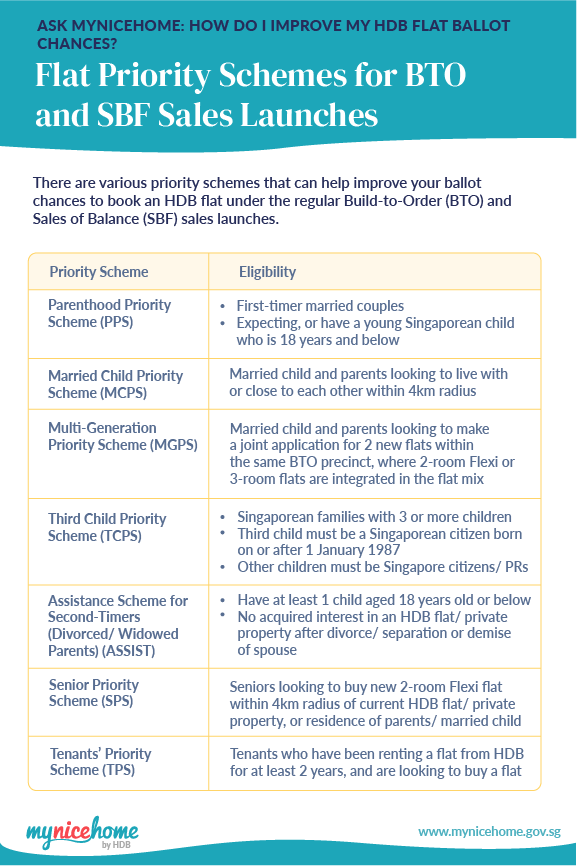

First-timers and those with pressing housing needs enjoy priority schemes that can improve your chances of getting balloted to book an HDB flat under the regular Build-to-Order (BTO) and Sales of Balance (SBF) sales launches. Learn more about HDB’s 7 priority schemes here!

Parents

Parenthood Priority Scheme (PPS)

First-timer married couples who are expecting, or have a young Singaporean child who is 18 years and below, will benefit from the Parenthood Priority Scheme (PPS). Up to 30% of BTO units and 50% of SBF units are allocated to applicants under this scheme.

Third Child Priority Scheme (TCPS)

Even better news for those with more kids – families with 3 or more children will enjoy priority under the PPS as well as the Third Child Priority Scheme (TCPS). Up to 5% of BTO/ SBF units are allocated under the TCPS.

Your application will first be balloted with other TCPS applicants. If that ballot is unsuccessful, your application will be balloted again under the PPS.

Assistance Scheme for Second-Timers (Divorced/ Widowed Parents) (ASSIST)

Under the Assistance Scheme for Second-Timers (ASSIST), up to 5% of 2-room Flexi and 3-room BTO flats in non-mature estates will be set aside for divorced or widowed parents with children aged 18 years old and below. This quota is shared with the 30% quota set aside for second-timer applicants.

Couples/ families wanting to live near or with their parents

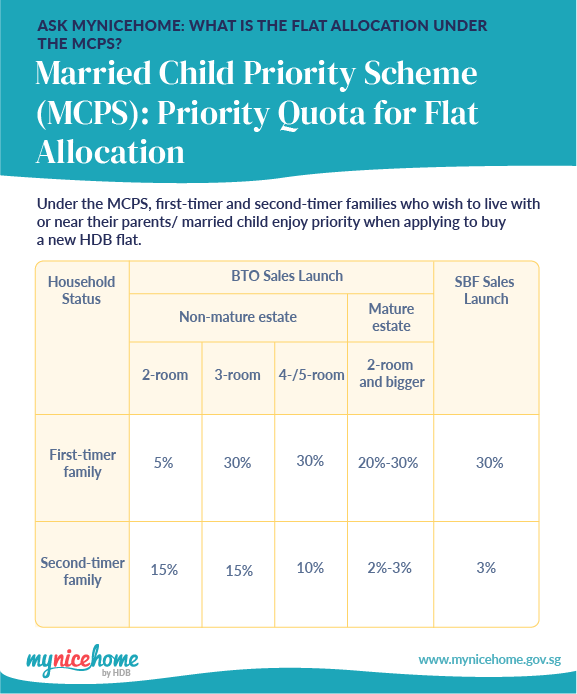

Married Child Priority Scheme (MCPS)

Keen to move out to your own place, but want to keep your family close? The Married Child Priority Scheme (MCPS) improves ballot chances for new flat buyers who wish to live with or near their parents for mutual care and support.

