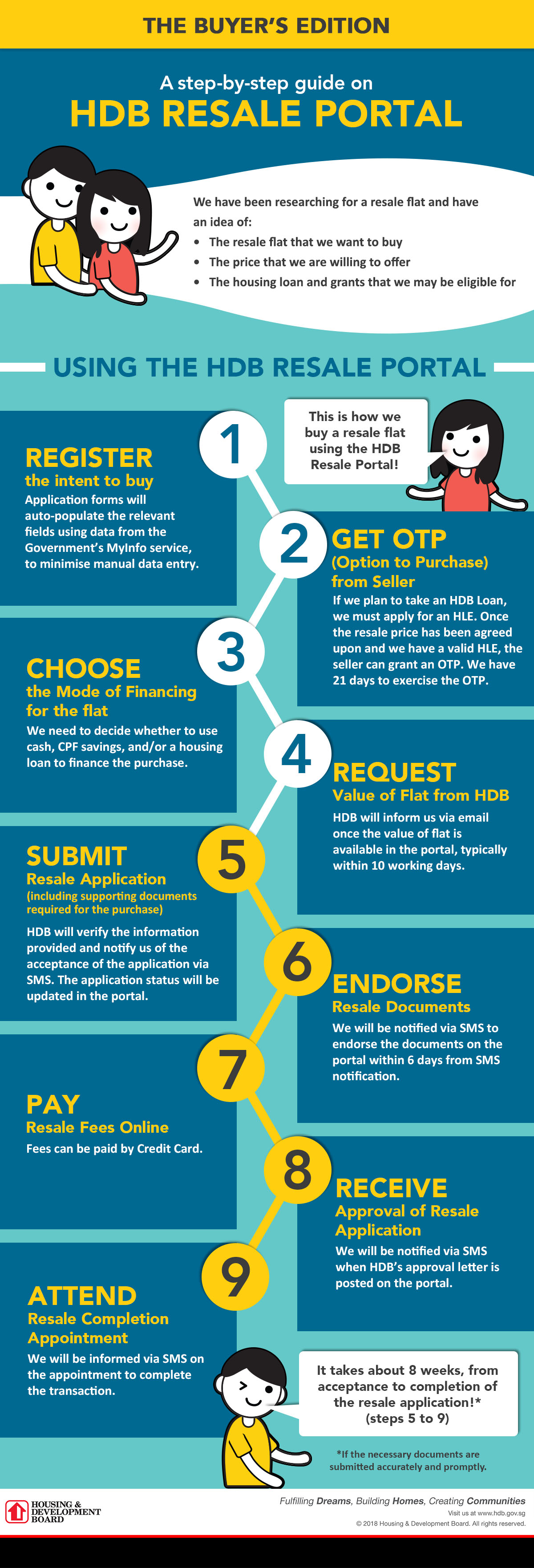

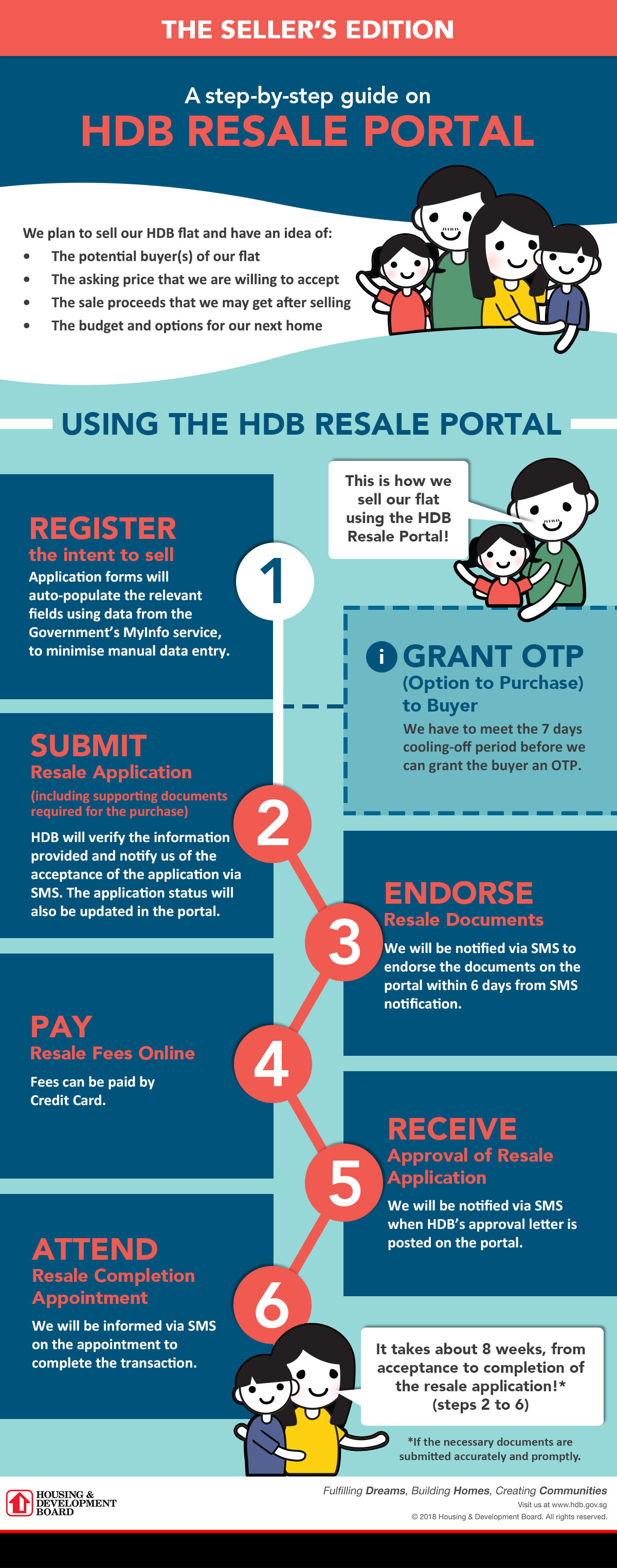

Selling a flat? Here’s what you need to know about the HDB Resale Portal.

The HDB Resale Portal was created to streamline the process of buying and selling resale flats. With eligibility checks and other processes integrated into the same portal, home owners can even sell their flat on their own, without a salesperson.

1. Get Your Home Ready

Selling your home may be unfamiliar to you, but we’re here to help! Check out our tips to make your flat selling journey as smooth as possible.

2. Register Intent to Sell at the HDB Resale Portal

Once you have confirmed with your flat buyer on the sale, and have mutually agreed on the selling price, you need to get the formal process started by registering your intent to sell on the HDB Resale Portal.

With the handy SingPass Mobile App, signing in is a breeze. By scanning a QR Code during the login process, your personal information from the Government’s MyInfo service will be automatically and securely populated into the HDB Resale Portal.

When you register the intent to sell, the HDB Resale Portal will also obtain information about your flat to help facilitate the sale – these include whether you have fulfilled the Minimum Occupation Period, and the Ethnic Integration Policy (EIP) quota prescribed to your precinct and neighbourhood.

The next step is to wait for 7 days – the cooling-off period – before you can proceed further. Take this time to exchange information with your buyer for the Option to Purchase (OTP). You can download the OTP form from the HDB Resale Portal (or HDB InfoWEB beforehand) to understand the terms and get started on the sections that you will need to fill in.

The OTP is a contractual document used for HDB resale transactions. Under the Housing and Development Act, sellers (and buyers) must use the Option to Purchase for any sale or purchase of flats. No gentlemen’s agreement or special handshake allowed!

3. Grant The OTP

After 7 days, you can sign on the completed OTP form and grant it to your buyer. You and your buyer will also need to agree on the Option Fee (a sum between $1 to $1,000) which will be paid to you and acts as a “deposit” for the OTP.

The Option you’ve granted to the buyer is valid for 21 calendar days and expires at 4pm on the 21st day. During this period, you will not be able to grant the Option to another buyer. Even if your buyer decides not to exercise the Option, you will need to wait for the Option to expire. In such situations, the buyer will forfeit the Option Fee.

