Thinking of buying your first HDB flat soon? Before you apply for a new flat in our sales launch exercises or look for a resale flat, you should be savvy and plan your finances first. The Woke Salaryman shares 5 tips on how you should plan for your finances for an HDB flat purchase:

Planning to buy a flat at one of HDB’s sales launches, and working out the math for your future home? Besides the purchase price of the flat, there are other costs and fees that you will need to pay at various stages of your flat buying journey. But don’t sweat it – check out our simple guide below!

Booking Your Flat

When you book your flat, you will need to pay the option fee, which varies based on the type of flat you’ve booked:

Flat Type

Option Fee

4/ 5-room and Executive Flat

$2,000

3-room

$1,000

2-room Flexi flat

$500

The good news is that the option fee is considered as part of your downpayment, which you have to pay when you sign the Agreement for Lease.

Signing of Agreement for Lease

Besides the downpayment for your flat, you will need to pay stamp duty and legal fees. Basically, you pay HDB to act as your solicitor in the purchase and/or mortgage of your flat. In contrast, for other property transactions, you would typically get a private solicitor to act on your behalf.

You can use IRAS’ handy Stamp Duty Calculator to calculate your stamp duty. For conveyancing fees, the rates are:

First $30,000: $0.90 per $1,000

Next $30,000: $0.72 per $1,000

Remaining Amount: $0.60 per $1,000

The minimum legal fee chargeable is $20, and it is subject to GST.

Key Collection

You’re now on the home stretch (pun intended)! Besides paying the balance of the flat purchase price, you will also need to pay stamp duty and legal fees. Yes, again, but this time it includes the following – depending on whether HDB acted for you in the purchase and/or mortgage of your flat:

Survey fee: $150 to $375, depending on flat type

Lease In-Escrow fee: Fixed at $38.30

Mortgagee solicitors’ bill (only payable if you are taking a housing loan from a financial institution)

You will also need to pay for the Home Protection Scheme (HPS), a mortgage-reducing insurance scheme offered by the CPF Board. Note that you must be insured under the HPS if you want to use your CPF OA to pay off your mortgage.

In the event of permanent disability or death before you turn 65, the CPF Board will pay the outstanding housing loan amount, based on the amount insured under HPS. You can pay the annual premiums using either your CPF savings or cash, and you can estimate your premium amount using CPF Board’s calculator. For more on the HPS, check out the CPF Board website.

Finally, if you’re taking a housing loan from HDB, you must buy fire insurance from HDB’s appointed insurer, FWD Singapore Pte Ltd. The coverage and premiums vary based on flat type – for more details, visit FWD’s website.

HDB has recently launched the Flat Portal, a one-stop portal that streamlines the process of buying and selling flats. Beyond flat listings and details on BTO projects in current and upcoming Sales Launches, customised financial calculators can also be used for budget and payment planning. Additionally, home buyers can also get information on housing loans offered by HDB and participating financial institutions.

Buying a flat is a big financial commitment, so you might be glad to know that there are several housing grants available to help you offset the purchase price of the flat and embark on your home ownership journey.

Do you know which grants you’re eligible for, or how much you can get? Here’s a handy guide that breaks down all you need to know about housing grants.

1. Enhanced CPF Housing Grant (EHG)

Who is eligible for the EHG?

First-timer citizen households and first-timer single citizens can apply for the EHG when buying a new flat from HDB or resale flat on the open market, subject to prevailing eligibility conditions. Resale flat buyers must qualify for the Family Grant or Singles Grant (whichever is applicable) to be considered eligible for the EHG.

If you’re buying a flat as a first-timer family, your average gross monthly household income must not exceed $9,000. If you’re a first-timer single, your average gross monthly income must not exceed $4,500.

What are the flat types eligible for EHG?

Generally, the EHG is applicable to both new and resale flats, for all flat types and locations. However, for first-timer single citizens, the applicable flat type would depend on the eligibility scheme and whether you are buying a new flat or resale flat. Do note though that the flat needs to have a remaining lease of at least 20 years.

How much grant can I get with the EHG?

Household Type

Grant Quantum*

Eligible first-timer households

Up to $80,000, depending on household income

Eligible first-timer single citizens

Up to $40,000, depending on household income

*The flat must have sufficient lease to cover the youngest buyer to the age of 95 –otherwise, the EHG will be pro-rated

You may be eligible if you’re a first-timer household buying a resale flat on the open market, and your average gross monthly household income does not exceed $14,000.

What type of flat can I buy to be eligible for the Family Grant?

2-room or bigger resale flat with a remaining lease of at least 20 years.

How much grant can I get with the Family Grant?

Household

2- to 4-room Resale Flat

5-room or Bigger Resale Flat

Comprising two Singapore Citizens

$50,000

$40,000

Comprising a Singapore Citizen and Singapore Permanent Resident**

$40,000

$30,000

** May later be eligible for the Citizen Top-Up – a $10,000 housing subsidy – when a qualifying household member becomes a Singapore Citizen

If you’re a first-timer single Singapore Citizen (35 years old and above) buying a resale flat with average monthly household income not exceeding $7,000, you may be eligible!

What type of flat can I buy to be eligible for the Singles Grant?

2-room to 5-room resale flat, with a remaining lease of at least 20 years.

Who is eligible for the Step-Up CPF Housing Grant? What type of flat can I buy to be eligible for the Step-Up CPF Housing Grant?

You may apply for this grant if you currently own a 2-room subsidised flat in a non-mature estate and are applying to upgrade to a subsidised 3-room flat in a non-mature estate.

Second-timer families who are rental tenants may also be eligible for the grant if they buy a 2- or 3-room flat in a non-mature estate.

How much grant can I get with the Step-Up CPF Housing Grant?

$15,000

6. Half Housing Grant

Who is eligible for the Half Housing Grant?

Couples comprising a first-timer citizen applicant and second-timer applicant, with an average gross monthly household income of less than $14,000, and buying a resale flat on the open market, may apply for the Half-Housing Grant.

What type of flat can I buy to be eligible for the Half Housing Grant?

2-room or bigger resale flats with a remaining lease of at least 20 years.

How much grant can I get with the Half Housing Grant?

The quantum of the Half Housing Grant is half that of the Family Grant.

Flat type

Grant amount

2- to 4-room resale flat

$25,000

5-room or bigger resale flat

$20,000

Do remember that if you sell your flat that was purchased with the help of CPF grants, all CPF monies used will be returned to your CPF Account – so you can use it for your next housing purchase, or retirement and healthcare needs!

Are you looking to buy a resale HDB flat but unsure of how the entire journey is like? Here’s a 5-step guide on how you can purchase a resale flat from the open market.

1. Check Your Eligibility

Before you start the process, first check if you are eligible to purchase a resale flat. Register your Intent to Buy through theHDB Resale Portal to receive an instant assessment on your eligibility to buy a resale flat. The Portal will also automatically retrieve and populate your particulars from the Government’s MyInfo service.

Now that you’ve done the necessary checks and financial planning, it’s time to look for an HDB flat that meets your budget and needs. You can engage a property agent to assist you in the search, or trawl property sites to shortlist suitable ones.

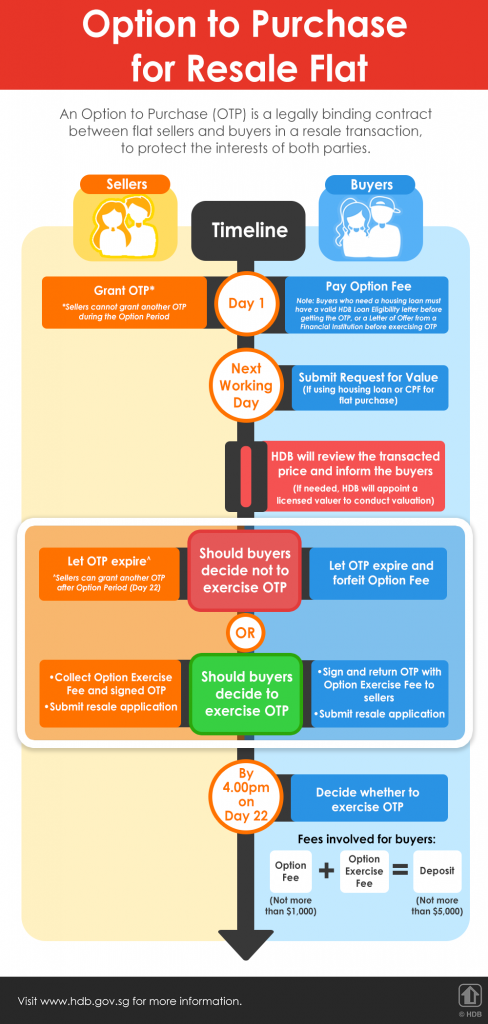

4. Obtain an OTP from the Seller

Once you have decided on the resale flat that you would like to purchase, you need to obtain an Option to Purchase (OTP) from the seller via the HDB Resale Portal. After the seller grants you an OTP, a Request for Valuation will be submitted to HDB. Following the valuation report, you (flat buyers) will have to decide whether to exercise the OTP.

