When a loved one departs, things change in more ways than we can imagine. So how can death in the family affect your flat?

1. If a co-owner passes away and you are the other co-owner

Most flats in Singapore are joint-owned – by husband and wife, or parent and child. If a joint-owner passes away, his or her share of the flat will be transferred to the remaining owner.

As the remaining family or single occupier, you can retain the flat ownership if:

You are a Singapore Citizen or Singapore PR

You are at least 21 years old

You fulfil HDB’s eligibility conditions to own the flat

2. If the sole owner passes away

If the flat’s sole owner passes away, their interest in the flat will be distributed according to their will; or if there is no will, according to the provisions of the Intestate Succession Act. A court order is required for legal authority to administer the deceased’s estate. The remaining family or occupiers should engage a private solicitor to apply for the appropriate court orders, which gives legal authority to the person named in the will (or if there is no will, someone as the Administrator) to manage the deceased’s estate.

Grant of Probate is needed if there is a will. This gives the person named in the will (the Executor) legal authority to manage the deceased estate.

Grant of Letters of Administration is needed if there is no will. This gives the Administrator legal authority to manage the deceased’s interest in the flat, which will be distributed according to the Intestate Succession Act.

As the remaining family or single occupier, you can retain the flat ownership if:

You are a Singapore Citizen or Singapore PR

You are at least 21 years old

You fulfil HDB’s eligibility conditions to own the flat

Once the Grant has been obtained, you can engage your own solicitor or appoint HDB’s solicitor to act for you to register your legal right as the Executor or Administrator.

As the Executor or Administrator of the estate, you will have to complete relevant paperwork and apply at the HDB Branch in charge of the flat to transfer flat ownership to the beneficiaries. This is subject to HDB’s eligibility conditions governing transfer of flat ownership.

For more information about buying, financing or selling your HDB flat, follow LeposhDesign on Facebook.

Sometimes life events may require us to change the ownership status of our flat. For example, when you are getting married and buying a flat with your spouse, or following a divorce or passing of a loved one in the family. It is possible to apply for a change in flat ownership without monetary consideration, as long as all the current and new flat owners are aware of and consent to this change.

As a flat owner, you may apply for a change in your flat ownership to immediate family members if they meet all eligibility conditions. Here are the 4 most common types of change in flat ownership.

Inclusion of owners (e.g including your daughter as an owner)

Withdrawal of owners (e.g your daughter withdraws as an owner)

Substitution of owners (e.g substituting your daughter’s ownership with your son)

Total change of owners (e.g changing the ownership to your child)

If there is more than 1 owner for the flat, you will need to decide on the manner of holding – either by joint-tenancy, or tenancy-in-common. The former means that all owners own the whole interest in the property, and do not have separate shares. Meanwhile the latter denotes that tenants-in-common own the same property, but each with their own separate shares. HDB allows a maximum of 4 owners for each flat.

Use the following resources to find out how to go about effecting a change in flat ownership within your family:

Selling a flat? Here’s what you need to know about the HDB Resale Portal.

The HDB Resale Portal was created to streamline the process of buying and selling resale flats. With eligibility checks and other processes integrated into the same portal, home owners can even sell their flat on their own, without a salesperson.

1. Get Your Home Ready

Selling your home may be unfamiliar to you, but we’re here to help! Check out our tips to make your flat selling journey as smooth as possible.

2. Register Intent to Sell at the HDB Resale Portal

Once you have confirmed with your flat buyer on the sale, and have mutually agreed on the selling price, you need to get the formal process started by registering your intent to sell on the HDB Resale Portal.

With the handy SingPass Mobile App, signing in is a breeze. By scanning a QR Code during the login process, your personal information from the Government’s MyInfo service will be automatically and securely populated into the HDB Resale Portal.

When you register the intent to sell, the HDB Resale Portal will also obtain information about your flat to help facilitate the sale – these include whether you have fulfilled the Minimum Occupation Period, and the Ethnic Integration Policy (EIP) quota prescribed to your precinct and neighbourhood.

The next step is to wait for 7 days – the cooling-off period – before you can proceed further. Take this time to exchange information with your buyer for the Option to Purchase (OTP). You can download the OTP form from the HDB Resale Portal (or HDB InfoWEB beforehand) to understand the terms and get started on the sections that you will need to fill in.

The OTP is a contractual document used for HDB resale transactions. Under the Housing and Development Act, sellers (and buyers) must use the Option to Purchase for any sale or purchase of flats. No gentlemen’s agreement or special handshake allowed!

3. Grant The OTP

After 7 days, you can sign on the completed OTP form and grant it to your buyer. You and your buyer will also need to agree on the Option Fee (a sum between $1 to $1,000) which will be paid to you and acts as a “deposit” for the OTP.

The Option you’ve granted to the buyer is valid for 21 calendar days and expires at 4pm on the 21st day. During this period, you will not be able to grant the Option to another buyer. Even if your buyer decides not to exercise the Option, you will need to wait for the Option to expire. In such situations, the buyer will forfeit the Option Fee.