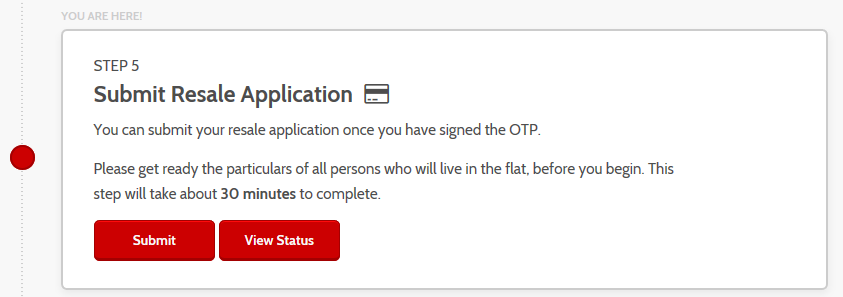

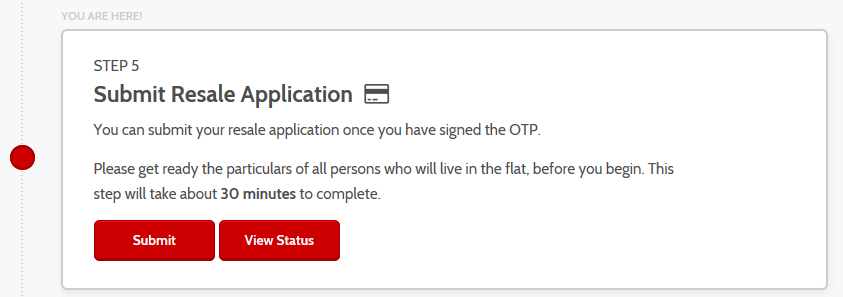

4. Submit Resale Application and Documents

Once your buyer has signed the OTP, you will need to log into the HDB Resale Portal and submit the resale application along with supporting documents. HDB will verify the information and notify you and your buyer of the application outcome within 8 weeks.

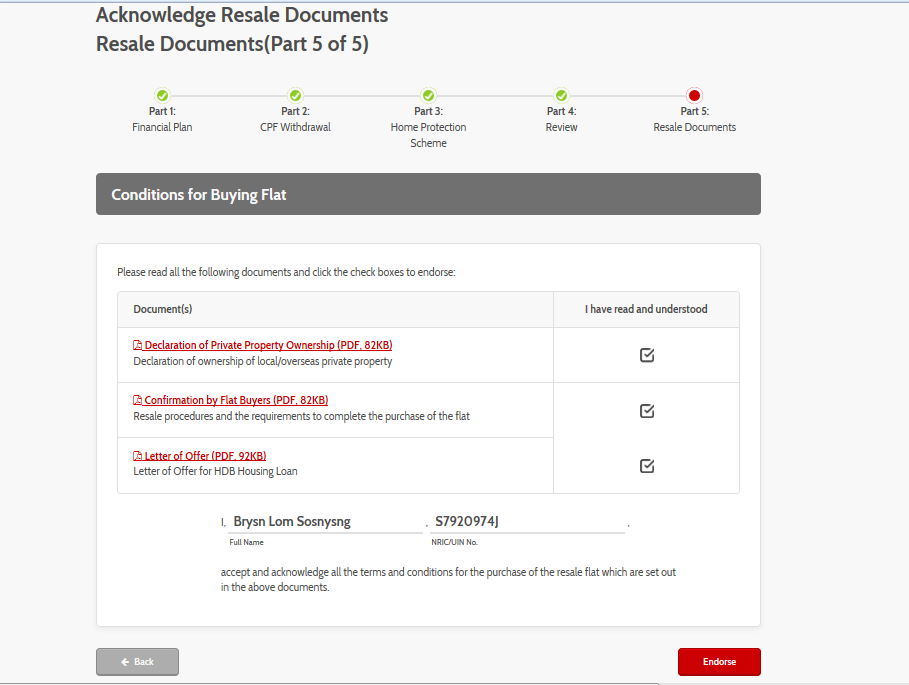

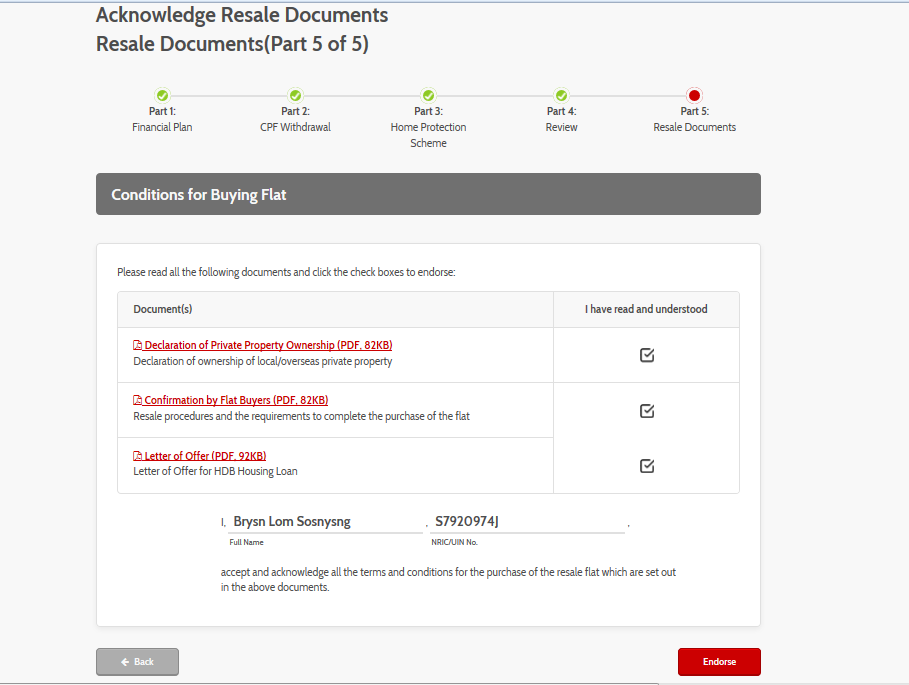

5. Endorse Resale Documents

After submitting the documents, both you and your buyer will be notified via SMS to endorse the documents on the HDB Resale Portal within 6 days.

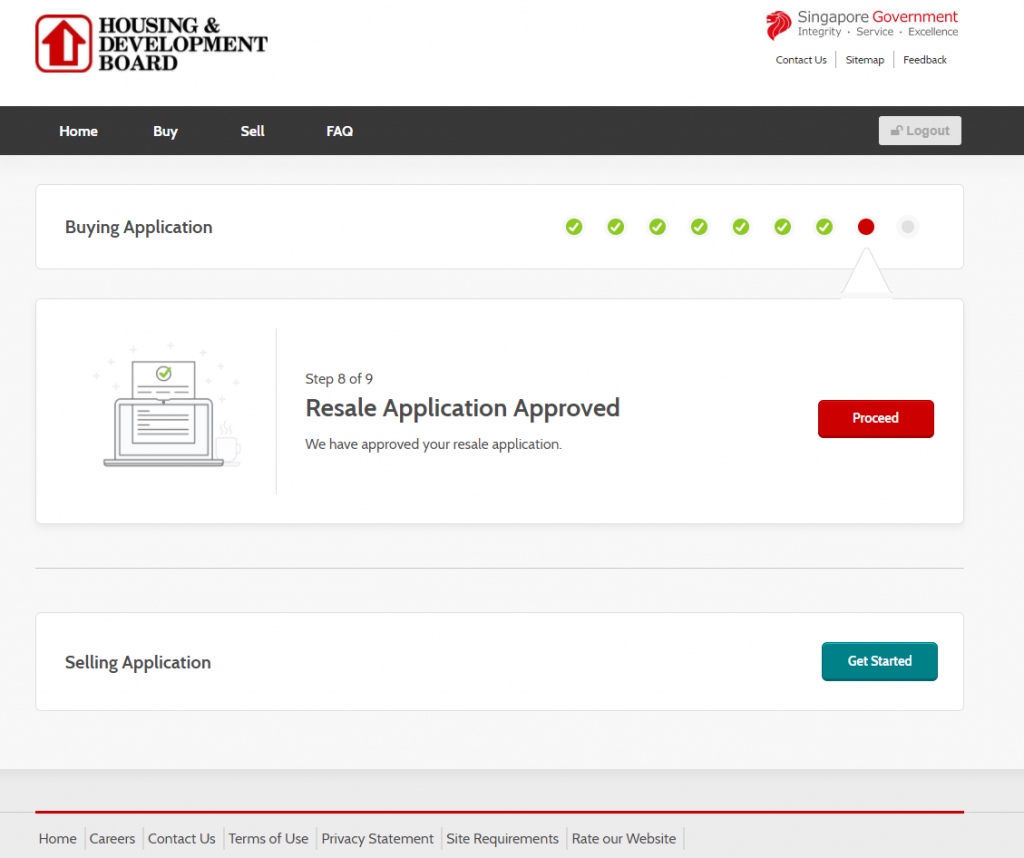

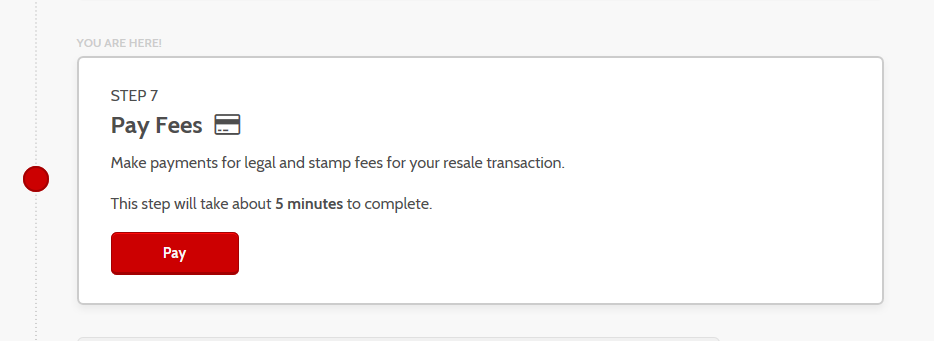

6. Pay Resale Fees and Wait for HDB’s Approval

Once the documents are endorsed by both parties, you can move onto paying the legal and stamp fees for the flat resale transaction. Credit or debit card payments are accepted.