5. Submit Resale Application

Should you decide to exercise the OTP, both you and the seller must submit the respective portions of the resale application on the HDB Resale Portal. HDB will then contact both parties to come down to HDB Hub to attend a resale completion appointment, to endorse documents which require ‘wet-ink’ signatures.

There you have it – you are 5 steps closer to getting a resale flat of your own!

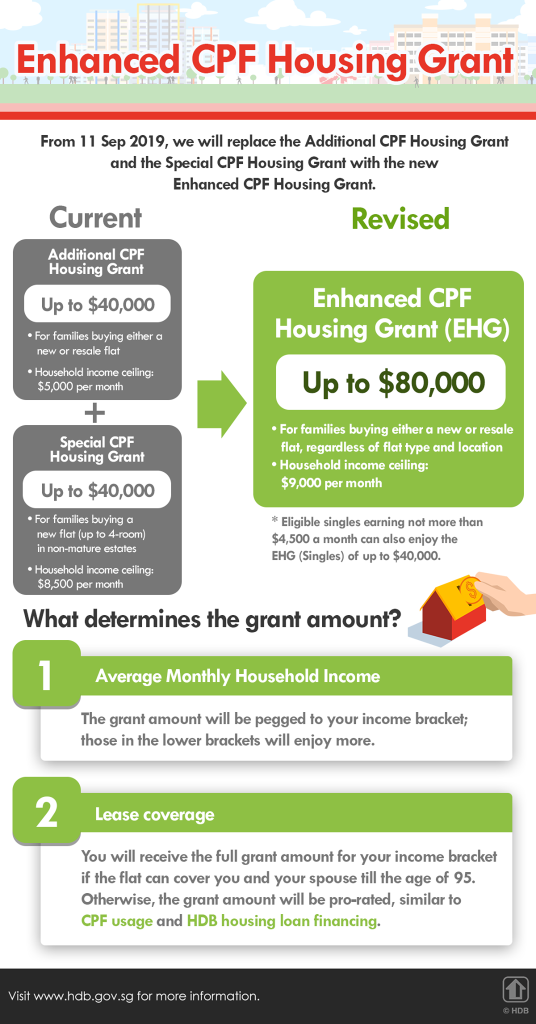

To make housing more affordable and accessible to Singaporeans, eligible first-time flat buyers can apply for an Enhanced Housing Grant (EHG) of up to $80,000.

What is EHG?

The EHG is a CPF housing grant for first-time flat buyers applying for a new Build-To-Order (BTO) flat or buying a resale flat in the open market. It helps to make housing more affordable and accessible to Singaporeans.

How much EHG am I eligible for?

Eligible first-timer applicants for new flats can enjoy an EHG of up to $80,000, while eligible first-timer singles can enjoy an EHG (Singles) of up to $40,000.

Similarly, eligible first-timer households buying a resale flat can also enjoy an EHG of up to $80,000, in addition to the CPF Housing Grant (up to $50,000) and Proximity Housing Grant (up to $30,000). This means that first-time resale homebuyers can enjoy up to $160,000 in housing grants!

How does EHG work?

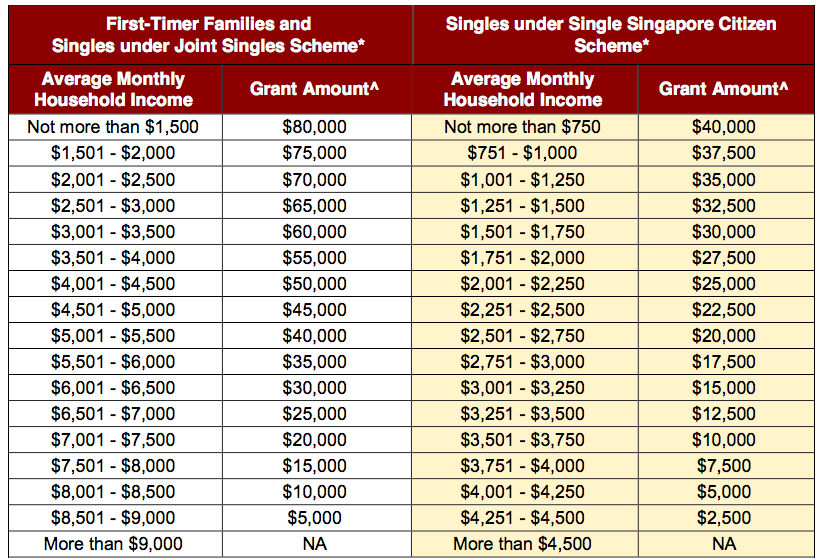

To qualify for EHG, the monthly household income for first-timer families should not exceed $9,000 (refer to Table 1 below). Eligible first-timer singles must be aged 35 and above, with a monthly income of less than $4,500. In both cases, the buyer or his/ her spouse must be in continuous employment for the 12 months prior to the date of flat application and remain working at the point of flat application.

Table 1: EHG Structure

*The EHG is applicable for those buying 2-room Flexi flats on 99-year leases in the non-mature estates, 2-room Flexi flats on short leases, and resale flats (up to 5-room under the Single Singapore Citizen Scheme, and all flat types under the Joint Single Scheme).

^The EHG amount is applicable to households buying a flat with a remaining lease that can cover the buyers and their spouses to the age of 95; otherwise, the household will enjoy a pro-rated EHG.

New Flat Applicants

For first-timer households*, the EHG is applicable for all flats, regardless of flat type and location.

*First-timer single citizens buying a flat under the Single Singapore Citizen scheme or Joint Singles Scheme, are only eligible to buy 2-room Flexi flats.

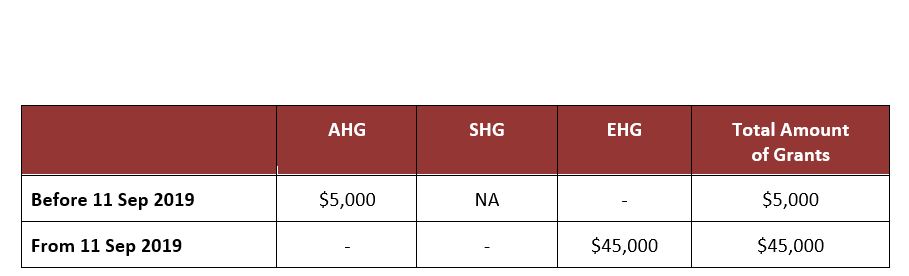

For example, Couple A has an average monthly household income of $4,800 and is looking to buy a 4-room BTO flat in Tampines, a mature estate. With the EHG, Couple A can enjoy an additional $45,000 in housing grants:

Example 1

Resale Flat Buyers

Eligible first-timer households buying a resale flats can enjoy up to $160,000 in housing grants, which includes the EHG (up to $80,000), CPF Housing Grant (up to $50,000) and PHG (up to $30,000).

For example, Couple B who are both Singapore Citizens with an average monthly household income of $4,800, is buying a 4-room flat in a mature estate to live near their parents. They can enjoy a CPF Housing Grant of $50,000, an EHG of $45,000 and Proximity Housing Grant (PHG) of $20,000.