You will qualify for the MCPS, as long as your new flat is a within 4km radius of your parents’ HDB flat or private property. Engaged couples, or parents looking to stay with or near their married child are also eligible to apply for the MCPS!

The following table summarises the quota of flats given priority under the MCPS in each new project:

Multi-Generation Priority Scheme (MGPS)

For married children wanting to live even closer to your parents, consider applying under the Multi-Generation Priority Scheme (MGPS)! This scheme allows you to submit a joint application for 2 flats in a single BTO project, increasing the ballot chances of both parties to stay within the same precinct and even on the same floor! A 60-year-old couple shares their story of purchasing a BTO flat under MGPS to be closer to family here.

Note that parents applying for a flat under MGPS would be eligible to apply only for a 2-room Flexi or 3-room flat.

Senior Priority Scheme (SPS)

The Senior Priority Scheme (SPS) supports elderly residents who wish to live near your married child i.e. within 4km radius from the HDB flat or private property that they reside in.

The SPS also applies to elderly residents looking to buy a new 2-room Flexi flat to age-in-place within a familiar environment i.e. within 4km radius of your current flat or private property.

At least 40% of the 2-room Flexi flats for each BTO project offered during HDB sales launches will be set aside for elderly applicants. Half of this quota i.e. 20% will be set aside for eligible elderly under the SPS.

Tenants of HDB rental flats

Tenants’ Priority Scheme (TPS)

Many rental tenants progress to owning a home . If you have been renting a flat from HDB for at least 2 years, and are looking to buy a flat, you can apply for a 2-room Flexi and 3-room BTO and SBF flats set aside under the Tenants’ Priority Scheme.

Download and share this infographic on HDB’s flat priority schemes, or visit the HDB InfoWEB for more details to improve your chances at the ballot. May the odds be in your favour!

5 Things to Know About the Community Care Apartments

Community Care Apartments (CCA) are public housing jointly developed by the Ministry of National Development (MND), Housing & Development Board (HDB) and Ministry of Health (MOH). The CCA combine senior-friendly housing with care services, offering an option for seniors to age in-place and independently in a community setting.

The first batch of CCA, which will be in Bukit Batok, was launched in February 2021. Seniors can look forward to the second batch of CCAs in Queenstown, to be launched later this year.

Harmony Village @ Bukit Batok

If you or your family members are looking to apply for a CCA, here are 5 key things to note.

1. Wide Range of Facilities and Amenities

The upcoming CCAs will be situated within the Health District @ Queenstown. There, HDB will work with partners to create a built environment conducive for healthy living and active ageing. There will be common facilities such as roof gardens, fitness stations, and community living rooms to promote social interactions between all residents. With Alexandra Hospital nearby, residents will have easy access to healthcare and medical services.

The first batch of CCAs is located at Bukit Batok West Avenue 9, close to parks such as Little Guilin, Bukit Batok Nature Park and Bukit Batok Central Park. Besides shopping malls and wet markets, there are also several healthcare facilities nearby, including Bukit Batok Polyclinic, St. Luke’s Hospital and Ng Teng Fong General Hospital. Within the development, residents have convenient access to an activity centre, a community garden, and fitness stations to maintain an active lifestyle. The CCA development will also house a hawker centre offering a variety of affordable food options.

2. Minimal to No Renovation Required

Interested seniors would be glad to know that little to no renovation is required for these units! Each 32sqm CCA unit adopts an open layout, with sliding partitions to separate the living room and bedroom for greater privacy.

Each unit comes with built-in wardrobes, cabinets and a furnished kitchen

The flat also comes ready with senior-friendly design features and other pre-installed fittings, including:

Wide wheelchair-friendly main door with a built-in bench at the side

Large wheelchair-accessible toilet with grab bars and slip-resistant flooring

Built-in wardrobe and cabinets

Furnished kitchen (without fridge and washing machine)

Service yard accessible from toilet, with clothes drying rack

Wheelchair-friendly bathrooms are outfitted with grab bars and slip-resistant

On each floor of the CCA block, there will also be a furnished communal space for residents to mingle, share meals and take part in group activities.