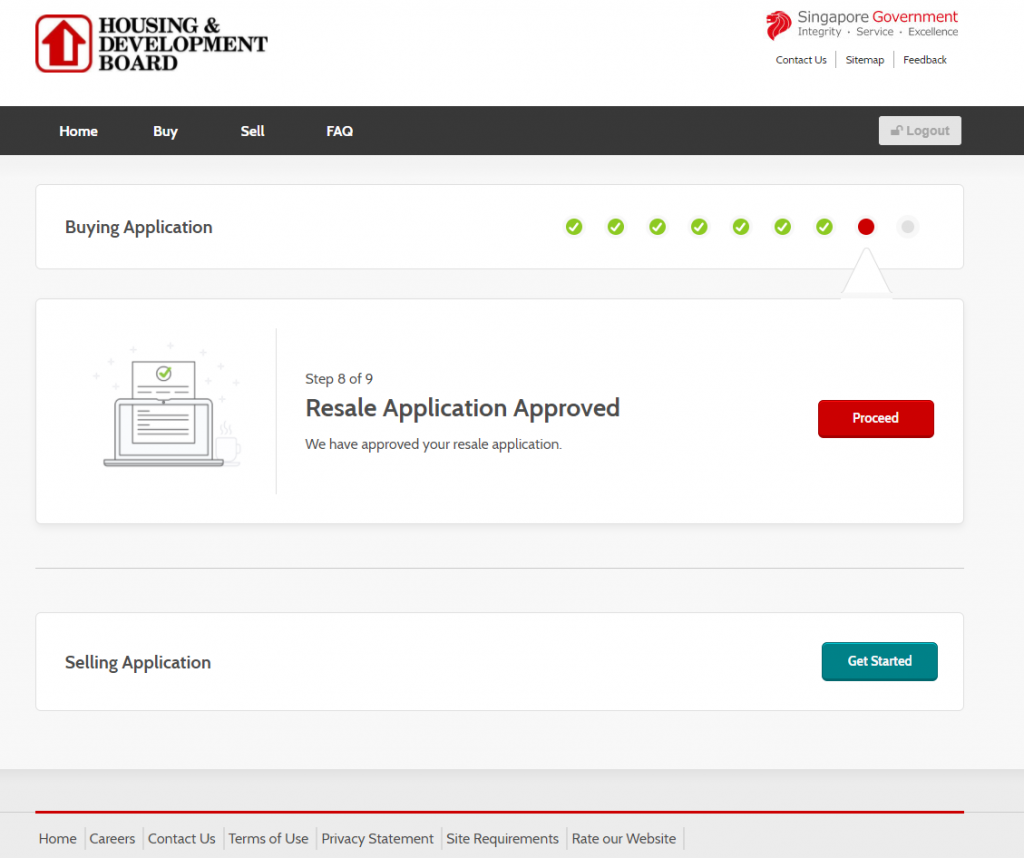

Once the fees are paid, all you need to do is wait for HDB to review and approve the resale application. You will receive an SMS notification when that happens!

7. Attend Resale Completion Appointment

You’ll also be notified on your Resale Completion Appointment at the HDB Hub in Toa Payoh, where both you and your buyer will need to attend to finalise the transaction.

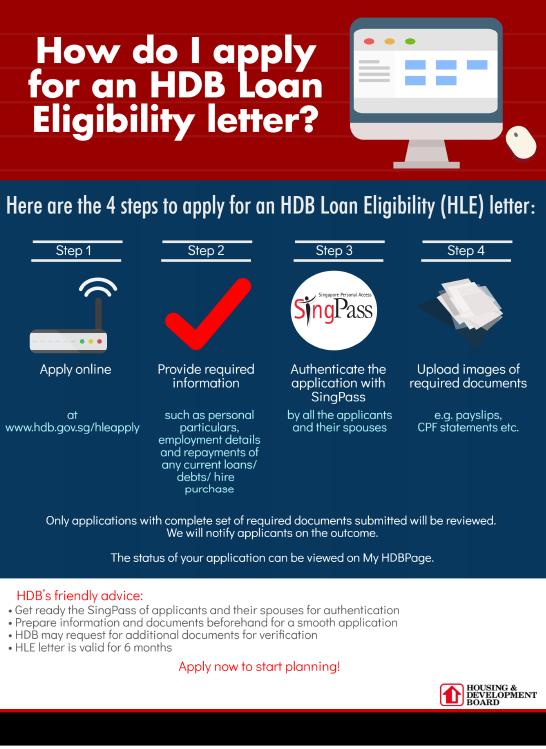

Once you have a great partner by your side and a shiny ring on the finger, it is only natural that both of you would be looking to buy your very own home sweet home. If you wish to take a housing loan from HDB, be sure to apply for your HDB Loan Eligibility (HLE) letter before you seek out your new pad.

Why do I need an HLE Letter?

An HLE letter will tell you the amount of HDB housing loan you are eligible for, the repayment preiod, and other important financial details. This loan amount, coupled with CPF housing grants, as well as your CPF and cash savings, make up the budget for your flat.

Armed with this information, you can avoid falling in love with a flat that is beyond your means.

You will need a valid HLE letter when you book a new flat with HDB, or even when you exercise an Option to Purchase to buy a resale flat.

Okay… so how do I apply for an HLE Letter?

There are only 4 steps to apply for an HLE letter. You can do so online via HDB InfoWEB. Do prepare the required information and documents beforehand for a smoother application.

Not everyone is eligible for an HDB housing loan though, so it is best to check on your loan eligibility as early as possible. Having an HLE letter in hand will also help you plan your flat budget. There is no harm in planning ahead; after all, the HLE letter is valid for 6 months and there is no payment involved to apply for one.

What if I did not get a large enough loan?

Regular income, age, and financial standing are 3 main factors that HDB considers in loan assessment. If you are just starting out in your career, and the eligible HDB loan amount is insufficient to cover the price of the flat you have your eye on, look around some more. There will be a flat for every budget and need.

Spend within your means and do not overstretch yourself financially — a cheaper flat might mean more money for rainy days, renovations, furnishings, or even a vacation.

We also have other financial tools; to help with your planning. All the best in working out a housing budget, so you can make an informed decision when buying a flat!

HDB resale flat buyers and sellers can now use the new HDB Resale Portal, launched on 1 January 2018.

The HDB Resale Portal streamlines all the resale of flats processes into a single platform, and provides a step-by-step guide for flat buyers and sellers throughout the resale transaction.

Using the HDB Resale Portal will benefit you in many ways:

– Shortens resale transaction time by up to 8 weeks

– Reduces manual entry of personal information

– Integrates all resale-related services

– Reduces number of appointments with HDB (Only 1 appointment required!)

With this portal, you can get instant results on your eligibility to buy a flat, housing grants, and HDB concessionary housing loan. Other important information, such as the Ethnic Integration Policy quota, upgrading status, upgrading costs billing status, and recent resale flat transactions nearby, have also been included in the HDB Resale Portal.

Here are the key steps to guide you in using the resale portal.

1. Register intent to buy/ sell

You must first register your intent to buy or sell a flat on the HDB Resale Portal. Your personal particulars will be automatically retrieved and populated from the Government’s MyInfo service.

2. Search for a flat and get an Option to Purchase (OTP)

Once you have found a resale flat within your budget, you will need to obtain an OTP from the seller. You have 21 days to exercise the OTP.

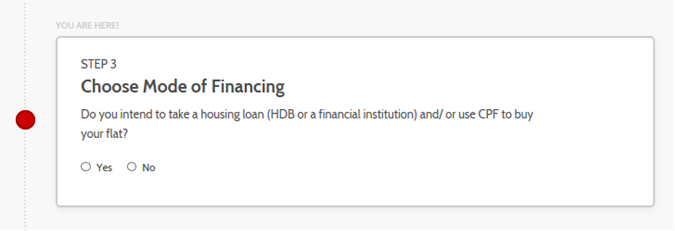

3. Choose the mode of financing

As a flat buyer, you will need to decide how you intend to finance the flat purchase. You can either use cash, CPF savings, or obtain a housing loan. If you wish to obtain an HDB housing loan, the HDB Resale Portal will guide you to apply for an HDB Eligibility Letter.

