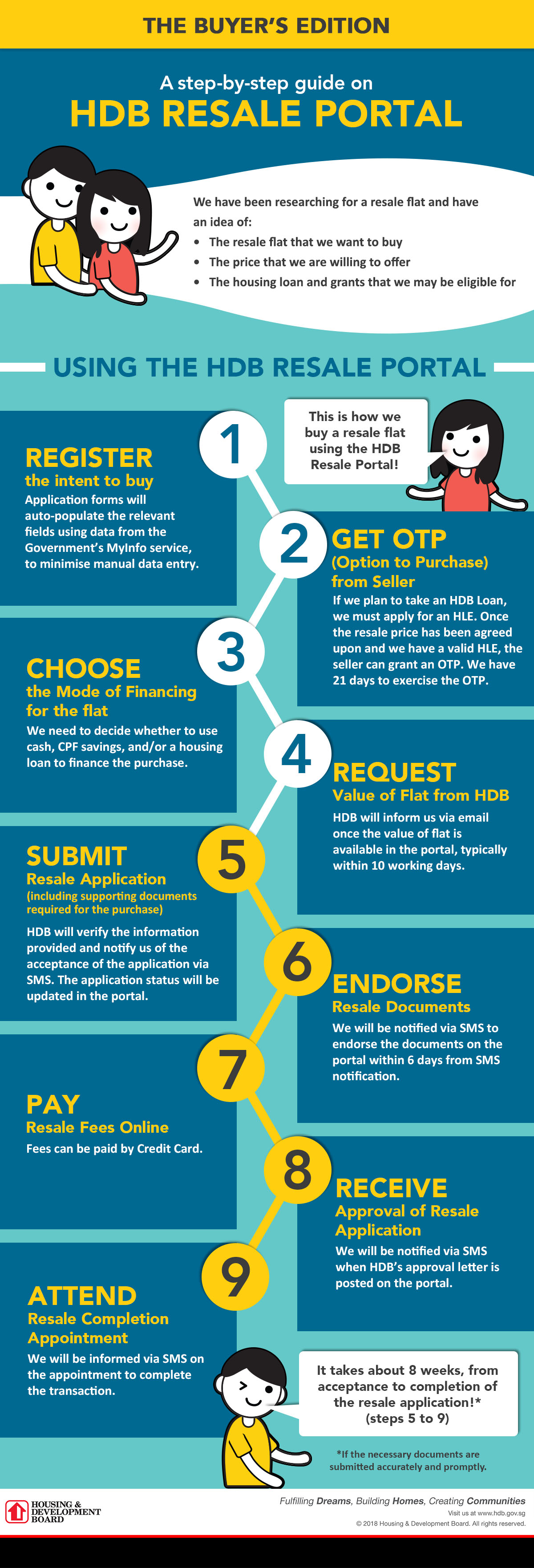

Here are the key steps to guide you in using the resale portal.

1. Register intent to buy/ sell

You must first register your intent to buy or sell a flat on the HDB Resale Portal. Your personal particulars will be automatically retrieved and populated from the Government’s MyInfo service.

2. Search for a flat and get an Option to Purchase (OTP)

Once you have found a resale flat within your budget, you will need to obtain an OTP from the seller. You have 21 days to exercise the OTP.

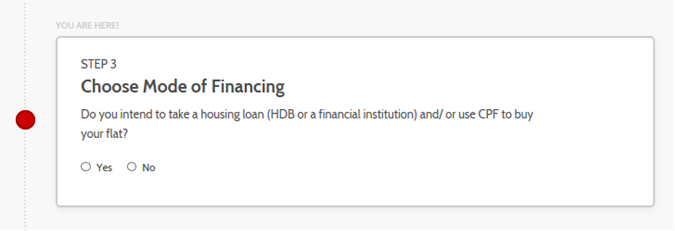

3. Choose the mode of financing

As a flat buyer, you will need to decide how you intend to finance the flat purchase. You can either use cash, CPF savings, or obtain a housing loan. If you wish to obtain an HDB housing loan, the HDB Resale Portal will guide you to apply for an HDB Eligibility Letter.