Residents can connect with each other at the communal space located at every floor of the CCA block

3. Integrated Care Services

Care services are provided at the CCA to meet seniors’ needs, to support independent living within a social setting for an enriching retirement life.

Residents will have to subscribe to a Basic Service Package. The package offers 24-hour emergency monitoring and response, basic health checks, and the service of an on-site community manager who will organise regular activities and programme for the residents. The community manager will also ensure that the following services are provided:

Care and support services

Simple home fixes

Activities at the communal spaces

Key card access to individual flats

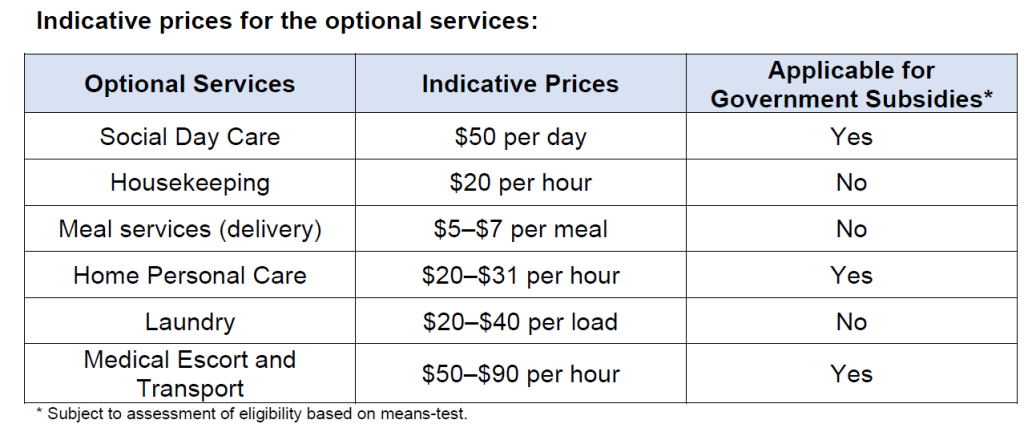

Depending on their needs and preferences, seniors can also choose to add on optional services that cover different activities in day-to-day living.