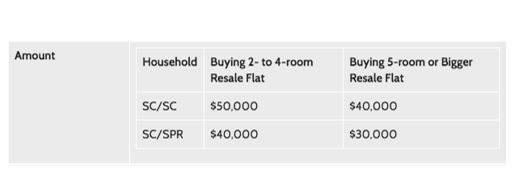

Table 2: CPF Housing Grant

Table 3: Proximity Housing Grant

What happens if the remaining lease of the flat I buy does not cover the youngest owner till the age of 95?

To enjoy the full EHG amount for the relevant income brackets, the purchased flat must have sufficient lease to cover the buyers and their spouses to the age of 95. Otherwise, the amount of grant will be pro-rated. This condition also applies to repurchased flats under the Sales of Balance Flats or Re-Offer of Flats exercises.

For example, Couple C, both aged 30, with an average monthly household income of $4,800, has purchased a resale flat with a remaining lease of 60 years. As the flat cannot cover them to the age of 95, they can enjoy an EHG of $40,000 as opposed to the full EHG amount of $45,000 for their income bracket.

In a Nutshell

Eligible first-timer applicants for new flats can enjoy up to $80,000 in housing grants while eligible first-timer singles can enjoy an EHG (Singles) of up to $40,000.

For eligible first-timer households buying a resale flat, they can enjoy up to $160,000 in housing grants, which includes the EHG (up to $80,000), CPF Housing Grant (up to $50,000) and PHG (up to $30,000).

Whether you are applying for a new BTO flat or buying a resale flat, remember to factor in the EHG when planning for your new home!

Read this guide to learn about other CPF housing grants available for home buyers.

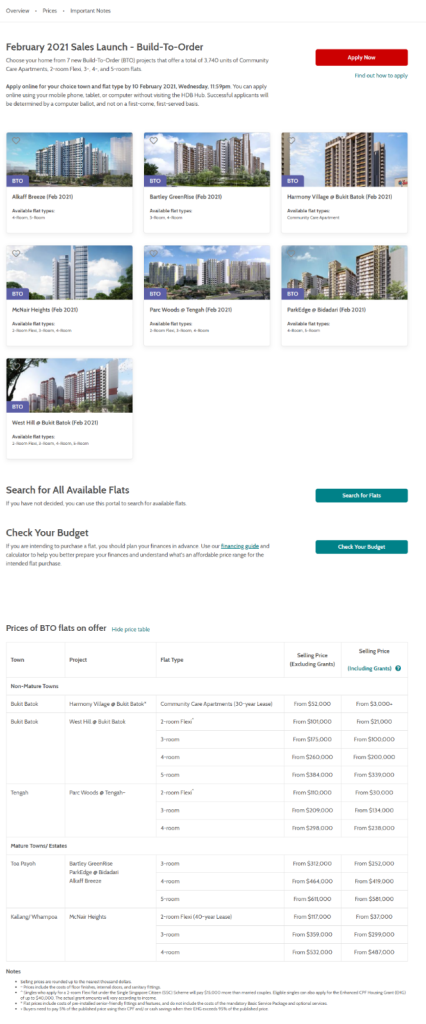

Thinking of applying for a BTO flat but don’t know where to start? Here is a step-by-step guide on the process, where we highlight the things you should note and share tips for each stage of the application process.

BTO flats are available for application quarterly. HDB will announce the exact application period on the day of the sales launch. So, be sure to follow MyNiceHome, to get first-hand details of the projects on offer!

You can also check out the HDB Flat Portal and HDB social media channels (HDB Facebook, MyNiceHome Facebook, Instagram & Telegram). In a typical sales launch, several projects will be launched and applicants will have one week to submit their application.

During a sales launch, you will see a banner (like the one pictured below) on the HDB Flat Portal. Click on it and it will lead you to a listing page with prices and information on the projects on offer. Be sure to go through the details and discuss the options with your spouse or co-applicant!

Homepage of the HDB Flat portal during Sales Launch

Pro tip: Plan your flat purchase by checking out the HDB Flat portal in advance. The portal lists BTO projects about 3 months ahead of the projects’ scheduled launch and you can find useful information such as the site map, flat types and number of units offered for each project.

Step 2: Check eligibility

Found a flat that you like? Check your eligibility before making an application. You can read the eligibility conditions below and visit HDB InfoWEB for more details.

Overview of eligibility conditions

Eligible Applicant/ Family Nucleus

• You will need to qualify for a new flat under one of our eligibility schemes:

Public Scheme

Fiancé/ Fiancée Scheme

Orphans Scheme

Citizenship

• At least 1 Singapore Citizen applicant

• At least 1 other Singapore Citizen or Singapore Permanent Resident

Age

• At least 21 years old

Incoming Ceiling

• You are within the set income ceiling for the flat you intend to buy

Property Ownership

• All applicants and occupiers listed in the flat application do not own other property overseas or locally, and have not disposed of any within the last 30 months

• All applicants and occupiers listed in the flat application cannot invest in private residential property from the date of flat application till after the 5-year Minimum Occupation Period (MOP)

• You have not bought a new HDB/ DBSS flat or EC, or received a CPF Housing Grant before; or, have only bought 1 of those properties/ received 1 CPF Housing Grant thus far

You should also ensure that you have sufficient funds to purchase the flat. Previously, this might involve visiting several websites and webpages, but HDB has made it easier by streamlining the information-gathering process on the new HDB Flat Portal. You can now work out the sums easily with the calculators on the Portal.

Step 3: Submit application

When submitting an online application, applicants will have to pay a non-refundable application fee of $10 via MasterCard/VISA. You have one week to submit your application, but there’s no need to rush as applications are not processed on a first-come-first-serve basis.

At the close of the application period, HDB will process the BTO applications using a computer ballot. This will determine your queue position to book a flat.

HDB will notify you via SMS, and/or email, on the outcome of your ballot in approximately 3 weeks after the close of application.

Pro tip: You can also visit HDB InfoWEB or log on to My HDBPage to check your application status.

Step 5: Book flat

If your application is successful, you will be invited to book a flat from 4 weeks after the release of the ballot results. Before you head down to HDB Hub at Toa Payoh for your appointment, be sure to have the required documents ready.

During the selection appointment, you will need to pay an option fee – this will form part of your downpayment for the flat purchase. The amount payable varies depending on the flat type. Payment has to be made via NETS.

Flat Type

Option Fee

4/5 room Executive

$2,000

3-room

$1,000

2-room Flexi

$500

If you are applying for the Enhanced CPF Housing Grant, you will need to submit the application formduring the appointment.

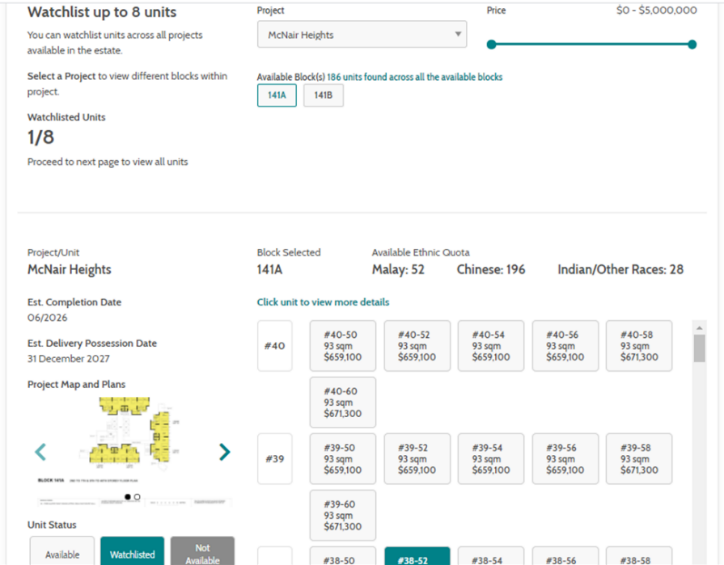

Pro tip: With the new HDB Flat Portal, you can create a watchlist of your preferred units and receive notifications if and when they have been booked by others.

Step 6: Sign Agreement for Lease

From 6 months after booking your flat, HDB will invite you to sign the Agreement for Lease. Ensure that you have the necessary documents with you.

This includes a valid Home Loan Eligibility Letter (HLE) from HDB if you are taking an HDB housing loan, or a Letter of Offer if you are taking a housing loan from a financial institution (FI).