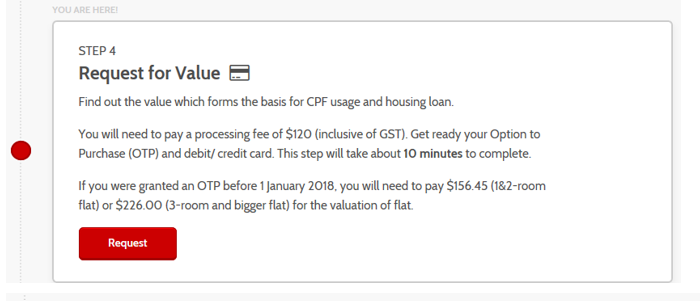

4. Request value of flat from HDB

If you are financing the flat purchase with your CPF savings and/or housing loan, you are required to submit a request to HDB to confirm the loan quantum and the amount of CPF savings you can use. You will pay HDB a processing fee of $120 (including GST).

Flat buyers can only submit a Request for Valuation after the seller has granted them an OTP. They will need to submit the Page 1 of the OTP and Request for Valuation, to HDB by the next working day after the OTP date.

If HDB requires valuation of the flat to be done, HDB’s appointed valuer will carry out the flat inspection within 3 working days after informing the seller. Flat buyers can check the flat’s valuation in the HDB Resale Portal within 10 working days from the inspection date.

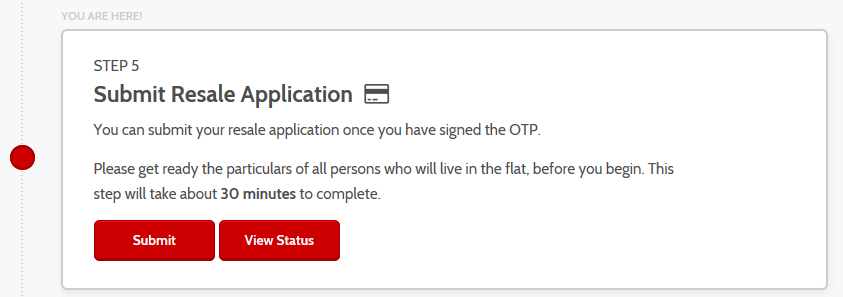

5. Submit resale application

Both flat buyers and sellers must submit their respective portions of the resale application with the supporting documents to the HDB Resale Portal, after the OTP has been exercised. They will need to pay an administrative fee, depending on the flat type.

HDB will verify the information and notify the buyers and sellers of the application outcome, typically within 8 weeks.

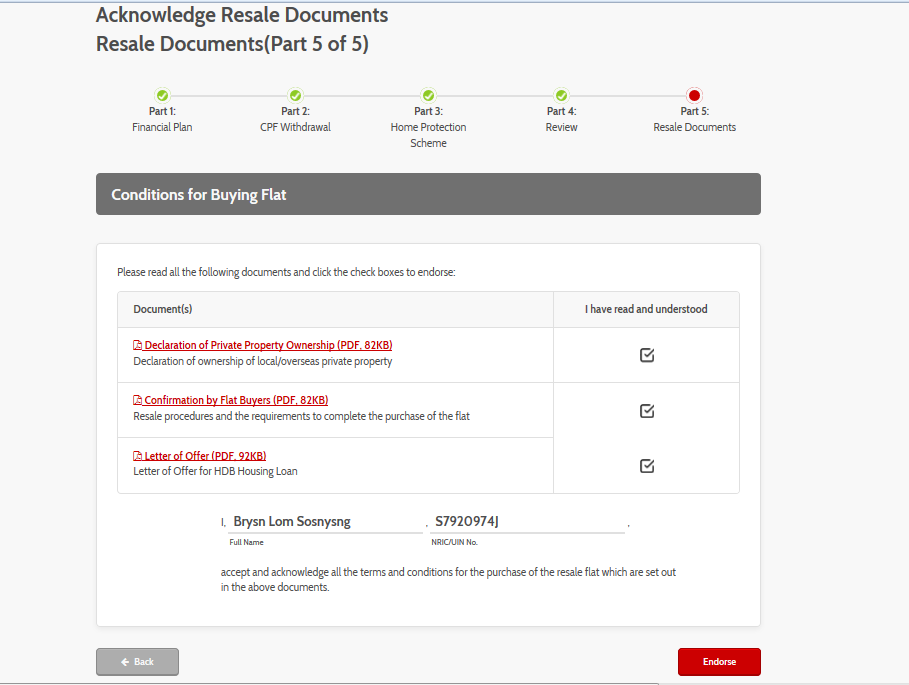

6. Acknowledge resale documents

HDB will compute and prepare the documents for buyers and sellers to endorse in the HDB Resale Portal. Both parties must endorse the documents within 6 days.