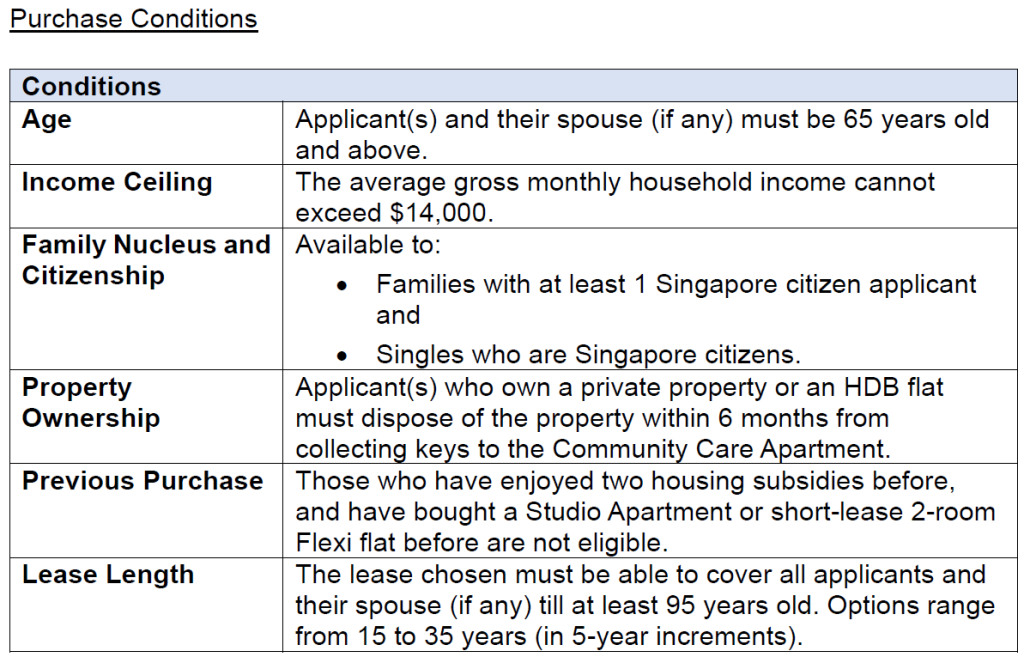

4. Eligibility Conditions

As the CCA is intended as an affordable housing option for seniors, the applicant(s) and their spouse (if any) must be 65 years old and above. Applicants have the flexibility to choose a lease ranging from 15 to 35 years (in five-year increments), as long as it covers both the applicant and their spouse (if any) until at least 95 years old.

Those who have taken up housing subsidies twice, and have bought a Studio Apartment or short-lease 2-room Flexi flat before are not eligible to purchase a CCA.

Here’s a quick summary of the eligibility conditions:

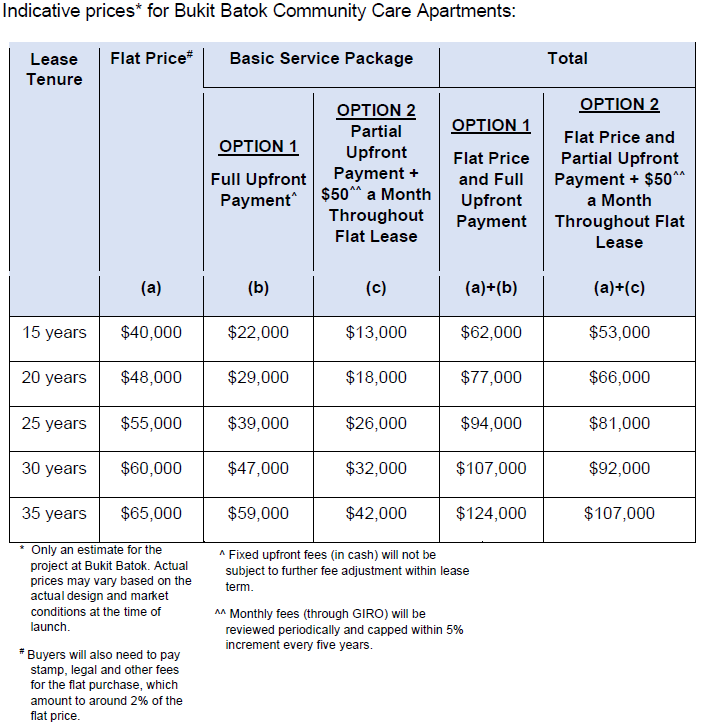

5. Full Upfront Payment for Flat Purchase

Successful applicants for CCA are required to make full upfront payment for the flat by cash and/or CPF. For the mandatory Basic Service package, applicants can decide to make either full or partial upfront payment in cash, with a monthly fee throughout the lease term.

This is illustrated in the indicative prices for the CCA at Bukit Batok:

Using the 15-year lease tenure as an example, an applicant has 2 payment options.

While both options require full upfront payment of $40,000 for the flat itself, the applicant may choose either to pay $22,000 upfront (Option 1) for the Basic Service Package, or make partial upfront payment of $13,000 (Option 2) with the remaining fees to be paid monthly. If partial payment is chosen, the applicant would have to pay an estimated $50 per month throughout the remaining lease tenure of 15 years.

Another key difference between a CCA unit and other HDB flats is that it cannot be resold or rented out. Owners who do not require the CCA anymore can return it to HDB. They will receive a refund of the value of the remaining lease of the flat.

Another is more flats reaching their MOP, as these newer flats may command higher prices than older flats in the same location.

One phenomenon we’ve noticed is an increasing number of million-dollar HDB flats. Though they are only a fraction of the total HDB transactions, they’ve received a lot of attention.

Many of our readers have asked us whether it’s a good idea to buy these flats.

Here are my thoughts on why I (Ruiming) am strategically not inclined to buy one. And why this might apply to you.

Just to be clear: We’re not saying you SHOULDN’T buy a million-dollar HDB flat. Some people might have reasons for buying these flats, we’ll explain this later.

What makes a million-dollar flat?