You would also need to make a downpayment for your flat. The amount depends on the type of loan you are taking. For HDB Loan, it is 10% of the purchase price and it can be fully paid for using the CPF funds in your CPF ordinary account.

For a loan from an FI, it is 20% of the purchase price, of which at least 5% must be paid using cash and the remaining can be paid using your CPF savings.

As the maximum loan quantum granted by financial institutions is 75% of the purchase price, you will have to pay the balance 5% of the purchase price using cash or CPF savings when you collect the keys to your flat. The actual cash quantum would depend on the maximum loan ceiling.

For payment using CPF savings, you would need to access your Singpass and your mobile phone or OneKey token for 2-factor authentication. The registration for Singpass and activation of 2FA will take up to 10 working days. So be sure to prepare these in advance!

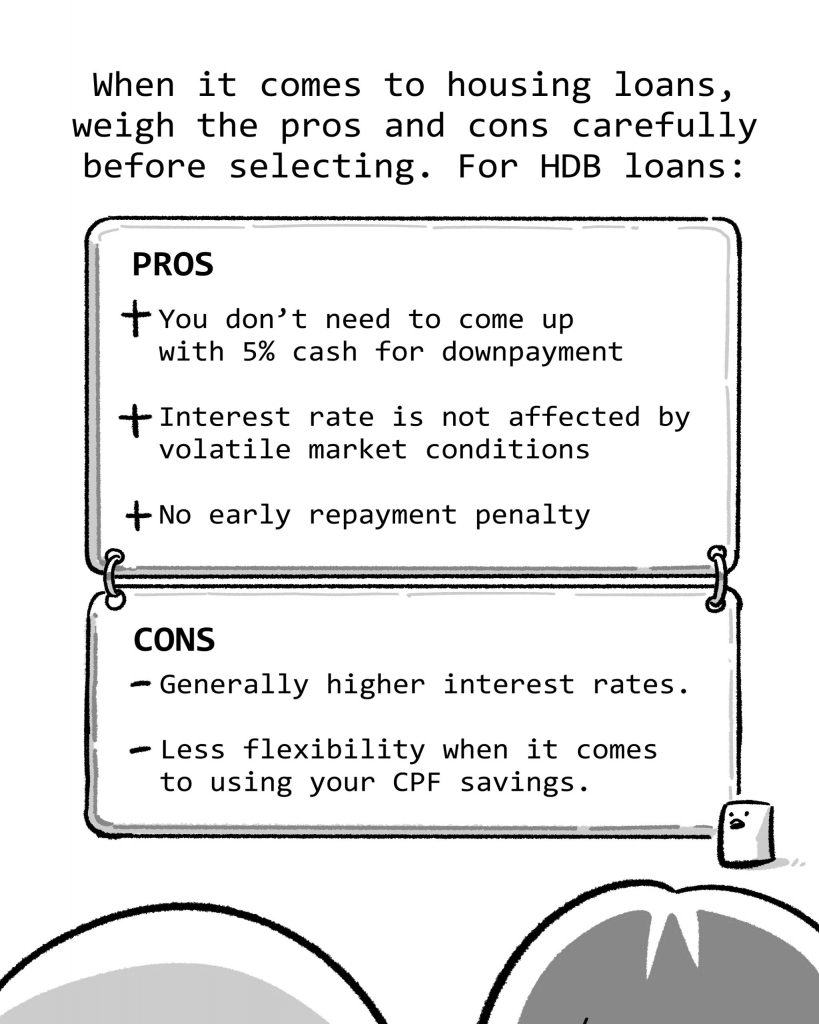

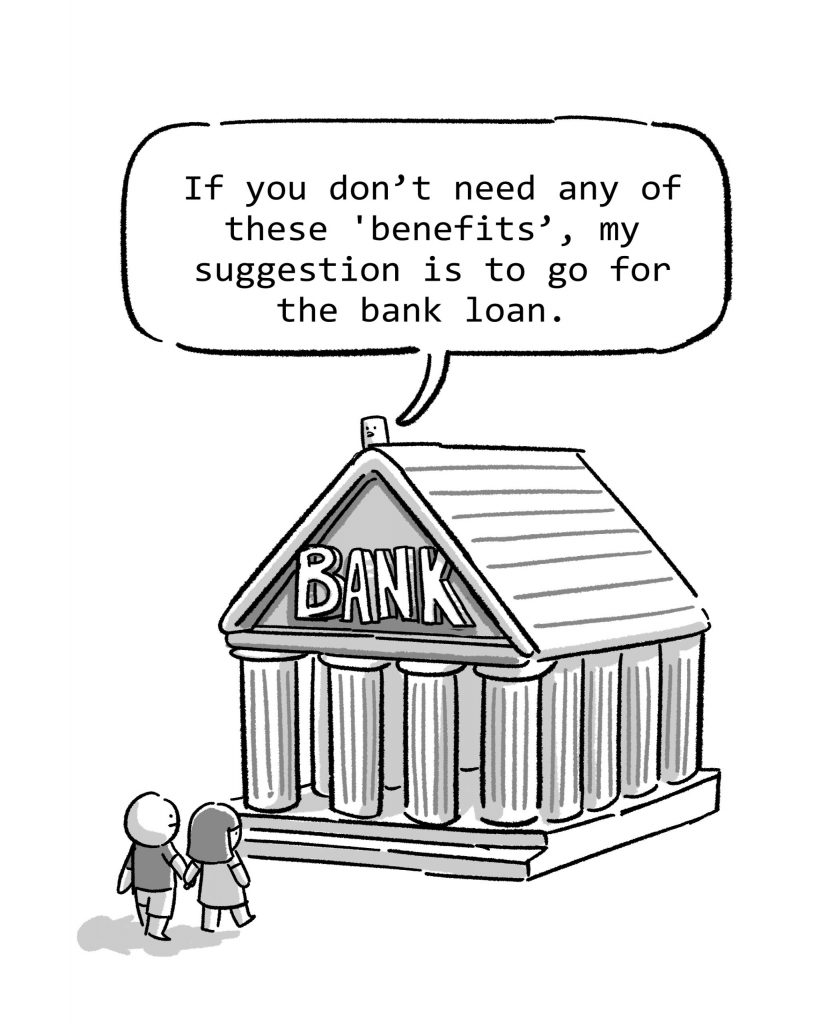

Pro tip: There are several factors to consider when deciding between an HDB housing loan or a loan from an FI. Check out this article to compare the differences between the two financing options.

Step 7: Collect keys to flat

When construction of your flat is completed, HDB will notify you to make a trip to its office to collect the keys to your flat. The key collection process is straightforward and you will be guided by experienced HDB officers. Have the necessary documents with you, collect your keys and congratulations on becoming a home owner!

Planning your flat purchase is now easier with the new HDB Flat Portal – a one-stop platform for flat buyers to gather housing-related information and plan their housing budget. We break down the portal’s many useful features in this step-by-step guide on how you can use the HDB Flat Portal for your BTO application!

Content

1.Work Out Flat Budget With the Budget Calculator

• Fill in household and financial information

• Estimate the housing loan amount from HDB or financial institutions (FIs)

• Adjust loan amount and repayment period based on affordability

• Understand the considerations when taking a housing loan from HDB or FIs

2. Find a Flat on HDB Flat Portal

• Search for flats based on estimated budget

• Browse through available flats

• Shortlist and compare flats

3.Check Flat’s Payment Plan With the Payment Plan Calculator

• Find out the estimated costs and fees for intended flat

• Receive housing loan estimates for intended flat purchase

• Check the payments required at different milestones

4. Apply for a Flat

• Submit flat application

• Receive notifications for shortlisted units

Work out your Flat Budget with the Budget Calculator

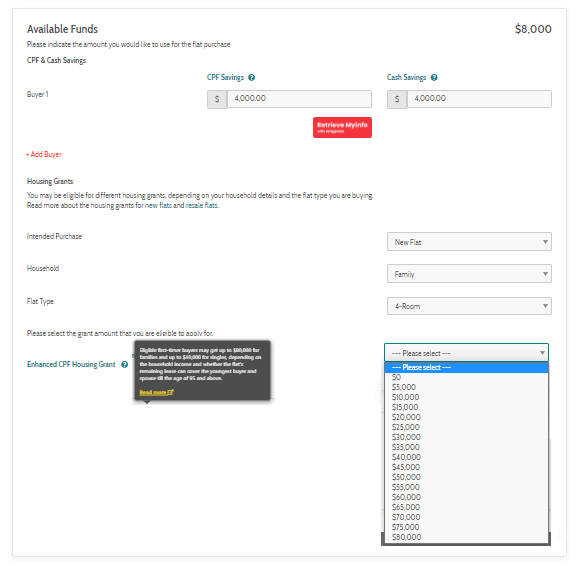

As with any big purchase, it’s good to start by working out your budget. This will help you shortlist suitable flats that you can afford, and here’s where the budget calculator on the HDB Flat Portal comes in handy! The budget calculator helps you calculate your housing budget by considering your CPF and/or cash savings, probable CPF housing grants, and amount of estimated housing loan from HDB or the FIs.