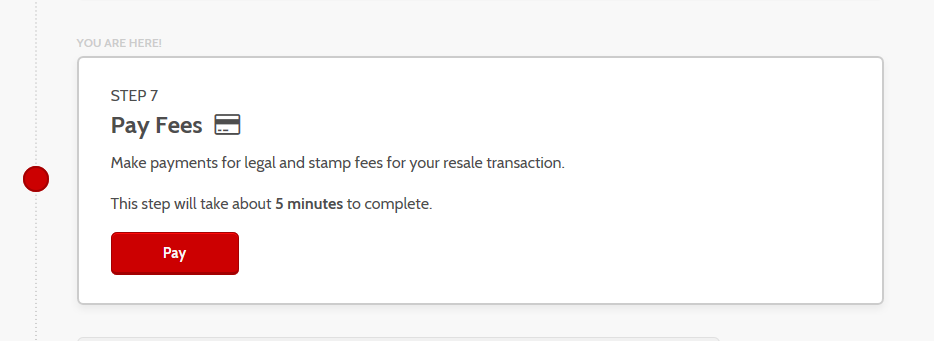

7. Pay resale fee

Flat buyers and sellers are required to pay online for the legal and stamp fees using the HDB Resale Portal.

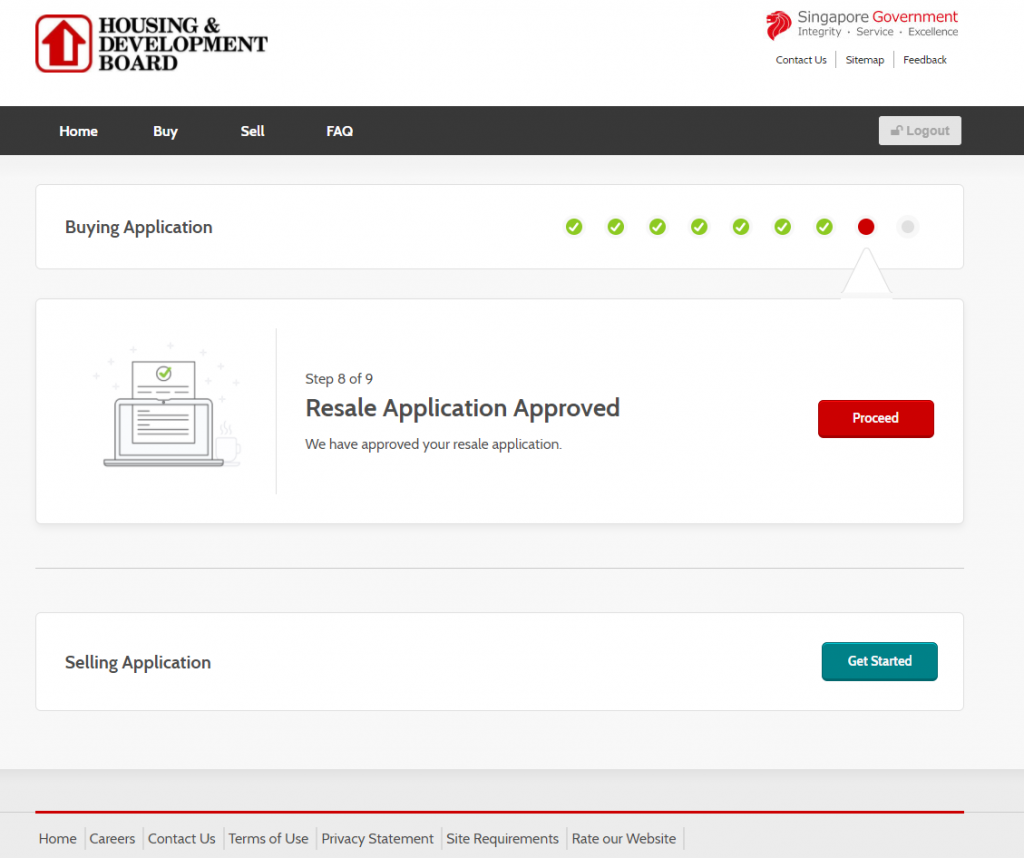

8. Wait for HDB’s approval

HDB will inform flat buyers and sellers once the application has been approved. The approval letter will be available on the HDB Resale Portal.

9. Attend completion appointment

Flats buyers and sellers must attend the Completion Appointment at HDB Hub to complete the resale transaction.

In summary, here are the steps for flat buyers and sellers:

Home Tours: Heritage Home with a Contemporary Twist

Ridzwan and Nadiah’s home in Kallang is reminiscent of a shophouse – but with a modern touch.

With its local-inspired décor, Peranakan accents and mid-century modern furnishings, Ridzwan and Nadiah’s BTO flat in Kallang is reminiscent of a shophouse – but with a contemporary touch.

Purchasing Their First Home

“We opted for a 3-room flat as we wanted to be comfortable in terms of the space and budget,” Nadiah explains. “We applied for housing grants and made the downpayment with our CPF. This freed up our cash savings for other home-related costs such as renovation works and furnishings.”

Home owners Nadiah and Ridzwan

“Our home reflects our modern take on a heritage shophouse – perfect for old souls,” laughs Ridzwan.

A Personality-Driven Home

Ridzwan and Nadiah wanted the space to incorporate their lifestyles and personalities. In the living room for instance, the couple demarcated a space for their book collection. “Both Nadiah and I love reading – one of the first things we talked about when we met was our shared love for Enid Blyton books when we were children,” Ridzwan smiles.

In addition to their book collection, the feature shelf also houses the couple’s collection of trinkets, including a vintage clock and tingkats. Family heirlooms such as a typewriter and sewing machine also double as home décor, adding to the nostalgic vibes that carry throughout the space.

The patterns of the semi partition are reminiscent of Peranakan-inspired prints