A million-dollar resale HDB flat would typically have a few main qualities that allow it to command its hefty price tag.

The more of these qualities it has, the more likely it’ll reach the magical $1,000,000 price tag and beyond.

Size: The larger the flat, the more expensive it will be. This gives flats in less popular areas the ability to command higher prices. The recently sold jumbo flat in Yishun is one example.

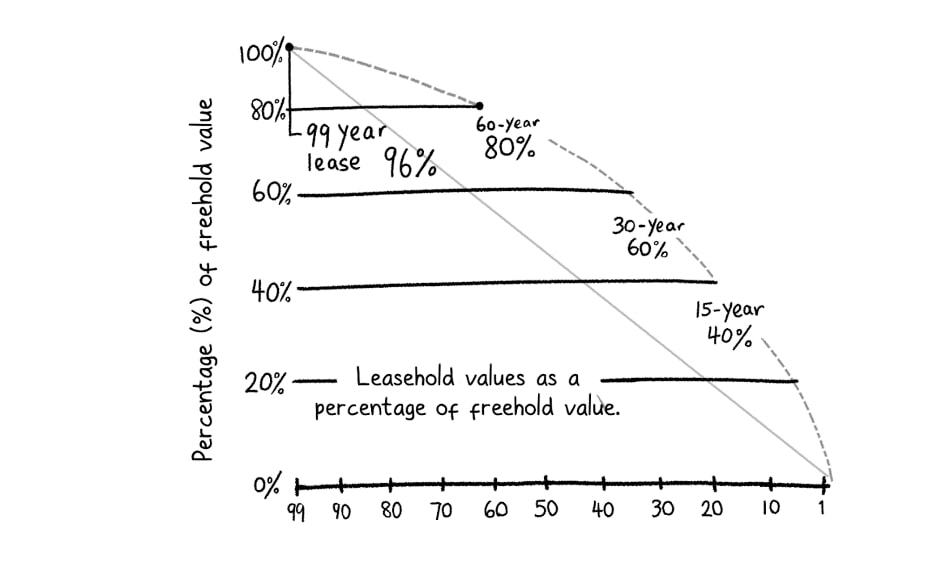

Lease: Generally, the newer the flat, the more expensive it will be, and vice versa. The Singapore Land Authority (SLA) has a rough guide known as ‘Bala’s Table’, which kinda shows how property prices are affected by their lease.

Older flats also have a limited pool of buyers, because if the lease of the HDB flat doesn’t last the youngest buyer till 95, there will be limitations on how someone’s CPF can be utilised.

Why is understanding Location, Size and Lease important?

Because these are effectively the trade-offs you have to make if you want to buy a home within your means.

Why you might not want a million-dollar flat

Why?

It’s for the simple reason that more money spent on my home means less money elsewhere. As the saying goes, every decision for something is a decision against something else.

These are some things I’d keep in mind while buying a home.

Financial security:

Buying an affordable home means financial security during turbulent times.

If history serves as a guide, our adult lives – like our parents’ – will have its share of economic highs and lows. This could mean times of unemployment and uncertainty.

By buying a flat well within your means, you’ll need to worry less about your mortgage in bad times.

While millennials have only known the era of low interest rates, it’s important to remember this isn’t always the case. Singapore Interbank Offered Rate (SIBOR) actually hit interest rates of 3.56% in 2006, and home loans upwards of 7% during the late 1990s.

Case in point: Some readers who’ve signed up for floating mortgages during the pandemic are beginning to worry about interest rate hikes. They should. Paying 3.85% vs 1% interest on a six-digit loan definitely adds up!

Also, despite recent events, it would be wise to remember that prices of HDB flats don’t go up all the time.

From 2013 – 2019, both public and private property priceswere on the decline. The same can be said for the late 1997, where the HDB resale index fell by almost 30%, and only recovered in 2008.

Those who’re thinking of treating their flat like an investment, take note!

Don’t pay *too much* for centrality and convenience

“Time is money.

So, if you’re financially savvy, shouldn’t the smart thing be to save time, by living in a mature, central location closer to the CBD?”

This is something people often say to us when we advocate buying a more affordable but less centrally located home.