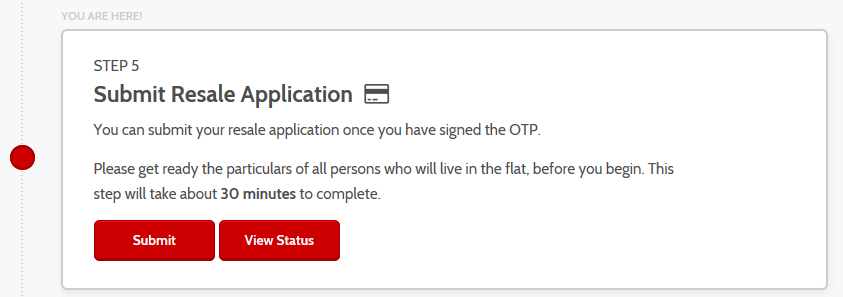

4. Submit Resale Application and Documents

Once your buyer has signed the OTP, you will need to log into the HDB Resale Portal and submit the resale application along with supporting documents. HDB will verify the information and notify you and your buyer of the application outcome within 8 weeks.

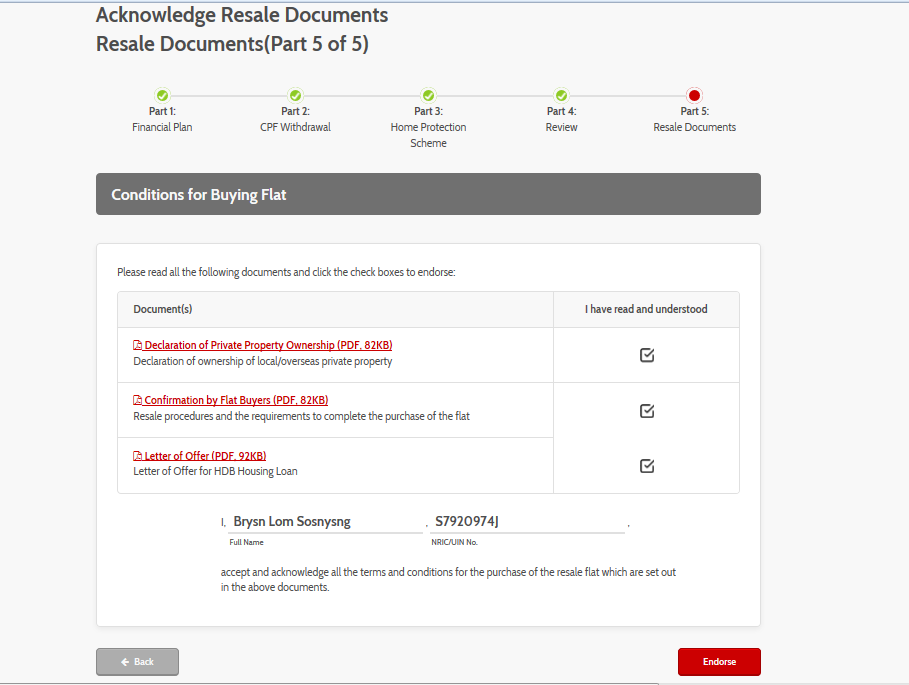

5. Endorse Resale Documents

After submitting the documents, both you and your buyer will be notified via SMS to endorse the documents on the HDB Resale Portal within 6 days.

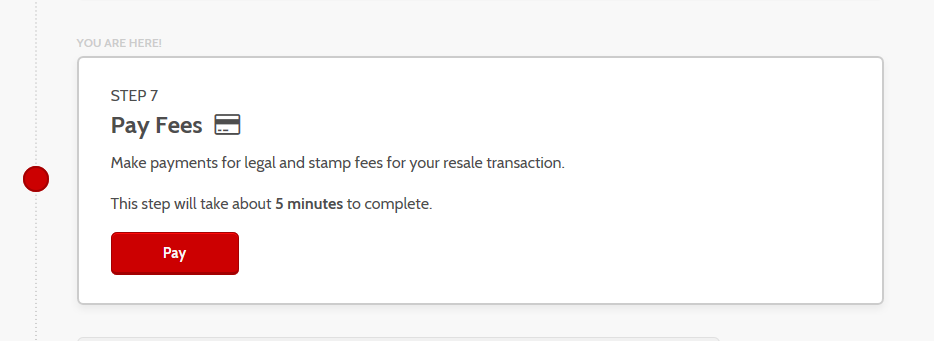

6. Pay Resale Fees and Wait for HDB’s Approval

Once the documents are endorsed by both parties, you can move onto paying the legal and stamp fees for the flat resale transaction. Credit or debit card payments are accepted.