Step 1: Fill in your household and financial information

On the menu bar, select ‘Calculators’ followed by ‘Check My Budget’. Enter your available CPF and cash savings, household income, and flat that you intend to purchase. Based on the information, the type of housing grant and probable grant amounts will be shown. You can find out more about housing grants eligibility by clicking on the “Read more” link in the tooltip.

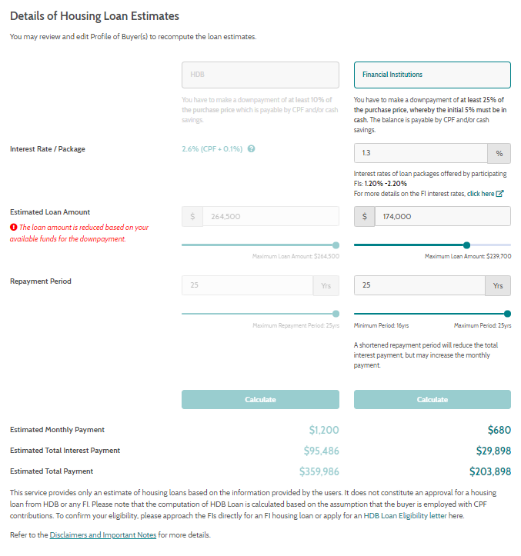

Step 2: Estimate housing loan amount from HDB or FIs

Next, if you are considering a housing loan, you can obtain from HDB and the FIs an estimate of the housing loan amount that you would be considered for. Start by selecting your financing option ie. housing loan estimates from HDB or the FIs.

Can’t decide between the two? You may compare the estimated loan amount, interest rate, monthly payment, total interest payment and conditions for each financing option. The calculator also provides a list of interest rates on housing loan packages from participating FIs. You may refer to this to indicate a preferred interest rate for the computation of the FI housing loan estimate.

Do note that the housing loan computation are estimates based on the information you have provided and does not constitute an actual approval for a housing loan from HDB or the FIs. You may wish to reach out to the FIs if you require clarification on your eligibility for a housing loan.

A side-by-side comparison on the estimated housing loan from HDB and FIs

Step 3: Adjust loan amount and repayment period based on affordability

You can adjust the loan amount, repayment period or the FI interest rate to understand the differences in estimated monthly repayment and total interest payment for each combination. The loan amount will be adjusted accordingly, should there be insufficient funds required for downpayment for the flat purchase. Your estimated housing budget will appear at the top of the page.

Step 4: Understand the considerations when taking a housing loan from HDB or FI

There are various factors to consider when taking a housing loan. Understanding the terms and conditions of each loan options can help you make an informed decision before purchasing a flat.

With an estimated flat budget in mind, it’s time to look for a flat! Click on ‘Search for Flats’ under ‘Related Services’ at the bottom of the budget calculator. This will lead you to the ‘Finding a Flat’ page where the available flats within your computed budget would be populated. You can also access the page via the menu bar of the HDB Flat Portal.

Find a Flat on the HDB Flat Portal

The HDB Flat Portal lists current and upcoming BTO and SBF flats during sales launches and flats for open booking. In this article, we will focus on BTO and SBF flats.

Pro tip: You can save your search profile and choose to be notified via email when a unit or project that matches your criteria becomes available.

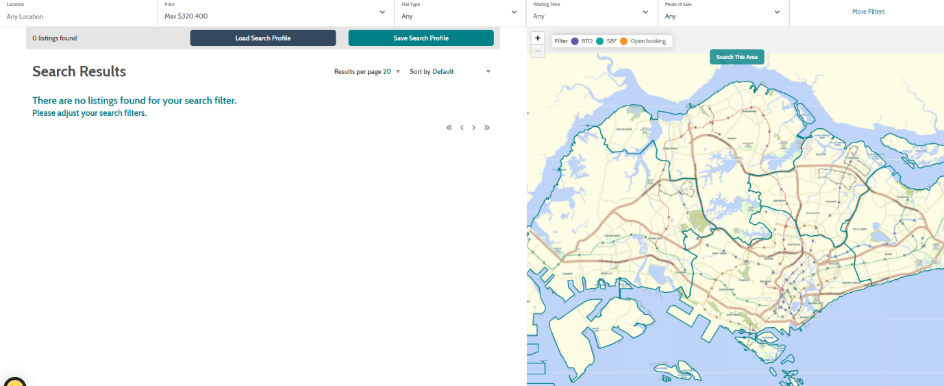

Step 1: Search for flats based on your estimated budget

Search for the flats by location, price range, flat type, waiting time and other criteria. You can also import your estimated housing budget from the budget calculator into the maximum price search filter.

Step 2: Browse available flats

During a sales launch, a banner will appear on the HDB Flat Portal’s homepage. Clicking on this will lead to a page with information of the projects on offer.

Step 3: Shortlist and compare flats

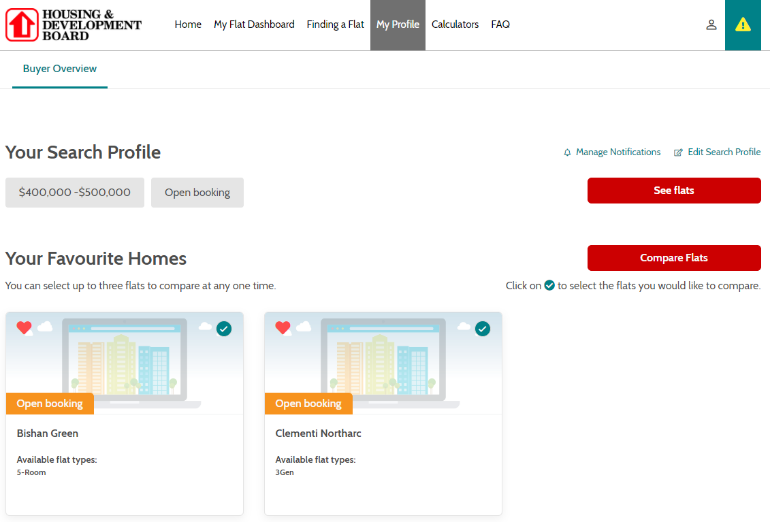

Shortlisted several flats that you like but can’t quite decide yet? Click on the heart-shape button to save them to your favourite list for a side-by-side comparison later. You can add up to 10 homes to your favourite list for comparison.

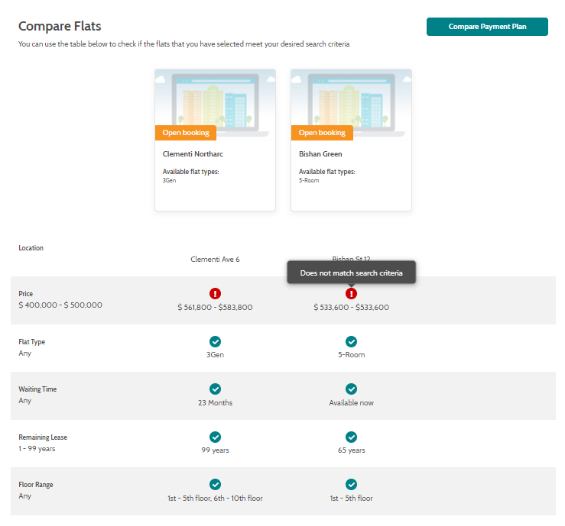

For flat comparisons, click on ‘My Profile’ on the menu bar. Under “Your Favourite Homes”, select up to three listings and click ‘Compare Flats’ to compare their location, price, flat type, waiting time, remaining lease and floor range. Attributes that do not meet your saved search profile will be indicated with a red exclamation mark.