While I see the logic, perhaps it’s worth considering the following points:

More centrality and convenience always costs more. This is the same whether you’re in London, Tokyo, Paris, or Melbourne. If you need to spend a lifetime working to pay this difference, it might not be worth paying for.

For example, it might make sense for a couple earning a combined income of $20,000 to buy a $900,000 flat in a central location to save time. They can comfortably afford the payments, and it makes sense to reduce their commute time.

However, if you need to borrow money from your parents, or look for ways to get around the loan limits offered by financial institutions, it’s usually a sign you cannot afford the convenience you desire.

Not all workplaces are in the CBD. There are many smaller commercial centres around the island. Jurong East, Paya Lebar, Changi, One-North etc. Even if you work in the CBD, with flexi-work arrangements you might go into the office less and less.

If you intend to buy a car or a motorcycle/scooter (like many people do), then centrality might not matter as much. You are effectively already paying for convenience when you decide to own private transportation.

Finally, in places not as well served by public transport, some creativity can go a long way. Speaking from first-hand experience, I’ve found that using a bicycle can often help you get to your destination faster if it’s less than 10 km away. Otherwise, you can still use a bike to cover that last mile to the MRT station.

If you are able to make this lifestyle change and your workplace is supportive, you might not need to fork out hundreds and thousands of dollars for that unit in a central location.

Paying for space you don’t use:

As someone who might not have lots of kids (or even remain child-free), a large flat is wasted on me (and by extension, I’ll be wasting money on a larger flat).

Sure, having more space is always a luxury in land-starved Singapore. Or any city.

The question is whether it makes financial sense.

Don’t get me wrong; I like to have enough personal space. But not at the expense of my freedom to do other things.

For reference: I currently rent a 3-room HDB flat with my girlfriend that’s about 700 sq ft. It’s serviceable, though I certainly could be happier with 900 sq ft.

Do you have enough for other life goals?

A roof over your head is important. But I dare reckon that it won’t be the only aspiration you have in life.

My own personal goals include:

Experience working overseas at some point in life ($200,000 for living expenses) / be a digital nomad

Embark on a year-long cycling trip ($100,000)

Be able to choose to do a job that I like (have a passive income of at least $2,000 a month)

If I spend too much on a house, these goals will remain just that – dreams. Every single extra dollar spent here moves me further away

from reaching these goals.

Mind you, even if you do not know what your other life goals are, I think it doesn’t hurt to be cautious about overpaying for a home. The home you buy can limit the dreams you can chase.

So if you’re considering buying a million-dollar flat, weigh the opportunity costs of spending that sum on housing and ask yourself if you can live with the trade-off.

So why do people buy million-dollar flats?

I’m just going to say it: I think buying a million-dollar flat is a bad idea for the median-income Singaporean because of budget constraints.

That being said, above-median-income Singaporeans do exist. They can afford these expensive flats, and find them attractive despite the price tag.

Consider this: A million dollars for an HDB flat is certainly a lot of money, but to get a condominium of equivalent size at a comparable location will cost at least 3-5 times more!

In such scenarios, buying a million-dollar HDB flat may be more appealing despite the lack of private facilities.

Yes, there is little question it’s a seller’s market right now. And will be for a while. Be prepared to pay more than pre-pandemic times.

However, what is also true is that there are many choices on the resale market.

The cheapest HDB flat on PropertyGuru is asking for $250,000 as of the writing of this article. The most expensive one? An eye-popping $1.65 million.

Our advice? Calculate what you can afford first above all else. Use your judgement to determine whether the seller’s asking prices are reasonable.

If you want to be extra safe, buy something below your means.

Otherwise, for peace of mind, buy something within your means.

And unless you want to spend the foreseeable future stressing about paying your mortgage, never spend beyond your means.

Stay woke, salaryman

A message from our sponsor, HDB

There are many factors that come into play when looking for a new home – the location, proximity to loved ones and amenities, size and more.

But amongst all of these, affordability is one of the key factors in making a housing decision. After all, housing would likely be one of your first biggest ticket purchases, so it’s important that your future home fits your budget and your needs.

If you’re looking for a new home, check out the guides, articles and resources available on MyNiceHome.

Also, check out past content pieces we’ve developed with HDB to navigate through your home-buying decision: