A Guide to CPF Housing Grants

A Guide to CPF Housing Grants

Buying a flat is a big financial commitment, so you might be glad to know that there are several housing grants available to help you offset the purchase price of the flat and embark on your home ownership journey.

Do you know which grants you’re eligible for, or how much you can get? Here’s a handy guide that breaks down all you need to know about housing grants.

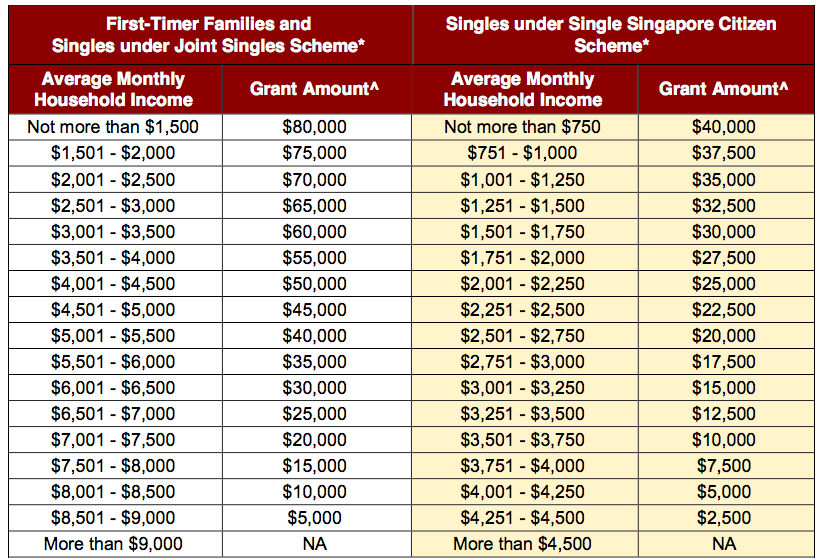

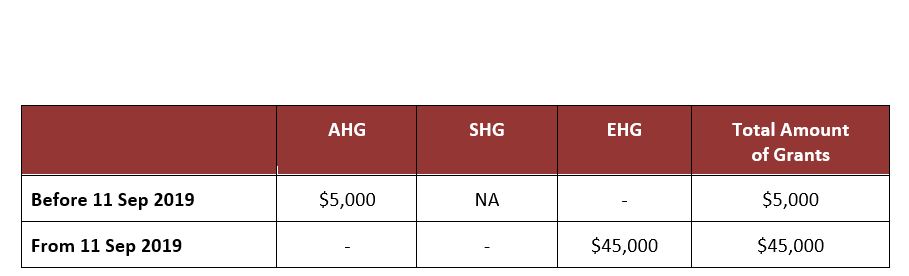

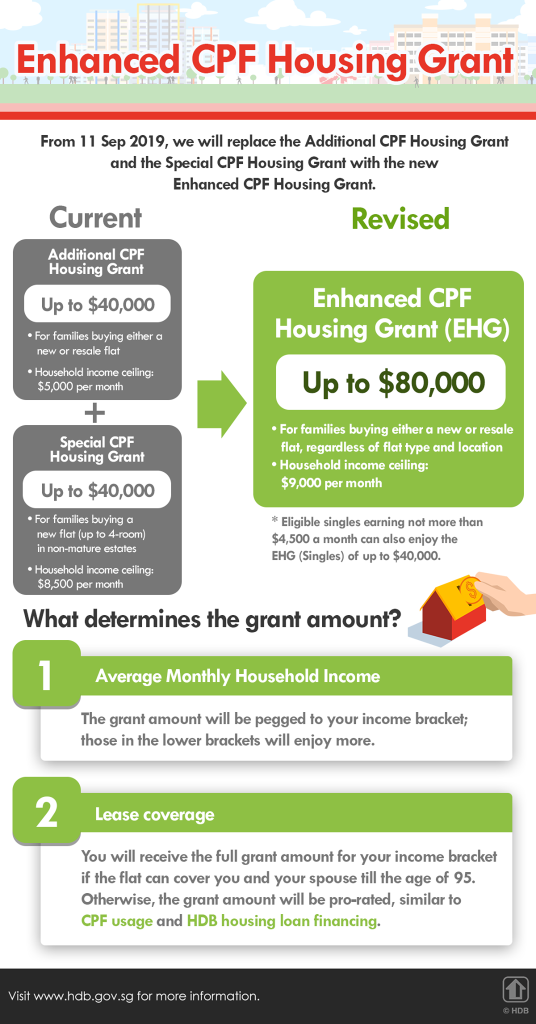

1. Enhanced CPF Housing Grant (EHG)

Who is eligible for the EHG?

First-timer citizen households and first-timer single citizens can apply for the EHG when buying a new flat from HDB or resale flat on the open market, subject to prevailing eligibility conditions. Resale flat buyers must qualify for the Family Grant or Singles Grant (whichever is applicable) to be considered eligible for the EHG.

If you’re buying a flat as a first-timer family, your average gross monthly household income must not exceed $9,000. If you’re a first-timer single, your average gross monthly income must not exceed $4,500.

What are the flat types eligible for EHG?

Generally, the EHG is applicable to both new and resale flats, for all flat types and locations. However, for first-timer single citizens, the applicable flat type would depend on the eligibility scheme and whether you are buying a new flat or resale flat. Do note though that the flat needs to have a remaining lease of at least 20 years.

How much grant can I get with the EHG?

| Household Type | Grant Quantum* |

| Eligible first-timer households | Up to $80,000, depending on household income |

| Eligible first-timer single citizens | Up to $40,000, depending on household income |

*The flat must have sufficient lease to cover the youngest buyer to the age of 95 –otherwise, the EHG will be pro-rated

Read here for more details on EHG.

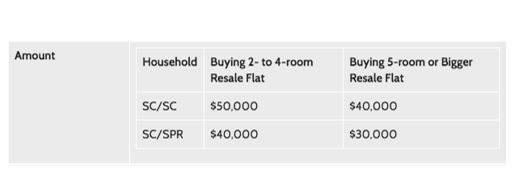

2. Family Grant

Who is eligible for the Family Grant?

You may be eligible if you’re a first-timer household buying a resale flat on the open market, and your average gross monthly household income does not exceed $14,000.

What type of flat can I buy to be eligible for the Family Grant?

2-room or bigger resale flat with a remaining lease of at least 20 years.

How much grant can I get with the Family Grant?

| Household | 2- to 4-room Resale Flat | 5-room or Bigger Resale Flat |

| Comprising two Singapore Citizens | $50,000 | $40,000 |

| Comprising a Singapore Citizen and Singapore Permanent Resident** | $40,000 | $30,000 |

** May later be eligible for the Citizen Top-Up – a $10,000 housing subsidy – when a qualifying household member becomes a Singapore Citizen

Any other grants I could be eligible for?

- Enhanced CPF Housing Grant

- Proximity Housing Grant

Read here for more details on the Family Grant.

3. Singles Grant

Who is eligible for the Singles Grant?

If you’re a first-timer single Singapore Citizen (35 years old and above) buying a resale flat with average monthly household income not exceeding $7,000, you may be eligible!

What type of flat can I buy to be eligible for the Singles Grant?

2-room to 5-room resale flat, with a remaining lease of at least 20 years.

How much grant can I get with the Singles Grant?

| Household | 2- to 4-room Resale Flat | 5-room Resale Flat |

| Single Singapore Citizen | $25,000 | $20,000 |

Any other grants I could be eligible for?

- Enhanced CPF Housing Grant for Singles

- Proximity Housing Grant

Read here for more details on the Singles Grant.

4. Proximity Housing Grant (PHG)

Who is eligible for the PHG?

This grant is for those who are buying a resale flat on the open market to live with or close to their parents and/ or married children.

What type of flat can I buy to be eligible for the PHG?

| Household | Flat Type* |

| Married couples and families | Any resale flat |

| Single citizens living near parents | 2 to 5-room resale flat |

| Singles citizens living with parents | Any resale flat |

* The flat needs to have a remaining lease at least 20 years.

How much grant can I get with the PHG?

| Household | To live with parents/ child | To live near parents/ child (within 4km) |

| Married couples/ families | $30,000 | $20,000 |

| Singles citizens | $15,000 | $10,000 |

Any other grants I could be eligible for?

- Family Grant

- Singles Grant

- Enhanced CPF Housing Grant

Read here for more details on the PHG.

5. Step-Up CPF Housing Grant

Who is eligible for the Step-Up CPF Housing Grant? What type of flat can I buy to be eligible for the Step-Up CPF Housing Grant?

You may apply for this grant if you currently own a 2-room subsidised flat in a non-mature estate and are applying to upgrade to a subsidised 3-room flat in a non-mature estate.

Second-timer families who are rental tenants may also be eligible for the grant if they buy a 2- or 3-room flat in a non-mature estate.

How much grant can I get with the Step-Up CPF Housing Grant?

$15,000

6. Half Housing Grant

Who is eligible for the Half Housing Grant?

Couples comprising a first-timer citizen applicant and second-timer applicant, with an average gross monthly household income of less than $14,000, and buying a resale flat on the open market, may apply for the Half-Housing Grant.

What type of flat can I buy to be eligible for the Half Housing Grant?

2-room or bigger resale flats with a remaining lease of at least 20 years.

How much grant can I get with the Half Housing Grant?

The quantum of the Half Housing Grant is half that of the Family Grant.

| Flat type | Grant amount |

| 2- to 4-room resale flat | $25,000 |

| 5-room or bigger resale flat | $20,000 |

Do remember that if you sell your flat that was purchased with the help of CPF grants, all CPF monies used will be returned to your CPF Account – so you can use it for your next housing purchase, or retirement and healthcare needs!

Source: mynicehome.gov.sg