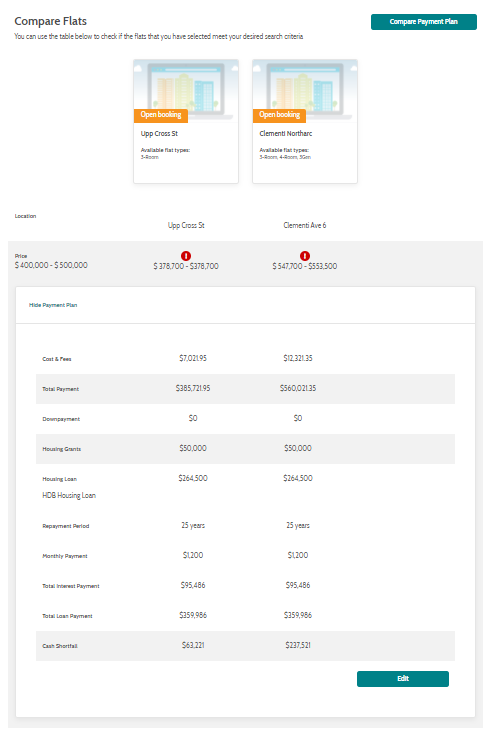

You can also compare the estimated cost and fees, loan amount, total interest payable, monthly repayment and more for the selected flats by clicking on the ‘Compare Payment Plan’ button. This will bring up the payment plan calculator. Simply fill in the missing information, scroll to the bottom and click on ‘Show Comparison’. Hop over to the next section for more information on the payment plan calculator.

Pro tip: Understanding the costs and fees involved at different payment milestones can help you make a more prudent flat purchase

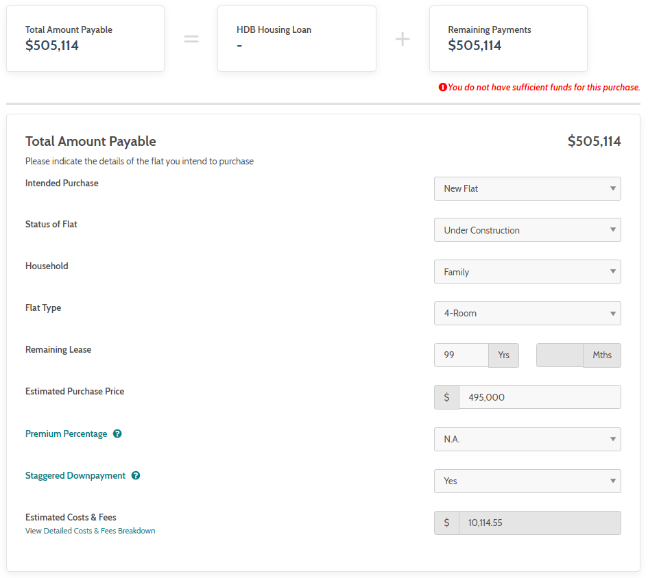

Check your Flat’s Payment Plan with the Payment Plan Calculator

If you have a preferred flat in mind, use the payment plan calculator to understand the payments involved for the different milestones, and find out if you have sufficient funds to finance the flat purchase.

The calculator checks the price of the flat against your available funds, probable CPF housing grants and estimated housing loan amount from HDB or the FIs, to determine if you have sufficient funds for the intended flat purchase. It also shows a breakdown of the cash and CPF payments required at various milestones of your flat buying journey to help you plan ahead .

Step 1: Find out the estimated costs and fees for the intended flat

Enter details of the flat that you intend to purchase. The estimated costs and fees related to the flat purchase will be calculated and added to the price of the flat, to form your total amount payable. You may also view a detailed breakdown of the costs and fees.

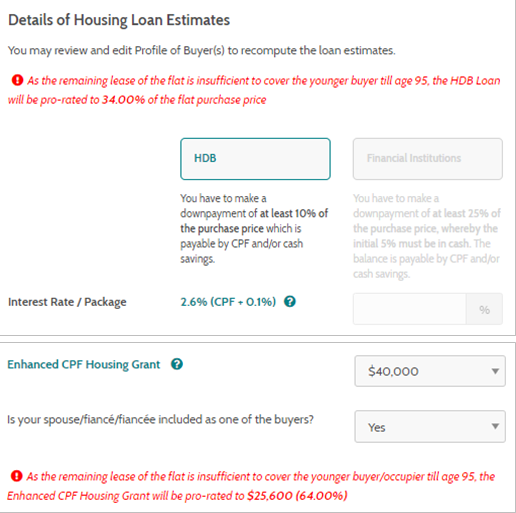

Step 2: Receive housing loan estimates

Remember the budget calculator? This section will be pre-filled based on the information you have provided in the budget calculator (note that the fields will only be pre-filled when the same browser tab is used for computing figures on both calculators).

If the remaining lease of the flat does not cover you or your spouse till the age of 95, the estimated HDB housing loan amount and Enhanced CPF Housing Grant amount will be automatically pro-rated.

In the above scenario, you will be advised to visit the CPF Housing Usage Calculator to work out the estimated amount of CPF savings you can use to purchase the flat.

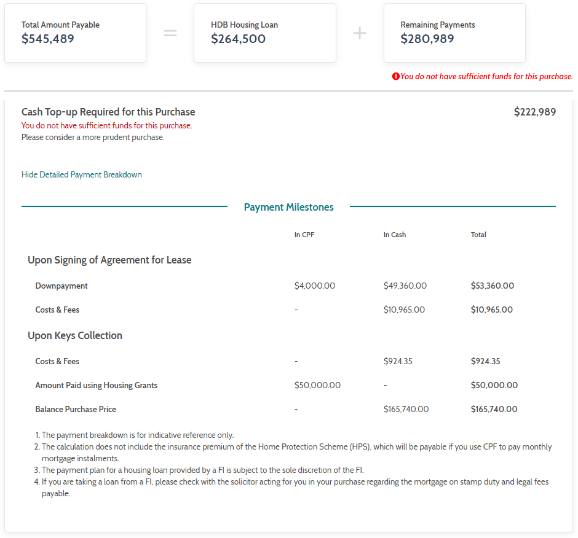

Step 3: Check the payments required at the various milestones

After deducting your estimated housing loan and available funds (CPF and cash savings) from the total amount payable, you will be shown a detailed breakdown on the amount of CPF and cash payment at different milestones.

The calculator will also alert you if you have insufficient funds for the flat purchase and show the amount of cash top-up required.

Apply for a Flat

During a sales launch, information on the BTO and SBF projects on offer will be available on their respective pages. These pages will also include a link to an online flat application form.

Step 1: Submit flat application

Click on the application link and submit your flat application before the closing date. For BTO and SBF sales launches, do note that applications are not processed on a first-come-first-served basis. HDB will check on your eligibility to buy a flat and determine your queue position to book a flat through a computer ballot.

Step 2: Receive notification for units on your Watchlist

If you are invited to book a flat, you can place your preferred flat on a watchlist to monitor their availability. You may choose to receive email notifications when any of the units on your watchlist are booked. The link to the watchlist module can be accessed through the project details page under ‘My Profile’.

Ready to apply for your flat? Hop over to the HDB Flat Portal now!

Maybe your flat is now a little roomy after the children have grown up and moved out, or you’re looking for a place that’s closer to them so you can help take care of the grandchildren. Or perhaps you‘re looking for a change in environment, a new home where you can enjoy your golden years. Whatever the reason, there are housing options, schemes, and grants that seniors can tap on when buying a flat. Here’s a senior’s guide to flat buying:

Housing Options for Seniors

For those looking for a cozy space that’s easy to maintain, you could consider a 2-room Flexi flat. If you and your spouse are aged 55 and above, you can also opt for a shorter lease. You can choose a lease of between 15 and 45 years in 5-year increments, as long as it covers you and your spouse up to the age of at least 95 years. The price of the flat will also be adjusted based on the lease chosen.