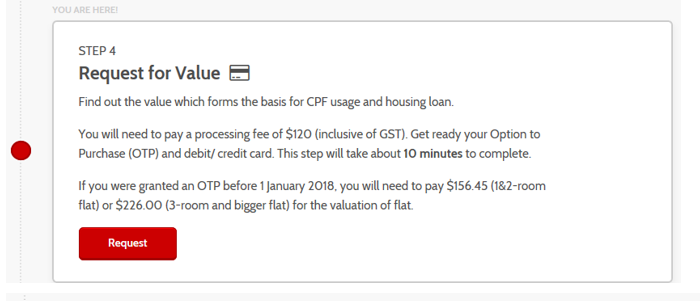

4. Request value of flat from HDB

If you are financing the flat purchase with your CPF savings and/or housing loan, you are required to submit a request to HDB to confirm the loan quantum and the amount of CPF savings you can use. You will pay HDB a processing fee of $120 (including GST).

Flat buyers can only submit a Request for Valuation after the seller has granted them an OTP. They will need to submit the Page 1 of the OTP and Request for Valuation, to HDB by the next working day after the OTP date.

If HDB requires valuation of the flat to be done, HDB’s appointed valuer will carry out the flat inspection within 3 working days after informing the seller. Flat buyers can check the flat’s valuation in the HDB Resale Portal within 10 working days from the inspection date.

5. Submit resale application

Both flat buyers and sellers must submit their respective portions of the resale application with the supporting documents to the HDB Resale Portal, after the OTP has been exercised. They will need to pay an administrative fee, depending on the flat type.

HDB will verify the information and notify the buyers and sellers of the application outcome, typically within 8 weeks.

6. Acknowledge resale documents

HDB will compute and prepare the documents for buyers and sellers to endorse in the HDB Resale Portal. Both parties must endorse the documents within 6 days.

7. Pay resale fee

Flat buyers and sellers are required to pay online for the legal and stamp fees using the HDB Resale Portal.

8. Wait for HDB’s approval

HDB will inform flat buyers and sellers once the application has been approved. The approval letter will be available on the HDB Resale Portal.

9. Attend completion appointment

Flats buyers and sellers must attend the Completion Appointment at HDB Hub to complete the resale transaction.

In summary, here are the steps for flat buyers and sellers:

Buying a flat is a huge financial commitment (you already know that!) and getting a second flat is no easier. There are many things to consider, so read on to make sure you have everything covered before putting your money down for your second home.

Computing your estimated sale proceeds

Do you know how much proceeds you might receive from the sale of your existing flat? As the cash proceeds will form part of your budget for your next flat, having a realistic estimate is crucial to helping you calculate the amount you can afford to spend. Simple math!

With information such as your outstanding mortgage loan, CPF funds used including interest, resale levy (if applicable), and some of the other payments due, you can use HDB’s Sale Proceeds Calculator to get a ballpark estimate of the cash proceeds from the sale of your flat!

Resale levy

You do not have to worry about the resale levy, if you plan on getting a resale flat on the open market next.

The resale levy applies to those who plan to buy a new flat from HDB, but have previously received some form of subsidy for their first flat – be it through the purchase of a flat from HDB, or a resale flat with the CPF housing grants.

As new HDB flats are sold at a subsidised price, the resale levy is put in place to ensure that there is a fair allocation of public housing subsidies between first-timers and second-timers.

Grants available

Second-timer home buyers can also be eligible for housing grants! If you are buying a resale flat that is within 4 km of where your parents/ child currently stay, you may be eligible to apply for the Proximity Housing Grant, which aims to help more families live close to each other for mutual care and support.

If you are intending to take a second HDB loan, do note that your loan amount will factor in your CPF and cash proceeds from the sale of your flat. This is to ensure that you do not over-borrow!

The commercial interest rate will be applied to your HDB housing loan if you plan to sell your current flat only after buying your next flat. The interest rate will be converted to the concessionary rate only after you have sold your current flat, and used the proceeds to repay your housing loan.

Contra Facility

Want to sell your existing HDB flat and buy another flat at the same time? Consider applying for the Contra Facility, which allows you to use the cash and CPF proceeds from the sale of your existing flat to purchase your next flat, concurrently.

The Contra Facility can help you reduce the cash outlay needed for your next flat, the mortgage loan amount needed and the subsequent monthly repayments. If you are buying a new flat, you can collect the keys to your new flat and renovate it, while selling your existing flat!

We hope this article has made financial planning for your second HDB flat less daunting. Follow us on Facebook for more useful information on buying a HDB flat and HDB living.

The post ‘My Resale Journey From West to East’ appeared first on the MoneySmart blog

This article was updated on 25 May 2021.

Conversations around public housing usually revolve around affordability, value, and financing. Beyond the dollars and cents, it’s hard to get a tangible sense of what owning a flat means to people, and the significance of having a home to call their own.

