A Guide to Prime Location Public Housing (PLH)

A Guide to Prime Location Public Housing (PLH)

HDB will be building new public housing in prime, central locations like the city centre and the Greater Southern Waterfront. These flats will be sold under a new housing model called the Prime Location Public Housing (PLH) model.

What is PLH?

The Prime Location Public Housing (PLH) model is a public housing model that aims to keep HDB flats in prime, central locations affordable, accessible, and inclusive for Singaporeans.

This model was developed after considering feedback from the public—more than 7,500 Singaporeans, including academics and industry experts, shared their views on the model over almost a year.

Which areas will this new public housing model apply to?

The PLH model will apply for selected public housing projects in prime and central locations like the city centre and surrounding areas, including the Greater Southern Waterfront. The PLH model will not be retrospectively applied to existing flats.

What are the HDB flat types available for PLH flats?

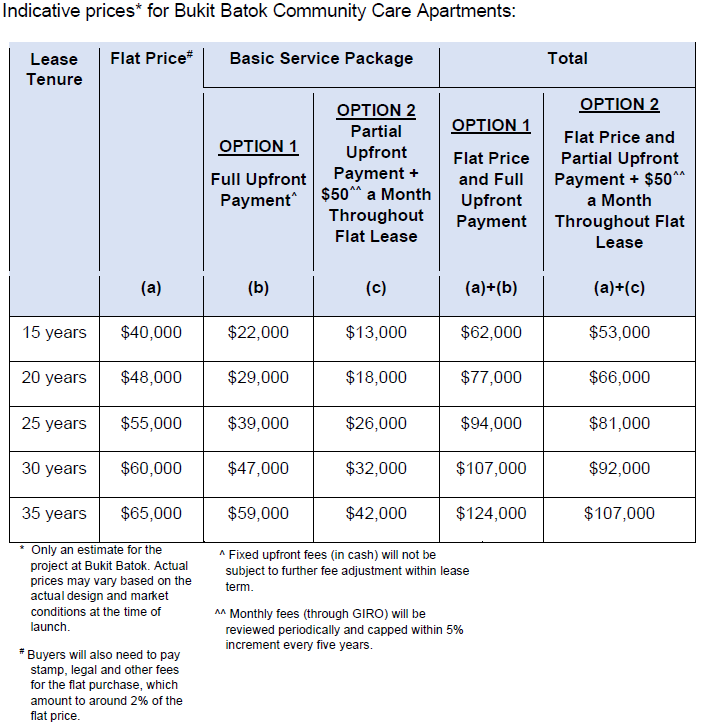

About 960 units of 3-room and 4-room flats will be offered for sale in the first project to be launched under the PLH model at Rochor. The project will also include 40 units of 2-room rental flats.

Will there be additional subsidies for prime location flats?

New PLH flats are priced with additional subsidies, on top of the substantial subsidies already provided for BTO flats today. These additional subsidies keep PLH flat prices affordable for a wide range of Singaporeans.

When PLH flat owners sell their homes, they will pay to HDB a percentage of the resale price of the flat, commensurate with the extent of the additional subsidy provided. This is to be fair to other BTO flat owners who do not receive these additional subsidies. For the pilot projects, River Peaks I and II, this amount is fixed at six percent of the higher of the resale price or valuation.

All prevailing grants such as the Enhanced CPF Housing Grant (EHG) of up to $80,000, will continue to apply for eligible families who buy a PLH flat.

What are the eligibility conditions for the purchase of prime location flats?

To buy a new PLH flat, you must meet the prevailing BTO eligibility conditions such as being a Singaporean household and meeting the household income ceiling, currently set at $14,000.

Beyond the initial purchase, subsequent flat buyers of resale PLH flats will also have to meet the prevailing eligibility conditions for the purchase of BTO flats. This helps to ensure that PLH flats remain inclusive and accessible to a broad group of subsequent flat buyers over time. Without these conditions, the resale prices of these prime location flats may rise beyond the reach of many Singaporeans; and over time only the better-off will be able to afford to buy them.

A summary of key eligibility conditions for purchase of 3-room and larger flats are below:

| Conditions | Flats bought from HDB and PLH resale flats * | Typical Resale Flats |

| Citizenship | At least one applicant is a Singapore Citizen (SC). Household must comprise at least one SC and one Singapore permanent resident (SPR). | At least one applicant is a SC or SPR. Household can comprise only SPRs. |

| Family Nucleus | Must have an eligible family nucleus, e.g. married couple. | Must have an eligible family nucleus; or if single, must be aged 35 and above. |

| Income Ceiling | $14,000^ | Not applicable |

| Private Property Ownership | Must not own or have an interest in a private property and have not disposed of any in the last 30 months. | Allowed, but must dispose of private property within 6 months of buying the resale flat. |

Note:

* With or without CPF housing grants.

^ Or $21,000 if purchasing with extended/multi-generation family.

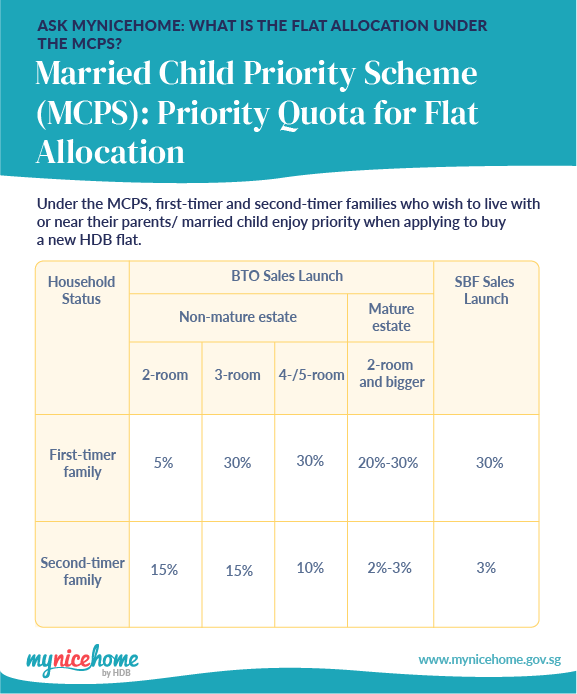

Will there be flats set aside for priority allocation under the Married Child Priority Scheme?

Yes, flats will continue to be set aside for those applying under the Married Child Priority Scheme (MCPS). The priority quotas will be adjusted for individual PLH projects, to provide opportunities for Singaporeans whose family members do not live nearby, to also live in prime areas.

How long will I need to live in the PLH flat before I can sell it? Will I be able rent out spare bedrooms or the whole flat?

Given the prime locations and additional subsidies provided for PLH flats, PLH flat owners will need to live in their flats for at least 10 years before they can sell them on the open market or invest in a private residential property. This measure helps to safeguard PLH flats for families with genuine housing needs and discourage speculation.

While owners of PLH flats may rent out spare bedrooms, renting out of whole flats is not allowed, even after MOP.

| Conditions | BTO Model | PLH Model |

| Resale of flat | Allowed after MOP* | Allowed after MOP^ |

| Renting out of spare rooms | Allowed | Allowed |

| Renting out of whole flat | Allowed after MOP* | Not allowed |

| Investment in private property | Allowed after MOP* | Allowed after MOP^ |

Note:

* MOP is five years.

^ MOP is ten years.