These senior-friendly short-lease flats come installed with grab bars. You can also opt for additional senior-friendly fittings in the flat under the Optional Components Scheme (OCS). These include built-in kitchen cabinets with induction hobs and cooker hood, kitchen sink, and a built-in wardrobe.

Schemes and Grants

Seniors can also tap on schemes and grants either to help improve their chances of being balloted for a new flat during sales exercises or to help finance the flat purchase.

If you are selling your current flat and buying a 3-room or smaller flat, you may be eligible for the Silver Housing Bonus. If eligible, you could receive a cash bonus of up to $30,000 when you top-up your CPF Retirement Account (RA) with your sales proceeds and join CPF LIFE, CPF’s life annuity scheme that provides monthly payouts for as long as you live.

If you’re buying a new flat, you may also qualify for one of our Priority Schemes, which improve your chances when balloting for a flat. If you are buying a new flat near your married children, you may qualify for the Married Child Priority Scheme. If you’re looking specifically to buy a 2-room Flexi flat that is either near your current flat to age-in-place in a familiar environment or near your married child, you may qualify for theSeniors Priority Scheme.

If you’re buying a resale flat near your children, you may qualify for theProximity Housing Grantof $20,000.

From housing options designed with your needs in mind, to schemes and grants to help in your flat buying journey, there is plenty of support for seniors when buying a flat.