When asked to describe the overall look and feel of their home, Ridzwan says, “It’s a combination of mid-century modern and influences from local heritage – in a way, our home design is our classy take on a traditional Singapore shophouse.”

Space Planning

One of the home owners’ priorities is to have a flexible space that can adapt to their changing lifestyle needs.

For example, a sliding glass door replaces the wall between one of the bedrooms and the living room, resulting in a semi-open space. While the space is currently being used as the dining area and (?) Ridzwan’s home office, the room can be converted into a nursery once the couple starts a family.

The kitchen and service yard were combined to accommodate an extended kitchen counter.

“We enjoy cooking together, so we wanted a spacious layout that allows us to move about freely as we do so,” says Nadiah. “We love how we could also fit a full-sized pantry while allowing sufficient space for our laundry area.”

The black and white mosaic floor tiles in the kitchen are also found in the common bathroomThe porcelain sink is a statement piece that the couple chanced upon online

One uncommon feature is that the couple did away with a wardrobe in the bedroom. On this decision, Nadia explains, “We wanted to place a vanity table, which is a family heirloom, in the bedroom instead. We figured that having a storage bed and large cabinets in the common areas will meet our storage needs.”

The retro look of the customised rattan headboard perfectly complements the overall aesthetics of the flat

In the en suite, the sink was relocated to the right side of the bathroom, to accommodate an L-shaped counter. “With the fixtures and fittings flushed to the right, the space feels bigger.”

Similar to the common bathroom, black and white mosaic tiles were chosen for the en suite while jade green subway wall tiles are used to add a pop of colour

“With the current work-from-home arrangement, we have come to appreciate our home a lot more,” the couple laughs. “We usually work in the dining area, so during lunch time, we’d prepare and have our meals and get back to work. In the evenings, the communal area will be transformed to an exercise area for our workouts. We’re really happy with how our home is perfect for both work and play.”