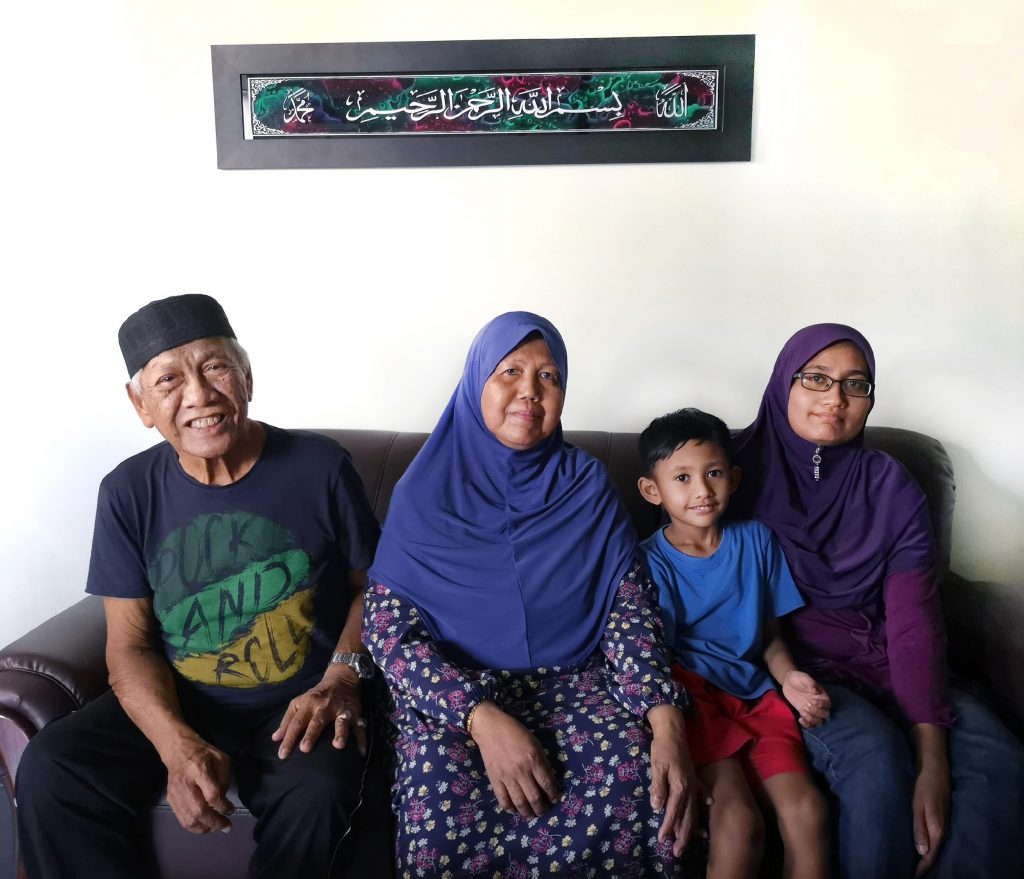

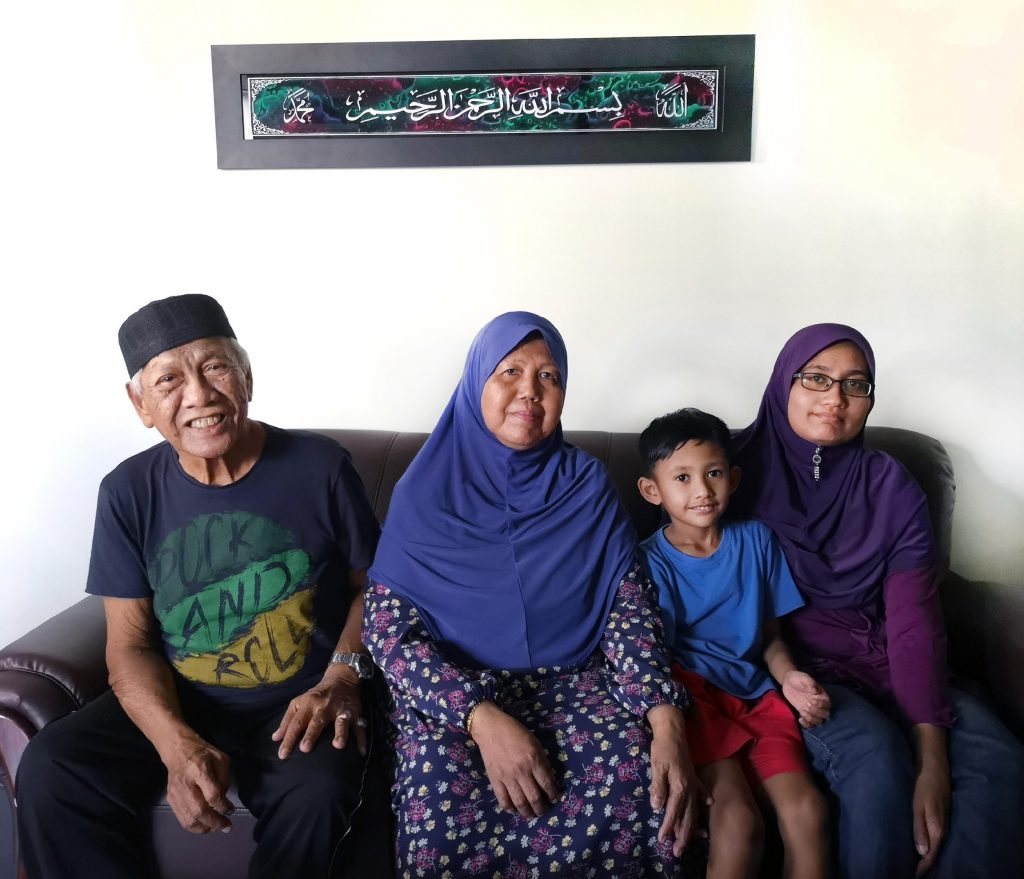

We spoke to different homeowners, specifically those who had bought resale flats, to get their thoughts about their home and flat buying journey. In the first of our 3-part series, we speak to Mr Ismail, who has lived on both sides of the island.

About The Flat

Owner: Mr Ismail bin Hamid, 41, Married with 4 kids

Location

Tampines

Flat Price

$410,000 (after $20,000 Proximity Housing Grant)

Year of Purchase

2018

Flat Type & Size

4-room flat/ 104 sqm

Remaining Length of Lease

63 years (as of Apr 2019)

Monthly mortgage amount & loan tenure

Nil (fully paid after selling previous flat)

Monthly mortgage amount & loan tenure

About $38,000

MoneySmart (MS): Mr Ismail, this is an amazing looking house. Tell us a little bit about why you chose to buy a flat here.

Mr Ismail: Tampines has been my home for the past 7 years. This flat is located 2 blocks away from where I grew up in, so this is a neighbourhood I am very familiar with. In fact, one of my primary school classmates still lives in the next block with his own family!

When I was growing up, there was only Bedok Interchange. There was no Tampines Interchange, and the Downtown Line certainly didn’t exist at that time, so you can imagine that getting around was very different from how it is now.

MS: Tell us a bit about your housing journey.

Mr Ismail: After I got married, my wife and I moved to Bukit Batok, which was near her family. It was a very different area from where I grew up, so that was something new. We then moved to a resale flat in Bukit Panjang. With convenience and proximity to family being a key consideration, we decided not to wait for a suitable BTO flat. At that time, the only available BTO flats were in Sengkang and Punggol, so we chose to buy a resale flat.

Due to family circumstances, we eventually moved back to the East, a few streets away from where we are currently staying now.

MoneySmart Tip: Interested flat buyers can get information on upcoming BTO projects 3 months before sales exercises for better planning. In the meantime, you can visit HDB InfoWEB for details on the upcoming BTO sales exercise.

MS: We also understand that you moved from a 5-room to a 4-room flat?

Mr Ismail: We felt that it was a much better idea to move to a 4-room flat because there was a lot of unused space in our previous 5-room flat. Even though we have four kids (aged 12, 9, 8, and 3), we felt that this current place suits our needs perfectly.

As you can see, the amenities around this place are great for our kids. We also considered the fact that there was a park that was very accessible and our kids wouldn’t have to cross any major roads to get there.

At this point, Mr Ismail’s wife also chimes in, highlighting the fact that the 4-room flat is much easier to clean than their previous home. They also managed to completely pay off their housing loan after moving, but more on that later.

MS: Tell us about your home buying process. Did you engage an agent or do it on your own?

Mr Ismail: We decided to go with an agent, and the reason was that our housing agent was also my friend from reservist! He also helped us to sell our previous home. I would say when it comes to engaging an agent, it definitely helps to have someone who knows his stuff.

It was an easy decision to buy our current home because we knew what we wanted, and the opportunity presented itself. I would say our only regret is that we missed out on a flat that is near the newly built Our Tampines Hub. There was nothing there at that point in time and we had no idea they were going to build an integrated community hub there!

MoneySmart Tip: Besides going through an agent, buyers and sellers can use the HDB Resale Portal to perform their own resale transactions. The portal will guide you on the buying journey and help you track the progress of your transaction. The resale process takes approximately 8 weeks to complete from the date of HDB’s acceptance of the resale application.

MS: How did you plan your finances? What were your goals or considerations?

Mr Ismail: For me, I chose to pay off this flat fully. I know it might seem a little “old school”, but we believe that we should just keep our money in CPF and use that for retirement.

For our previous homes, we also chose to take a loan from HDB. My wife works in a bank, so we understand that there are benefits and risks to taking a bank loan, and we ultimately settled on getting an HDB loan. Now that we’ve paid off this flat, we don’t have to worry about a mortgage anymore, and we can focus on planning for retirement.

MS: And what sort of grants did you get for your home?

Mr Ismail: At the start when we got our first place after we got married, we were eligible for a grant for first time buyers, and of course we were aware that we could get $20,000 in Proximity Housing Grant for this flat as we were moving near my parents.

MS: Your home looks really nice and comfortable. Did you have to renovate it a lot, and how much did you spend?

Mr Ismail: We spent about $38,000 on our renovations. We did have to do quite a bit of work, which included your regular maintenance such as repainting the place and redoing the flooring and doors. The main issue with the place was that the wiring wasn’t done properly so we had to redo everything because they were crossed all over the place. The kitchen was also rather old so we gave it a refresh.

MS: Can you share with us some thoughts around owning a home in Singapore?

Mr Ismail: For me, I never intended to buy a flat to profit from it. I plan to stay here with my wife till we pass on. Some people talk about leases expiring, but my perspective is that you are probably not even going to be alive when that lease expires, so why worry about it? As for my children, they will probably move out and buy a flat of their own, so I am not too worried about what happens with the lease.

There are many things that might change in the future which you have no idea about, so you plan for what you can. Other than that, I feel blessed to be able to say that I own a home, which is more than what many other people in other developed countries can say.

MS: Any other words of advice for homebuyers?

Mr Ismail: Go with what you are comfortable with. At the end of the day, you can overthink, but when you step into a neighbourhood, just ask yourself whether you feel like you belong there . Are you comfortable with the place and its surroundings? Is it a place you feel your children can grow up in?

Convenience is another factor. It might be more important for you to be near a supermarket than an MRT station. Whatever the case, understanding your needs is important. Small inconveniences can become a big deal over the course of a few years.

My Resale Flat Journey: First Property is 30-Year Old Resale Flat

The post ‘My Resale Journey: First Property is a 30-Year Old Resale Flat’ appeared first on the MoneySmart blog

Mr Wong, 32, and his wife, Madam Lai, 31, are on the cusp of moving into a resale flat in Jurong West with their child, as well as Madam Lai’s brother and sister-in-law.

The couple’s 5-room flat has just been renovated, and they are now putting the finishing touches to their new home.

In this second part of a 3-part series in which we present the stories of resale flat buyers, we spoke with Mr Wong on his new home and the process he went through to purchase his resale flat.

About The Flat

Owner: Mr Wong Bin Hao, 32, married with 1 kid

Location

Jurong West

Flat Price

$335,000 (after $40,000 housing grants)

Year of Purchase

2018

Flat Type & Size

5-room flat/ 121 sqm

Remaining Length of Lease

69 years (as of May 2019)

Monthly Mortgage Amount & Loan Tenure

About $1,600

18 years

Renovation Cost

About $35,000

When we visited Mr Wong’s flat at Jurong West Avenue 5, workmen were finishing up their final renovations.

But the flat already looked cosy and inviting, with a comfy couch and a pile of Hello Kitty cushions beckoning us as we entered.

MoneySmart (MS): Mr Wong, how did you and your wife decide to buy a flat in Jurong West?

My wife and I both work in the Jurong area. For a period of time, we rented in nearby neighbourhoods and moved around.

I have been living in Jurong West for about three to four years. I’ve always found this area quite lively and naturally, wanted to buy a home here.

MS: Besides the fact that it’s lively, what else about this place appealed to you?

My two-year-old kid goes to the childcare centre in this block. You can also see the playground from here so it’s perfect and convenient for us. There are some primary schools close by that my child can attend in the future.

There are also two malls nearby, Pioneer Mall and Gek Poh. When the future Jurong Region Line is up, we will be within walking distance to an MRT station, so I think it was worth the buy.