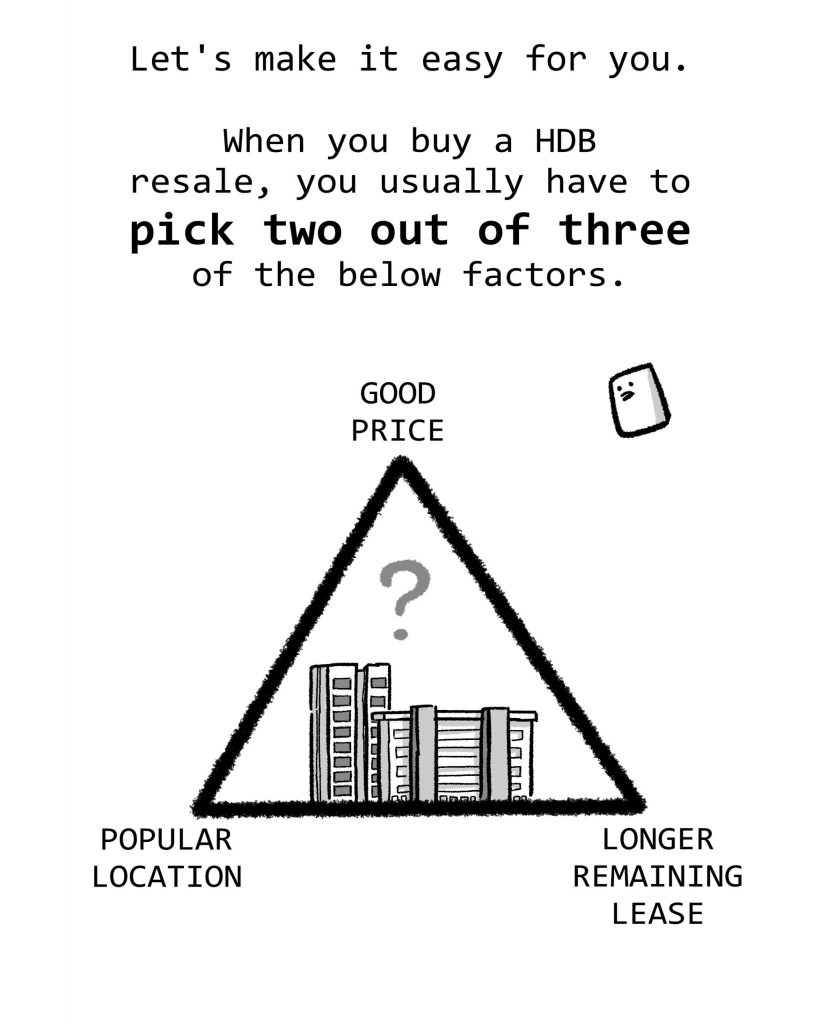

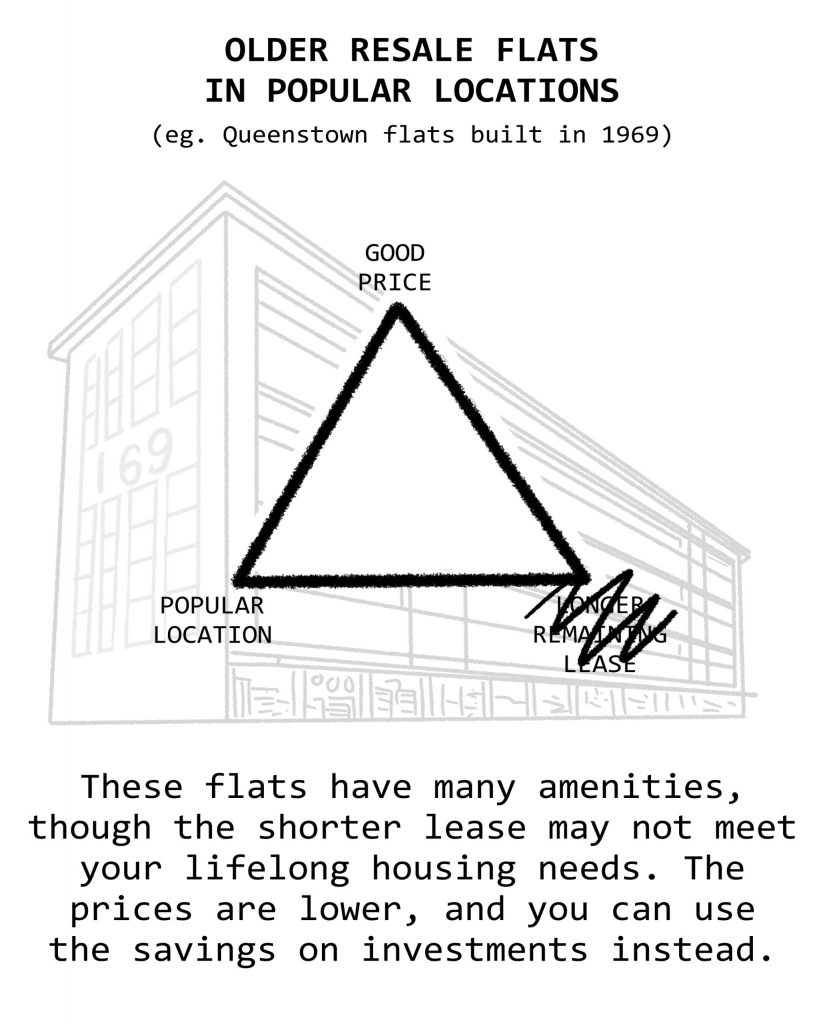

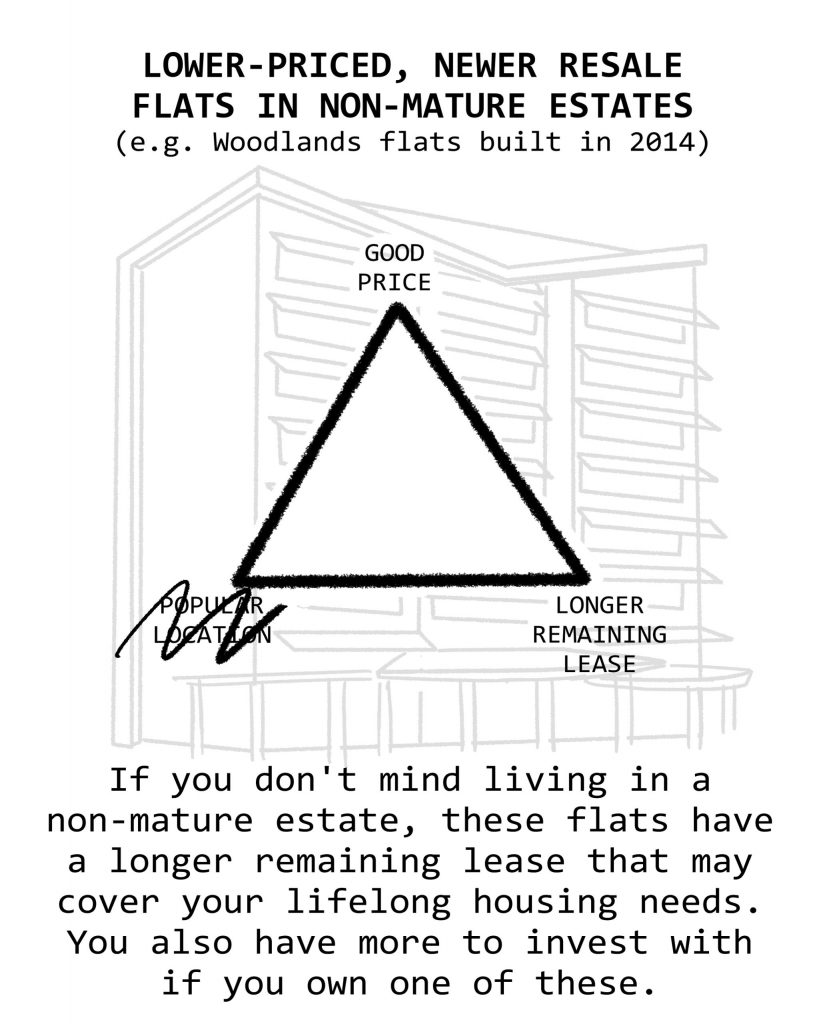

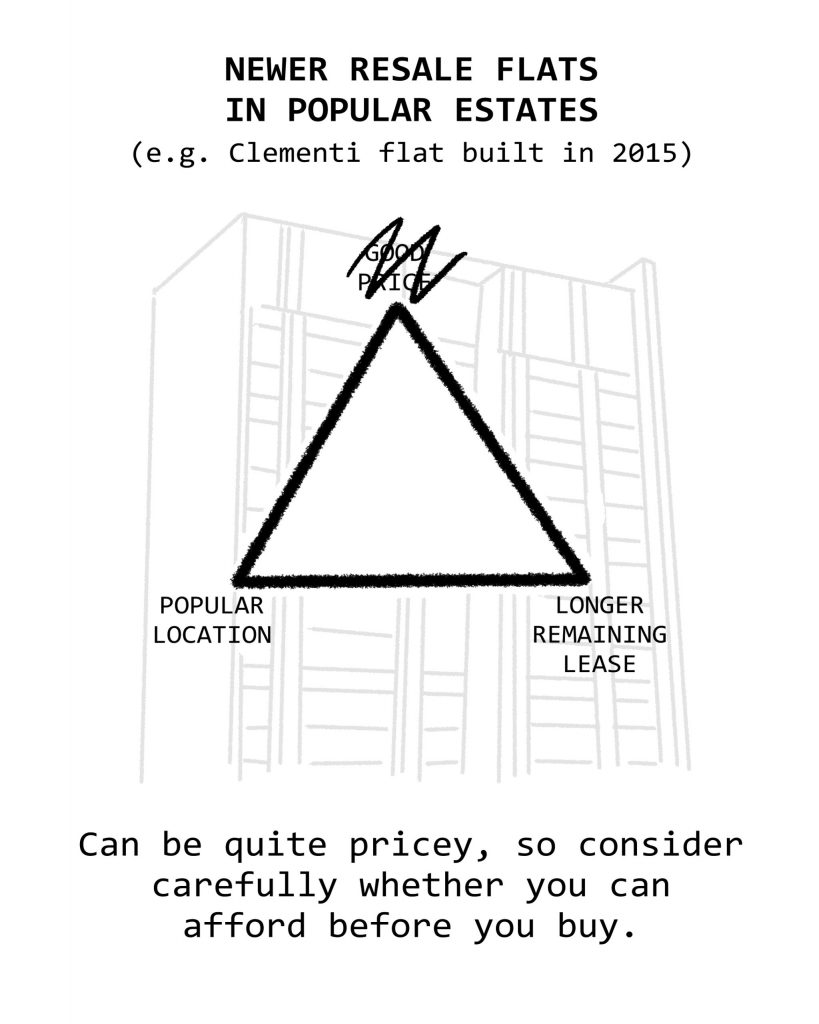

Thinking of buying a resale flat, but not sure what to look out for? Here are the 3Ls to consider when looking at potential resale flats – location, lease and layout.

1. Location

One of the advantages of purchasing a resale flat is the variety of HDB flats available on the open market. How then do you choose the location that suits you best?

For a start, it might be useful to think about what is important to you and your lifestyle. If you love being close to nature, you might want to look for a flat located near a park, for instance. If you have school-going kids, you may need to check out nearby schools. If living near your parents or in-laws is important, consider looking at resale flats near them. For this, you may also want to check if your potential home would qualify you for a Proximity Housing Grant.

Transport options are also important to consider. While living near an interchange, main road or major transport node would bring convenience, fringe neighbourhoods provide respite from the hustle and bustle.

2. Lease Length

Unlike BTO flats, resale flats sold on the open market come with varied leases. This is important to consider since the length of lease remaining on the flat would impact the amount of CPF money you can tap on to finance your flat purchase. It can also impact the Enhanced Housing Grant amount you can enjoy (if eligible). Both the CPF usage limit and the grant amount will be pro-rated based on the extent the remaining lease of the flat can cover the youngest buyer up to the age of 95.

Don’t worry if that sounds like too much math for you – the budget calculator on the HDB Flat Portal is a great resource to consider when purchasing a resale flat.

3. Layout

Finally, resale flats come in a variety of layouts, so it can be daunting to evaluate all the options. Again, ask yourself – what fits your lifestyle? If you’re a family with kids, you may prefer a bigger flat, but if you’re a senior looking for a comfortable place to retire, consider cosy spaces that are easier to maintain.

#BTOgether at 60: Couple Buys an HDB BTO Flat under MGPS

Mr and Mrs Loi were one of the first few families who moved to Punggol in 2003. After 18 years, having witnessed Punggol develop from a sleepy town into a bustling one, they moved to Bidadari to be close to family. The couple, both in their 60s, decided to purchase an HDB BTO Flat the same time as their son, Francisco, and daughter-in-law, Adora under the Multi-Generation Priority Scheme (MGPS).

Hello Mr and Mrs Loi, congratulations on your new home. How do you find it here?

Bidadari is very green and tranquil despite being close to many amenities, such as the shopping malls at Potong Pasir (Poiz) and Serangoon (NEX). There are also several eating places around the estate, so we will not run out of food choices! Like Punggol where we used to live, there are many covered linkways and ramps that make it easy for us to explore the estate—such as playgrounds— with our grandchildren.

How did you hear about MGPS?

We did not know about this scheme until our son asked us to apply for an HDB BTO flat together – as parents with their married child. He was considering Bidadari for its location and proximity to 2 MRT stations (Potong Pasir and Woodleigh), which makes getting around more convenient. We read up about the BTO project and were convinced when we saw that there will be a lot of greenery and a lake, as we wanted to live somewhere close to nature like Punggol!

Eventually, we applied for a 3-room flat and our son, a 4-room flat. It was a unique family bonding experience as we got to celebrate the different flat buying milestones together, such as being nervous about getting a ballot number, as well as the excitement during flat selection and key collection!

Can you describe your moving in process?

As our son helped us oversee the renovation, our ‘job’ was mainly to decide and buy the home appliances early so that he can make sure that that everything fits into the space and design. We also chose materials that are easy to clean and maintain. For example, we use KompacPlus for our kitchen as we are heavy cookers and the material prevents water marks and stains.

What do you love most about your new home?

We appreciate the layout of our current HDB BTO flat more, even though our current 3-room flat is smaller than our previous 4-room flat. There is more airflow, and we find it good for hosting guests as the living room feels bigger. When it is just the two of us, we enjoy how bright, cosy, and close to nature the home feels.

The dining area, where the family gathers

However, the best part for us is being able to spend more quality time with our son’s family even though we have our own private spaces. We also get to take turns to cook sumptuous dinners for everyone!

The Lois’ bright and airy living room

For more housing options for seniors, read here. Planning to purchase an HDB BTO flat? Find out everything you need to know in this step-by-step guide.