MS: You started out renting a flat. What made you decide to take the plunge and buy your own place?

For me, having that sense of ownership is important.

When you rent, you might need to move from time to time, like what happened to us in the past. I found it tiring to be moving from house to house every year or so.

Some landlords are also not prepared to accept tenants who keep different hours or lifestyles. At the start they may say everything is okay, then suddenly they become fussy and impose curfews on the tenants.

There are uncertainties when you rent a place with friends too – they may need to move elsewhere and you will need to find another flat mate.

When I rented a place, I had to pay the landlord rent in cash every month, and could not make use of my CPF savings. Now, I can pay my housing loan instalments using CPF, so I don’t really need to fork out cash. For all these reasons, I feel it is good to have my own flat.

MS: We understand that your flat is about 30 years old. Was its age a concern for you?

One reason why I bought a resale flat is that it is more spacious for my family. This flat is about 120 sqm and the kids have more space to run around. Sometimes my parents or my wife’s parents will visit. So it’s better to have more space.

We still have 69 years left on the lease which is good enough for us. Our children and future generations are likely to buy their own homes anyway, so we don’t need to worry about leaving this flat for them. As we are planning to use this flat as a home, I think it’s good enough. For the next generation, you don’t need to bother as the kids will buy their own homes.

Although this is an old estate, the area is well taken care of by the Town Council and HDB also carries out upgrading of the flats.

MoneySmart Tip: Use this online map service to get lease information, resale prices, and even season parking information for each housing block. You can filter through nearby amenities to see where to dine and shop.

MS: Do you see your flat as an investment?

When we were weighing the pros and cons of buying a 30-year-old flat compared to a newer one, we did think about this issue. However, we feel that a house is for the long-term and one that would see us through our old age. Instead of hoping to make a profit from moving houses, we would rather stay in one flat and finish paying our housing loan sooner, so that we can free up our finances for other things.

MS: How was the purchase process? Did you go through an agent or DIY?

We initially tried to DIY by using a property website, but later on we received calls from estate agents offering their services and we engaged an agent eventually. He asked us what sort of attributes we wanted in a flat, and helped us to look for suitable flats that were within our budget.

Everyone has different interests and needs, so it’s important to know what your own needs are, before you decide whether to engage an estate agent for your resale transaction.

MoneySmart Tip: We asked Mr Wong if he knows about HDB’s Resale Portal, and he says he doesn’t. The HDB Resale Portal could have guided him in the buying journey. It takes buyers and sellers through the buying and selling process in a step-by-step manner online and allows them to DIY their transaction if they choose not to engage an estate agent.

MS: How is your flat being financed?

We went for an HDB loan as we found it less complicated than going for a bank loan. For bank loans, the interest rate is a bit uncertain.

Although the HDB loan interest rate is currently higher than for bank loans, the difference is not that much after you do the math.

Initially we indicated that we wanted to settle the loan in 10 years. Then HDB called us to ask whether we wanted to reconsider. Based on our salary, they recommended an 18-year loan tenure so that we can buffer for things like employment changes or if we suddenly need cash for urgent reasons. They explained that we can make partial capital repayment or even redeem the loan earlier if our finances permit. We found the advice useful. My wife and I are planning to settle the loan earlier to incur less interest and save more for retirement.

MoneySmart Tip: Find out how you can make partial capital repayment or fully redeem your HDB loan and save on housing loan interest.

MS: Did you get to enjoy any grant?

We got the housing grant for first-time buyers, which was a really attractive sum. We initially set aside a bigger budget as we thought we would not be eligible for grants. So for us, getting the grant was a bonus.

We spent about $35,000 on renovations, mainly for works in the kitchen and for furnishings around the house. This includes $16,000 paid to our contractor, who was flexible to work with.

We did not hire interior design firms as we found their prices quite high. Since we wanted to save money, we thought it was better to work directly with contractors. For example, the rewiring cost quoted by the contractor was cheaper than market rate!

MS: Any advice for aspiring homebuyers?

You don’t really need to look for flats with fanciful fittings, because you will probably have to do your own renovations anyway. For example, even if the flat comes with nice flooring, the colour of the tiles may be uneven after the previous flat owner has removed all their furniture. So you might still need to replace the floor tiles.

MoneySmartTip: Planning your renovations for your HDB flat? Know what’s important to note and familiarise yourself with the guidelines.

My Resale Flat Journey: A Change of Scenery After More Than 20 Years

The post ‘My Resale Journey: A Change of Scenery After More Than 20 Years’ appeared first on the MoneySmart blog

After living in the West for more than two decades, Mr Bactarudin bin Launon and his wife decided it was time to move.

The couple, who previously lived in a 4-room flat in Jurong West, moved to a 3-room resale flat in Marsiling in January this year. This was in part motivated by the desire to stay closer to their daughter, and also better prepare for retirement by paying off their home loan.

For this final installment of our 3-part series profiling HDB resale flat buyers, we had a chat with Mr Bactarudin about his new home, his experiences as a resale flat buyer and his thoughts on owning a home in Singapore

About the Flat

Owner: Mr Bactarudin bin Launon, 70, married with a daughter who has moved out.

Location

Marsiling

Flat Price

$220,000 (after $20,000 Proximity Housing Grant)

Year of Purchase

2018

Flat Type & Size

3-room flat/ 76 sqm

Remaining Length of Lease

55 years (as of May 2019)

Monthly Mortgage Amount & Loan Tenure

Nil (fully paid after selling previous flat)

Renovation Cost

About $20,000

Mr Bactarudin and his wife greeted us in the living room of their newly-renovated flat at Marsiling Lane.

Mr Bactarudin, a security guard, was taking two weeks’ off work to recuperate after a fall.

While the couple appeared to have settled in well and seemed familiar with their new neighbourhood, they revealed that they had actually moved in just three months ago.

MoneySmart (MS): Thanks so much for having us here. We understand you used to live in Jurong West. Why did you decide to move to Marsiling?

Yes, we lived in Jurong West for 24 years before moving here. We sold our 4-room flat and rightsized to a 3-room flat.

MoneySmart Tip: Mr Bactarudin and his wife received a $20,000 Proximity Housing Grant, as they moved within 4 km of their daughter. Buyers who plan to take up the Proximity Housing Grant can check online whether the flat they intend to buy is within the 4km radius of their parents or children.

MS: Any reasons for not buying a smaller flat in Jurong?

Jurong is a big commercial area and I find things there becoming more expensive.

We also could not find a 3-room flat in the Jurong area for the same price as our current flat. Together with the fact that we could be closer to our daughter and grandchildren, getting this flat here in Marsiling at the price we bought it for was a natural decision.

MoneySmart Tip: To find out transacted resale prices sorted by different towns and flat types, buyers and sellers can access the median resale prices released every quarter.

MS: Having lived in the west for so long, how are you adapting to your new neighbourhood?

Based on my experience interacting with people, it’s almost the same. Depends on whether you take the initiative to greet them also, because we’re the newcomers here.

My neighbour here, who lives opposite us, talked to me first: “Uncle how are you, where you are from?” and so on. This was the first day after I moved in, and I was doing painting outside when they were leaving for work. The second day, I was once again doing painting outside and they started another conversation with me. I told them I moved here from Jurong, and then asked them more about themselves. That’s how we got to know each other.

MS: Are there any big differences between Marsiling and Jurong West?

I’m quite happy living here and find it comfortable.

Within the flat, I don’t see much difference between this and our old home. Outside the home, one main difference is having to walk further for makan.

The eating places in Jurong West were nearer to home. I could cross the road and have teh tarik. Over here in Marsiling, there is a supermarket, 7-11, and a wet/ dry market. It is further away and we will visit once in a while.

But most of the times, we cook at home so we don’t really go to these eateries that often.

MS: Did you get your current Marsiling resale flat through an agent or did you DIY the transaction?

We bought the flat through an agent who is a relative’s friend. They helped with everything. We just let them do everything. They found the price we wanted.

We viewed quite a few resale flats before making a decision. We did not move into this flat until our previous flat was sold.

MS: How did you finance the flat?

We didn’t take out a loan. The flat is fully paid for, so we do not need to pay any monthly instalments.

As I also needed money for my medical condition, selling the old flat and moving to a smaller one was a financial decision as well.

MS: What about the renovations?

We did our own renovations. I think we spent about $8,000.

His wife interjected that the renovations actually cost about $20,000.

We had to do a little bit of wiring. The bulk of the cost went into renovating the kitchen. We also spent on the flooring, sink, fittings, and buying furnishings.

MS: What are your thoughts on buying and owning a home in Singapore?

I’m from Singapore, this is my place, this is my country, this is where I was born.

Singapore is still where I would prefer to have a home to call my own. I recall some friends who bought a place outside Singapore – it may work for you if money is not an issue. But they were not familiar with the rules and the foreign environment. I have worries on what will happen to them if they don’t like it there and have to find another home if they want to return to Singapore.

If you are eyeing a new HDB flat, you would have thought about where your future home will be. For those still mulling it over, we break down the key differences between mature and non-mature estates.

Flat Prices

New flats are sold at subsidised prices, regardless of location. However, flat prices may vary based on factors like flat attributes, surrounding amenities and locations. In general, prices of flats in non-mature estates tend to be lower than those located in mature ones.

Regardless where you are aiming to set up your new home, you can receive the Enhanced CPF Housing Grant of up to $80,000 when you buy a flat.

Amenities

Home is so much more than just the four walls of your flat – amenities matter, too. Mature estates, as their name implies, are older as they were established much earlier than their non-mature counterparts. As such, residents enjoy various amenities that have been developed over the years. These include transport networks, shopping malls, schools, and parks.

But non-mature estates are far from under-developed! While not all amenities may be ready the minute you move in, give it some time and you’ll soon enjoy new facilities that might end up being the envy of others. Just look at Punggol or example! Singapore’s first eco-town now bustling with life, full of amenities comparable to mature estates. There are shops and communal spaces aplenty at Oasis Terraces, HDB’s first New Generation Neighbourhood Centre. Punggol Waterway, which meanders through the town, is also home to water-based recreation activities and other community activities.

Residents in newer estates also get to enjoy a living environment enhanced by the latest state-of-the-art urban solutions. Projects in Punggol are fitted with innovative eco-features such as centralised recycling refuse chutes to promote recycling; rainwater harvesting system to encourage water conservation, and LED with motion sensors.

TLDR: It Depends on Your Needs and Priorities

Of course, as with most decisions, there are pros and cons.

Flats in non-mature estates are great, budget-friendly options. While amenities in these estates might still be work-in-progress when you move in, you will soon be able to enjoy a wide range of new facilities near your home.

Mature estates have their own charm, with many established amenities around. However, competition for new flats in mature estates can be stiff, with a much smaller pool of flats available as compared to non-mature estates.

If mature estate is still your cup of tea, you can consider resale flats, too. You may be eligible for grants of up to $160,000 if you buy a resale flat.

All in all, whether a mature or non-mature estate is the best for you depends largely on your priorities. Still confused or need more advice on flat buying? Be sure to check out more of our articles!

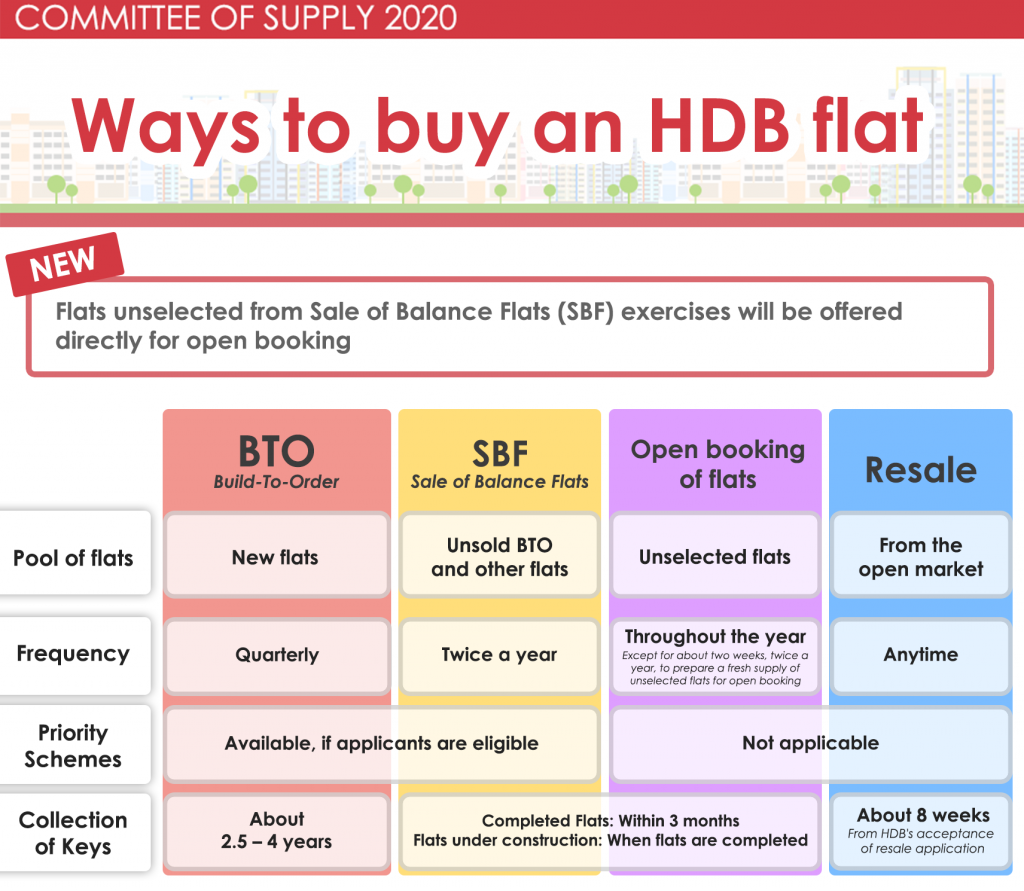

If you’re looking to purchase your first home, chances are you’ll be familiar with the Build-to-Order (BTO) and Sale of Balance (SBF) exercises. Did you know that in addition to these, you can also apply for flats through the Open Booking exercise and book a unit as early as the next working day?

Read on to find out more about HDB’s different sales modes!

Build-To-Order (BTO)

HDB launches new BTO flats for sale 4 times a year. A range of flat types in different towns are offered during each launch, providing home seekers with a range of housing options for every budget and need. BTO projects are announced 3 months prior to their launch, to help you with your planning.

At the close of each exercise, a ballot is conducted, and results are announced approximately 3 weeks later. If you want a flat faster, look out and apply for BTO projects that have a shorter waiting time of 2-3 years.

Sale of Balance (SBF)

SBF takes place twice a year, in May and November, alongside the sales exercises. With SBF, you can apply for balance flats from earlier BTO sales launches, surplus flats in projects built for those affected by the Selective En bloc Redevelopment Scheme (SERS), as well as flats repurchased by HDB. As such, there is usually a variety of flat types across different towns. You can indicate your preferred flat type and town during your application.

The flats could be under construction, near completion, or already completed. Hence, this is an option if you prefer to buy flats with a shorter waiting time compared to new BTO flats. But do note that the number of such balance units offered in each town is usually limited, and likely to attract high demand.

Open Booking of Flats

Open Booking of Flats lets you apply for a flat online any time throughout the year and to book a unit as soon as the next working day.

Currently, flats that are not taken up during SBF exercises are offered through the Re-Offer of Balance (ROF) flats before they are made available for open booking. To help buyers get their homes earlier, we will do away with ROF exercises, and offer unselected flats from SBF exercises directly for open booking. This was part of measures announced by Minister Lawrence Wong to keep housing accessible, at the Committee of Supply Debate 2020.

The Case for Buying the Most Affordable Home You Can

My co-founder bought a 3-room resale flat in a mature estate last year for a tidy $430,000 in Marine Parade (before the various CPF Housing Grants).

Personally, I think this is a pretty smart decision, given his income and lifestyle. A 3-room flat (or 4 room) flat also makes more sense compared to a 5-room flat, because:

Less rooms to clean

Less money spent on renovation

Lesser need for so many rooms anyway, if you’re not intending to have kids

That said, conventional home owner wisdom is to buy the biggest or the most expensive HDB flat based on your budget. I know couples who don’t earn that much but are considering going all out for HDB flats in locations like Boon Keng, where the resale prices could be as high as $900,000.

Yikes.

Today I’d like to present another argument: why you should buy the most affordable flat you can.

Now, I’m going to qualify some stuff upfront.

What we mean specifically is to ‘buy the most affordable flat that meets your needs, not ‘buy the absolutely cheapest flat.’

There is a difference.

Avoid the ‘asset rich, cash poor’ trap that many people fall into

To many traditional Singaporeans, this is the idea of being rich: Own lots of expensive things and live in a big house. This mindset is a key ingredient for a lifetime of debt.

But consider this other definition of being rich: Having enough money and freedom for many experiences – cycling around the world, starting a business, supporting causes you’re passionate about, spending more time with your ageing parents and young children.

We think, in the 21st century, the real marker of wealth is time, mobility and options.

All three cannot be achieved if you’re bogged-down paying for an expensive flat way beyond your means. BUT, they can be achieved if you work on your investments. Which brings us to our next point.

Buying a home beyond your means will limit your investment potential

Okay let’s get one thing clear.

There are generally two types of residential property in this world – property you live in, and property you invest in.

The first one is where you just live in and don’t make money from. This is your *home*. Even when you sell your home to get cash, chances are you’ll use this cash to buy another home.

The second is one you try to make money from. This is called an investment.

Sometimes, these two categories overlap. HDB flats, which are meant to be affordable public housing for homeownership, typically fall in the first category (more on this later).

Sometimes, these two categories overlap. HDB flats, which are meant to be affordable public housing for homeownership, typically fall in the first category (more on this later).

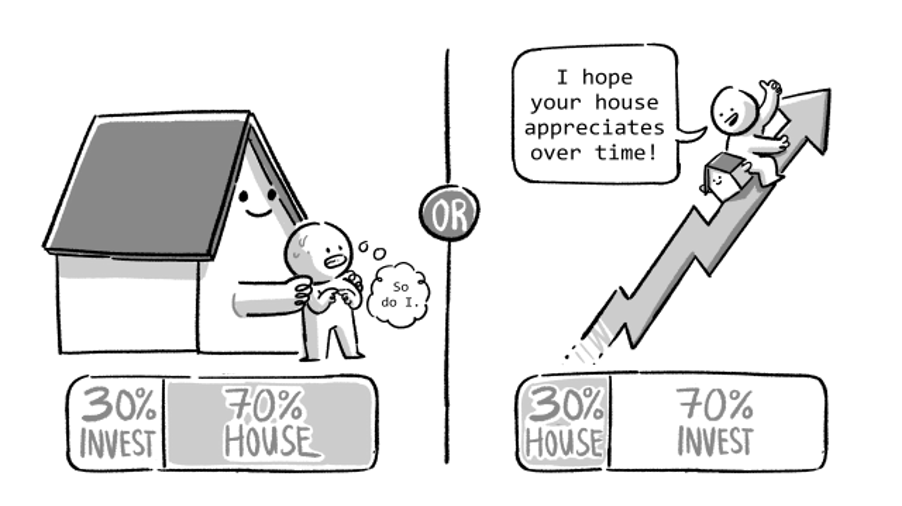

The more money spent on your home, the less money you have for investments (investment property, stocks, bonds, etc). Now, this sounds ridiculously simple, but many will find this hard to understand.

Simplified even further, it looks like this:

You want to retire earlier: spend below your means on your home, spend more on investments.

You want to retire at 62 like everyone else: spend within your means on your home, invest as per normal.

You want to have insufficient retirement funds: spend beyond your means on a home, don’t invest.

Here’s some boring math to drive the point home (pun intended). STAY WITH ME.

Let’s assume you buy an HDB flat and stretch payments across 30 years, at an interest rate of 1.7% p.a. These are what your mortgage payments will look like.

Property price

Monthly repayment, assuming 1.7% p.a over 30 years

$400,000

$1,419

$600,000

$2,129

$800,000

$2,838

If you had picked the $400,000 flat over the $600,000 one, you would have $710 more each month for your savings or investment.

This doesn’t seem like much, but let’s look at the opportunity cost of investing the $710 over 30 years.

Place

Interest rate

Opportunity cost of having $710 invested over 30 years

Under your mattress/ In a biscuit tin

(TWS does not recommend this investment vehicle)

0%

$255,600

CPF SA

4%

$486,542

Stock Market (conservative)

5%

$578,916.

Stock market (optimistic)

7%

$830,311

Now, I want to be very clear. We’re not saying that buying a $600,000 or $800,000 flat is a financial disaster.

If your combined household income is like $20,000, go ahead. You can buy pretty much any HDB flat you want and have enough left over to work towards your financial freedom.

But if you and your spouse are the median Singaporean couple earning about the median household income of $9,425, you need to be more cautious.

Which brings us to this.

What’s ‘too much’ to spend on a flat?

To avoid spending too much on a flat, you must know what is too much. Here are two methods you might find useful to judge whether your flat is too ex.

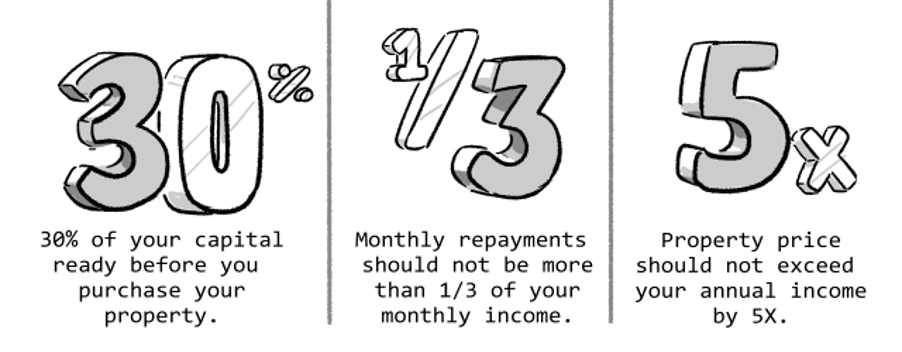

The first is the 3-3-5 rule, popularised by property blogger Property Soul and often criticised for being too conservative.

Following the ‘3-3-5’ means you meet all of the following criteria:

You should have 30% of your capital ready before you purchase your property

Your monthly repayments should not be more than ⅓ of your monthly income

And the property price should not exceed your annual income by 5x

Our suggestion is to use the last rule and then work backwards. It looks like this:

Your household income

The max price of a flat you should buy

Save this amount before buying

Your max monthly payments

$9,425 (median income in 2019)

$565,600

$169,650

$3,141

$14,000 (income ceiling for BTO)

$840,000

$252,000

$4,666

$16,000 (income ceiling for EC)

$960,000

$288,000

$5,333

Criticism for 3-3-5

Now, a lot of people find this rule very limiting. “iF i foLlOw ThiS I cAnNoT afFoRd anYthIng,” they say.

My opinion is that the rule is a good rule of thumb, and perhaps their tastes in properties are too exquisite or aspirational.

That said, different strokes for different folks. We’re a page focused on savvy financial decisions, not living in luxury or impressing people. So, use your own judgement.

The second rule we’ve created is a simple one called “follow the crowd”

It follows the same logic you used in secondary school to find out whether you’re keeping up with the syllabus.

If you’re the only one failing a test, you should be worried. But if everybody failed a paper, you’d be relatively safe.

(We’ve lumped all 3, 4, and 5 room flats in the same category because it’s very possible for small families to overextend themselves to buy a 5-room flat when a 3-room would have sufficed.)

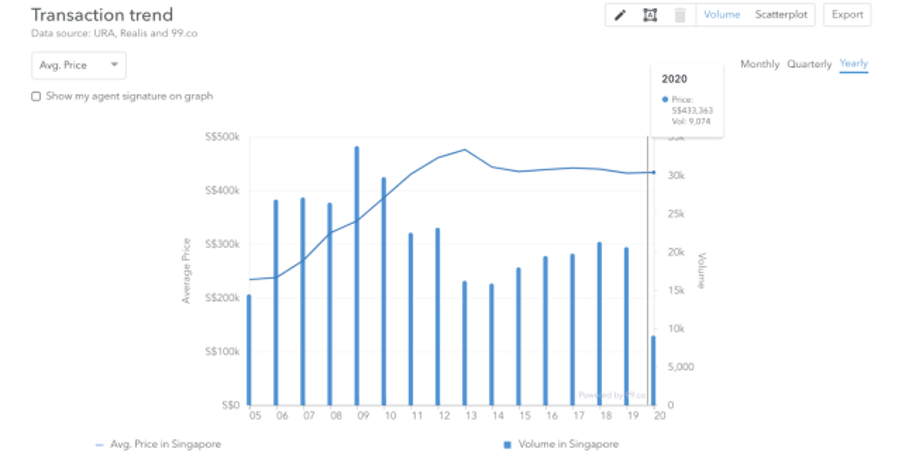

Which brings us to this magical number: The average price of all 3-, 4- and 5- room resale flats in 2020 is $430,000 (rounded down from $433,363). Typically BTO flats are cheaper, because they’re subsidised by HDB.

$430,000 isn’t a number we pulled out from nowhere, I’ve used paid software from 99.co (where I work) to generate this chart – it gets data from URA, REALIS and of course, 99.co.

At the same time, the median household income is $9,425.

If you spent more than $430,000 on your flat, but are earning below the median income, then you should be clear that you’re spending beyond the norm.

Same if you’re earning the median income but spent significantly more than $430,000.

Like the 3-3-5 rule, this isn’t something you need to follow religiously, but more of something to build self-awareness.

You’re not doomed if you ‘overspent’. But you need to recognise that you’ve spent beyond the average amount – and then work to make up for it somewhere.

If you find all these rules restrictive, you can check out HDB’s financial planning tools to help you draw your own conclusions instead.

They also have their own useful guidelines to help you make your decision.

Of course, buying a flat is not all about money

You know what? We get it. We actually do. Money isn’t everything. Buying and owning a flat is a rite of passage, and it’s often an emotional decision. A home has feelings attached to it – feelings of belonging, love, and hope.

What’s right for you?

We are not you, so we honestly don’t know.

What can be said is this: According to the Pareto principle, 80% of life’s outcomes are caused by the 20% of inputs. To simplify, 20% of your choices in life will affect 80% of your life.

Your first flat that you buy in the prime of your youth?