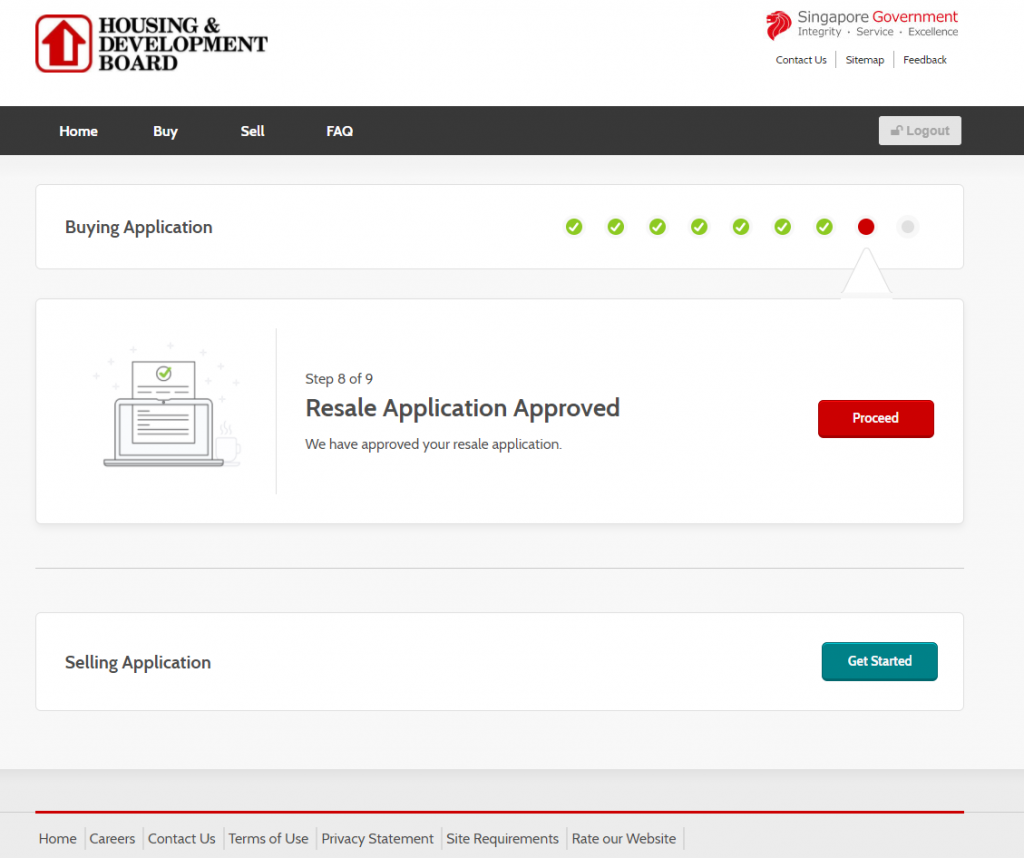

Once the fees are paid, all you need to do is wait for HDB to review and approve the resale application. You will receive an SMS notification when that happens!

7. Attend Resale Completion Appointment

You’ll also be notified on your Resale Completion Appointment at the HDB Hub in Toa Payoh, where both you and your buyer will need to attend to finalise the transaction.

It’s never too early to think about retirement adequacy — in other words, how you can supplement your income during your retirement years. Beyond CPF monies, personal savings, and possibly investments, home owners can also choose to unlock the value of their HDB flats in their golden years. Depending on your needs and preferences, here are some ways you can monetise your HDB flat:

1. Continue living in your flat

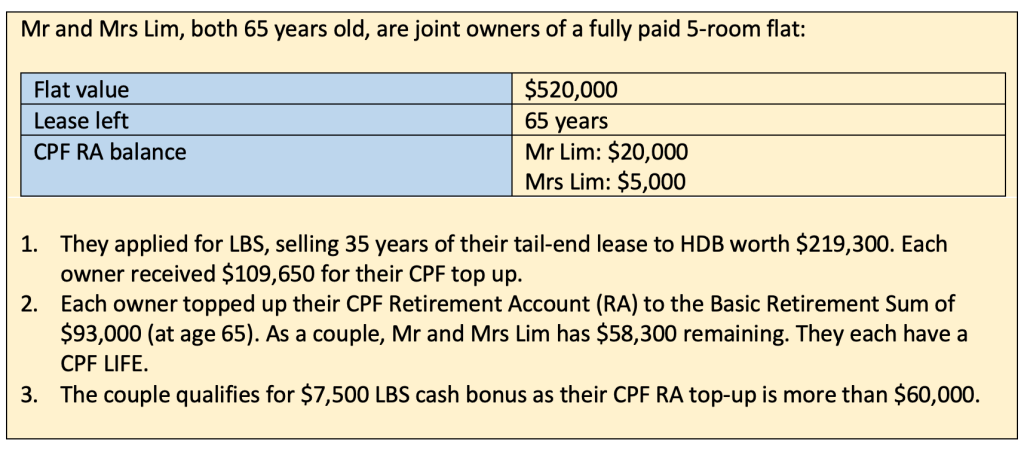

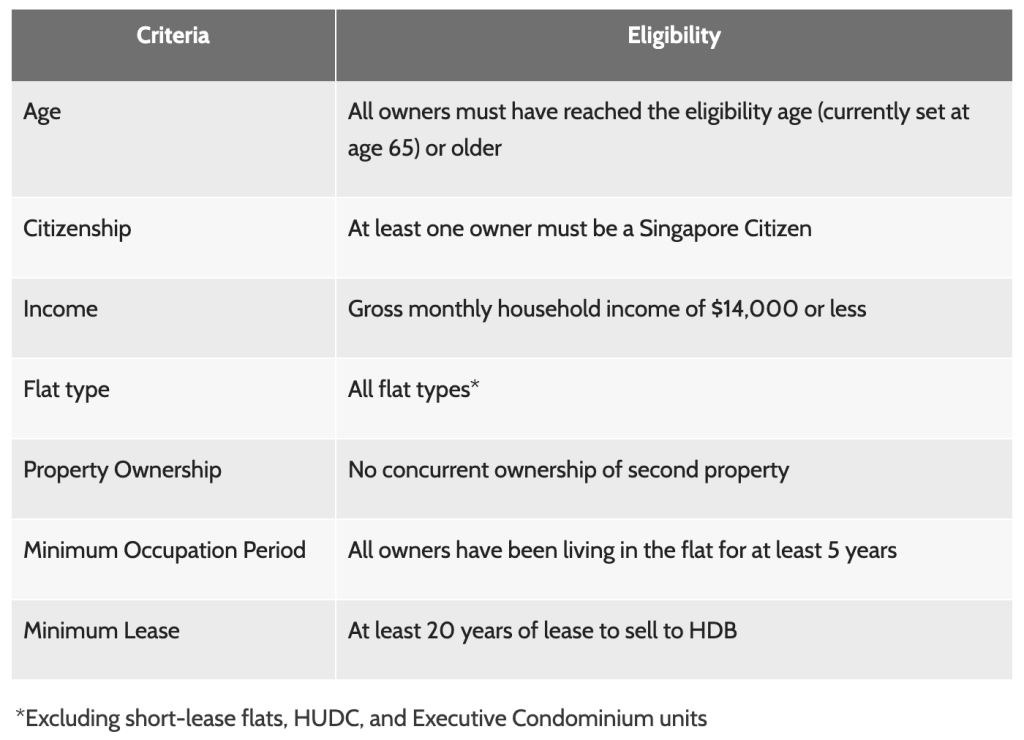

Mr and Mrs Lim, both 65 years old, chose to apply for the Lease Buyback Scheme (LBS) as they wanted to continue living in their existing flat. They received cash proceeds of $58,300, a monthly CPF LIFE payout of $1,090, and a cash bonus of $7,500.

You can consider monetising your flat under LBS if you have fulfilled the minimum occupancy period (MOP). Interested? Check out the eligibility criteria for LBS below, or on HDB InfoWEB:

If you are younger than 65 years old, there is the option of renting out your spare bedroom(s) for income. Remember to submit an application to rent out your bedroom(s) through My HDBPage or Mobile@HDB before the commencement of the tenancy, and refer to CEA’s tenancy agreement template for HDB flats.

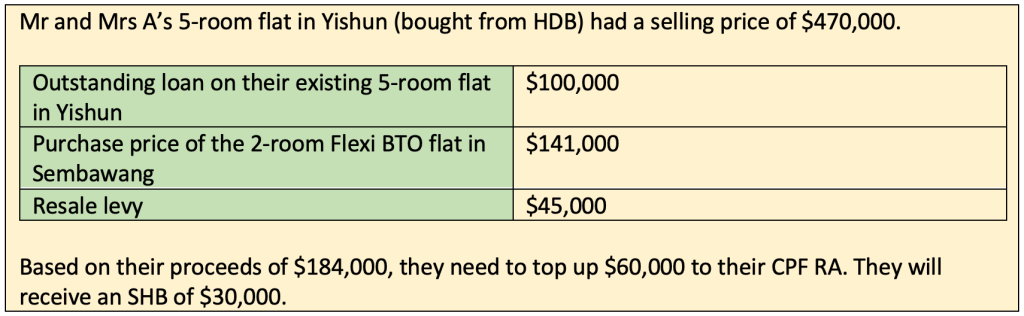

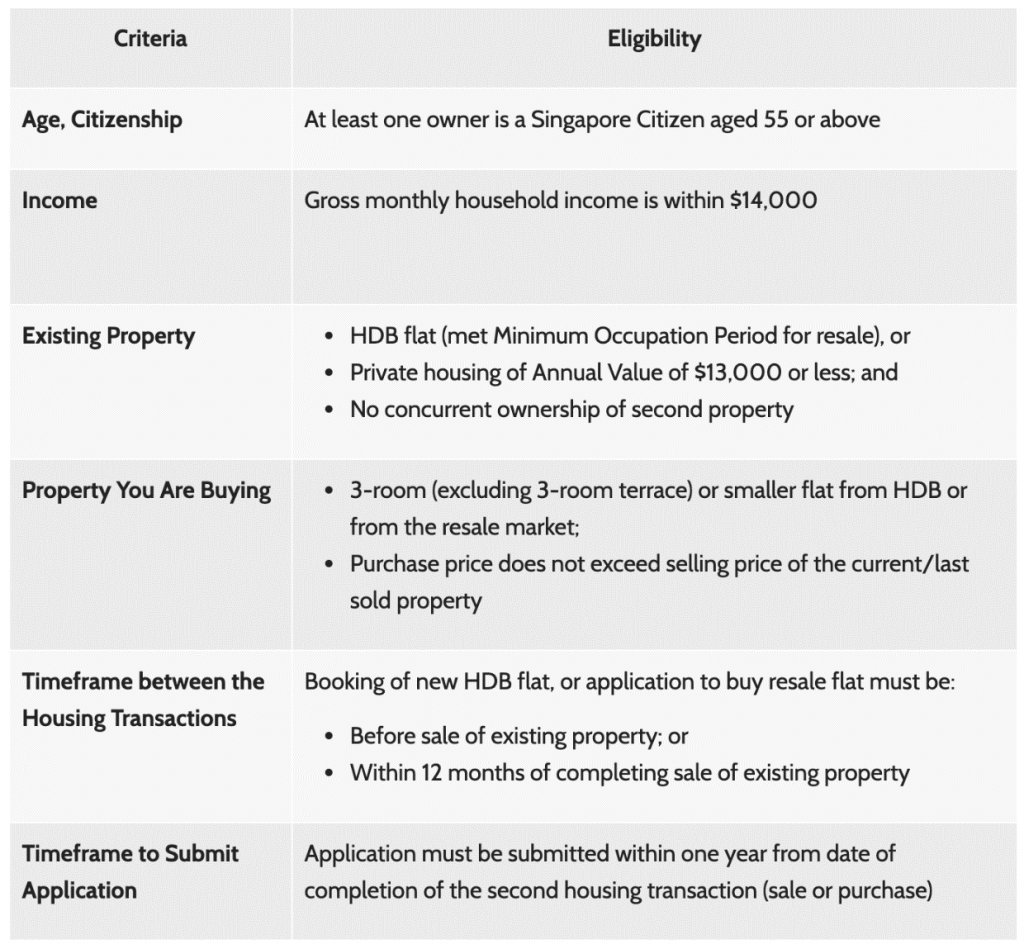

2. Moving out and purchasing a 3-room or smaller HDB flat

Mr and Mrs A sold their 5-room flat (bought from HDB) and bought a 2-room Flexi BTO flat. They qualified for a Silver Housing Bonus(SHB) of $30,000 on top of their proceeds.

The SHB is applicable when home owners top-up their CPF RA with the proceeds of the sale. You can view the eligibility criteria below, or on HDB InfoWEB:

For the latest information on monetising your flat for retirement, visit HDB InfoWEB.

Bonus tip: If you do not need an additional source of retirement income but want to learn more about other elder-friendly housing policies, here are 5 things to know about the Community Care Apartments.

So, you have listed your HDB flat on the market and are anxiously waiting for prospective buyers to pop by for a viewing. You may be ready to seal the deal, but is your house ready?

You don’t need huge home staging budgets like the real estate agents on Netflix’s Selling Sunset – all you need are some tips and tricks to spruce up your HDB flat before you arrange for flat viewings.

They say a picture paints a thousand words – this is especially relevant when selling your HDB flat, as you need to stand out from the crowd of existing flat listings. Take good photos showcasing the flat’s layout and space to highlight its potential.

P.S. Remember to take the photos during the day – natural light is key.

2. Declutter the Space

Clearing clutter is not an easy task but no one likes a messy space, especially prospective buyers of a new flat. Clutter makes it difficult for buyers to see the potential of the flat – after all, they are here to view the space.

3. Keep It Clean

Once you’ve gotten rid of clutter, do give the flat a thorough mop and scrub, especially on frequently used appliances and furniture. The flat need not be 100% spotless, but should at least be tidy – you do not want prospective buyers to be put off by the stains and dirt.

If your flat’s got attractive attributes, flaunt them! Whether it’s an unblocked view of the neighbourhood, ample living room space, or a unique kitchen concept, you should leverage these attributes which may appeal to prospective buyers. Open the windows to show the amazing view, rearrange the furniture to highlight the spaciousness of the living room, or if you’ve got a HDB flat with a great view, opt for viewings to happen in the day so that prospective buyers can enjoy the scenery.

Make your guests feel welcomed to your home. Add some fresh flowers or potted plant on the dining table, or even use scents to create a warm and cosy ambience in your room or home – these small touches could leave a strong and positive impression on your prospective buyers.

Now your flat is ready to meet its prospective owner! Did you know that you can sell your flat on the HDB Resale Portal? Check out our guide to find out more!

Good photos are key when selling your HDB flat. Not only do they showcase the flat’s potential, good photos will help set your home apart from existing flat listings. MyNiceHome caught up with experienced interior photographer Jino Lee, who gave us some tips on capturing the best side of your home!

1. Capture the Best Bits

Decluttering lets you capture the space and showcase its potential. An organised space also makes for appealing photographs, and helps prospective home buyers to visualise themselves living in the flat. To portray a cosy and lived-in look, include strategically placed coffee table books, coloured cushions or decorative plants in your photos.

2. Adopt Wide Angles

Wondering why the photographs aren’t doing enough justice to your flat? You might be using the wrong lens! Using wide angle lenses when capturing your shots can showcase the space to its fullest extent, and even make your house look more spacious.

3. Position Your Photos

Avoid out of perspective photos (left) by repositioning the angle such that it’s at eye level (right)

For a more accurate perspective of the space, capture your photos at eye level. At the same time, ensure that your photos angles are straight – if you require a little help, simply enable the grid option on your phone or camera.

4. Let the Light In

Never underestimate the power of good lighting. While natural light helps to soften the look of your photos, indoor lighting can also be used. Most importantly, ensure that the space is sufficiently lit to best showcase the space.

It might take some work, but the effort taken to showcase your flat will definitely be worth it.

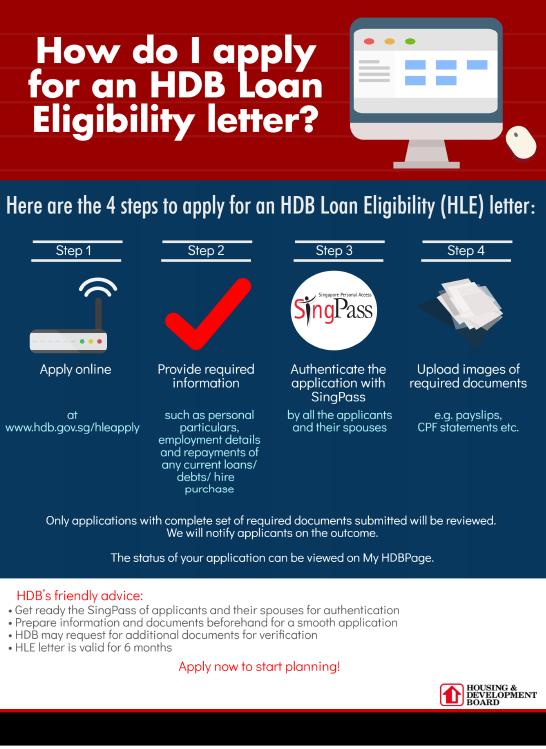

Once you have a great partner by your side and a shiny ring on the finger, it is only natural that both of you would be looking to buy your very own home sweet home. If you wish to take a housing loan from HDB, be sure to apply for your HDB Loan Eligibility (HLE) letter before you seek out your new pad.

Why do I need an HLE Letter?

An HLE letter will tell you the amount of HDB housing loan you are eligible for, the repayment preiod, and other important financial details. This loan amount, coupled with CPF housing grants, as well as your CPF and cash savings, make up the budget for your flat.

Armed with this information, you can avoid falling in love with a flat that is beyond your means.

You will need a valid HLE letter when you book a new flat with HDB, or even when you exercise an Option to Purchase to buy a resale flat.

Okay… so how do I apply for an HLE Letter?

There are only 4 steps to apply for an HLE letter. You can do so online via HDB InfoWEB. Do prepare the required information and documents beforehand for a smoother application.

Not everyone is eligible for an HDB housing loan though, so it is best to check on your loan eligibility as early as possible. Having an HLE letter in hand will also help you plan your flat budget. There is no harm in planning ahead; after all, the HLE letter is valid for 6 months and there is no payment involved to apply for one.

What if I did not get a large enough loan?

Regular income, age, and financial standing are 3 main factors that HDB considers in loan assessment. If you are just starting out in your career, and the eligible HDB loan amount is insufficient to cover the price of the flat you have your eye on, look around some more. There will be a flat for every budget and need.

Spend within your means and do not overstretch yourself financially — a cheaper flat might mean more money for rainy days, renovations, furnishings, or even a vacation.

We also have other financial tools; to help with your planning. All the best in working out a housing budget, so you can make an informed decision when buying a flat!

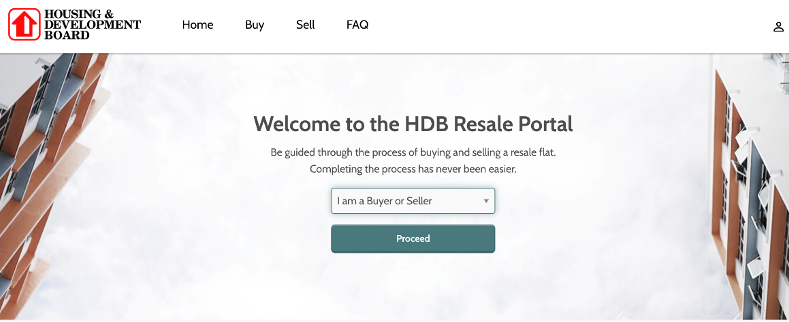

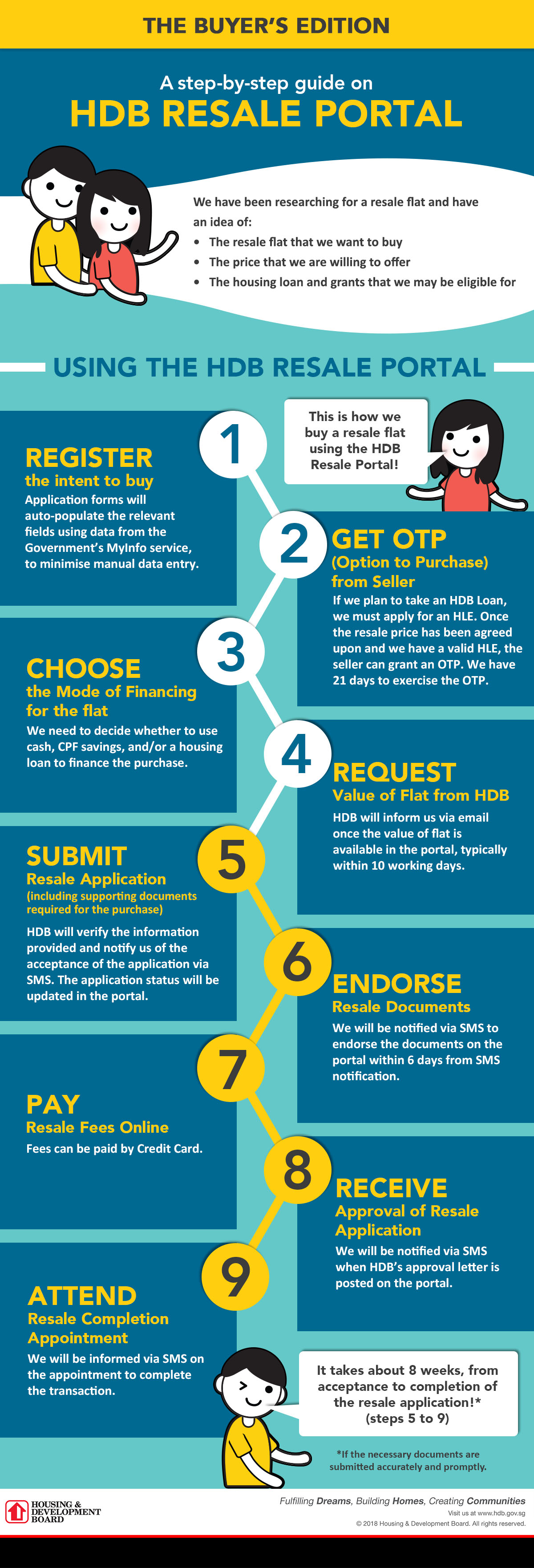

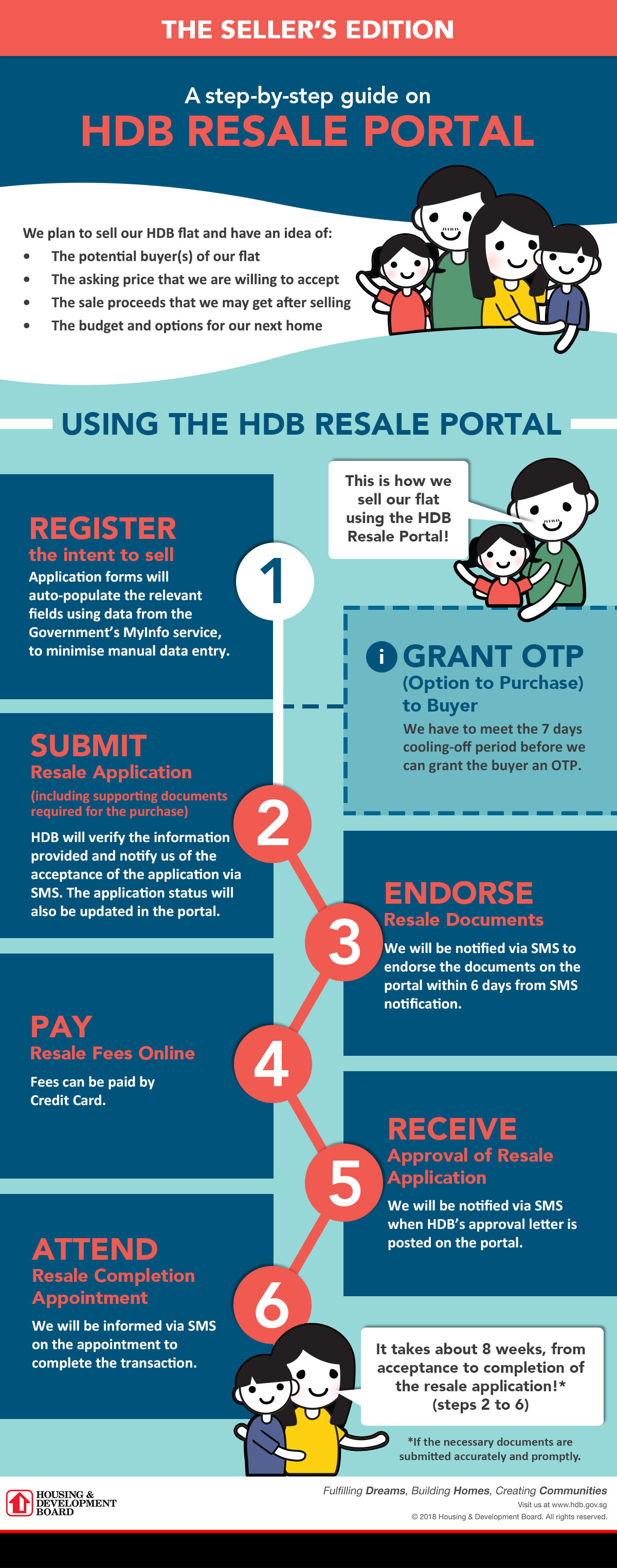

HDB resale flat buyers and sellers can now use the new HDB Resale Portal, launched on 1 January 2018.

The HDB Resale Portal streamlines all the resale of flats processes into a single platform, and provides a step-by-step guide for flat buyers and sellers throughout the resale transaction.

Using the HDB Resale Portal will benefit you in many ways:

– Shortens resale transaction time by up to 8 weeks

– Reduces manual entry of personal information

– Integrates all resale-related services

– Reduces number of appointments with HDB (Only 1 appointment required!)

With this portal, you can get instant results on your eligibility to buy a flat, housing grants, and HDB concessionary housing loan. Other important information, such as the Ethnic Integration Policy quota, upgrading status, upgrading costs billing status, and recent resale flat transactions nearby, have also been included in the HDB Resale Portal.

Here are the key steps to guide you in using the resale portal.

1. Register intent to buy/ sell

You must first register your intent to buy or sell a flat on the HDB Resale Portal. Your personal particulars will be automatically retrieved and populated from the Government’s MyInfo service.

2. Search for a flat and get an Option to Purchase (OTP)

Once you have found a resale flat within your budget, you will need to obtain an OTP from the seller. You have 21 days to exercise the OTP.

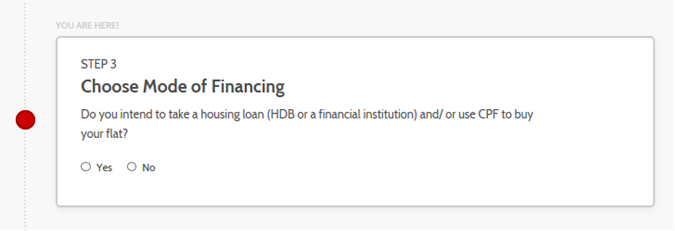

3. Choose the mode of financing

As a flat buyer, you will need to decide how you intend to finance the flat purchase. You can either use cash, CPF savings, or obtain a housing loan. If you wish to obtain an HDB housing loan, the HDB Resale Portal will guide you to apply for an HDB Eligibility Letter.

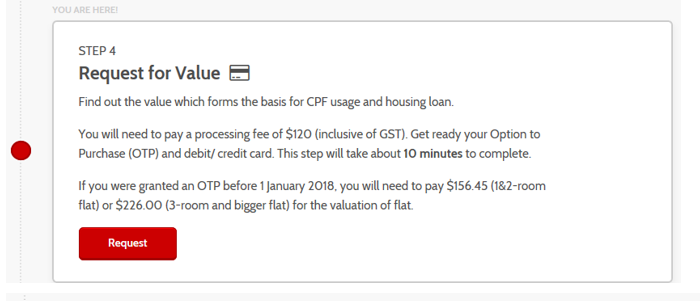

4. Request value of flat from HDB

If you are financing the flat purchase with your CPF savings and/or housing loan, you are required to submit a request to HDB to confirm the loan quantum and the amount of CPF savings you can use. You will pay HDB a processing fee of $120 (including GST).

Flat buyers can only submit a Request for Valuation after the seller has granted them an OTP. They will need to submit the Page 1 of the OTP and Request for Valuation, to HDB by the next working day after the OTP date.

If HDB requires valuation of the flat to be done, HDB’s appointed valuer will carry out the flat inspection within 3 working days after informing the seller. Flat buyers can check the flat’s valuation in the HDB Resale Portal within 10 working days from the inspection date.

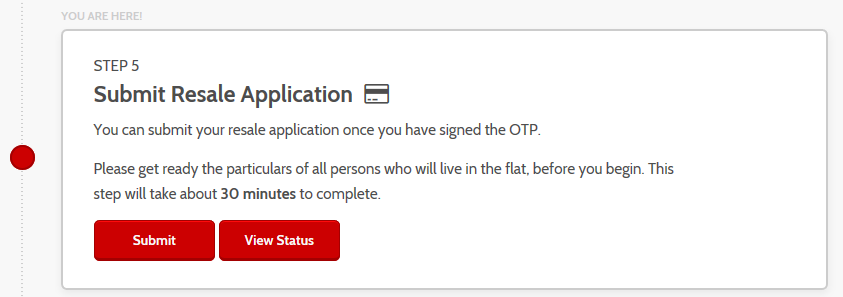

5. Submit resale application

Both flat buyers and sellers must submit their respective portions of the resale application with the supporting documents to the HDB Resale Portal, after the OTP has been exercised. They will need to pay an administrative fee, depending on the flat type.

HDB will verify the information and notify the buyers and sellers of the application outcome, typically within 8 weeks.

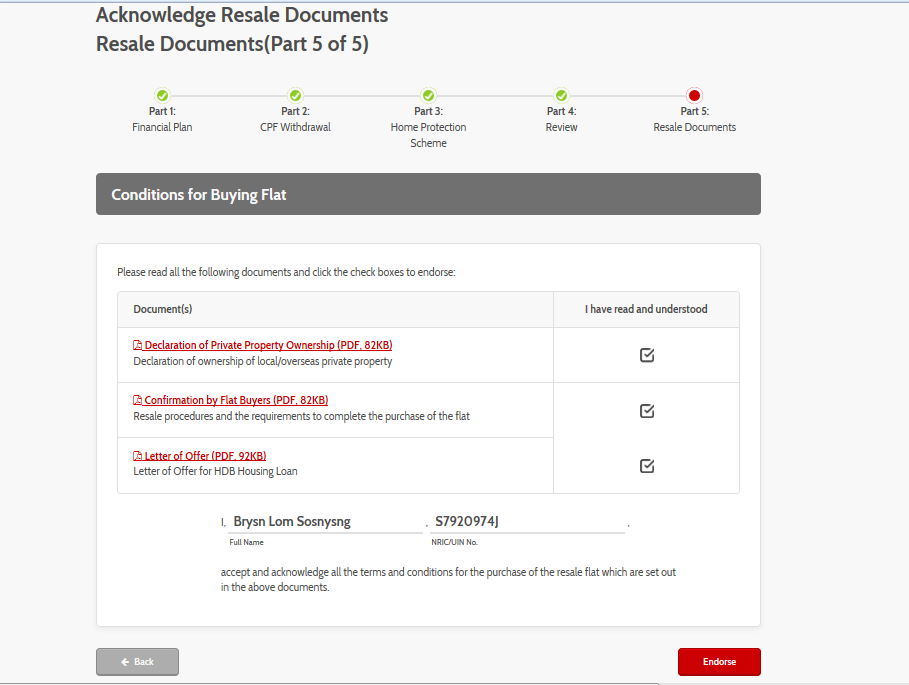

6. Acknowledge resale documents

HDB will compute and prepare the documents for buyers and sellers to endorse in the HDB Resale Portal. Both parties must endorse the documents within 6 days.

7. Pay resale fee

Flat buyers and sellers are required to pay online for the legal and stamp fees using the HDB Resale Portal.

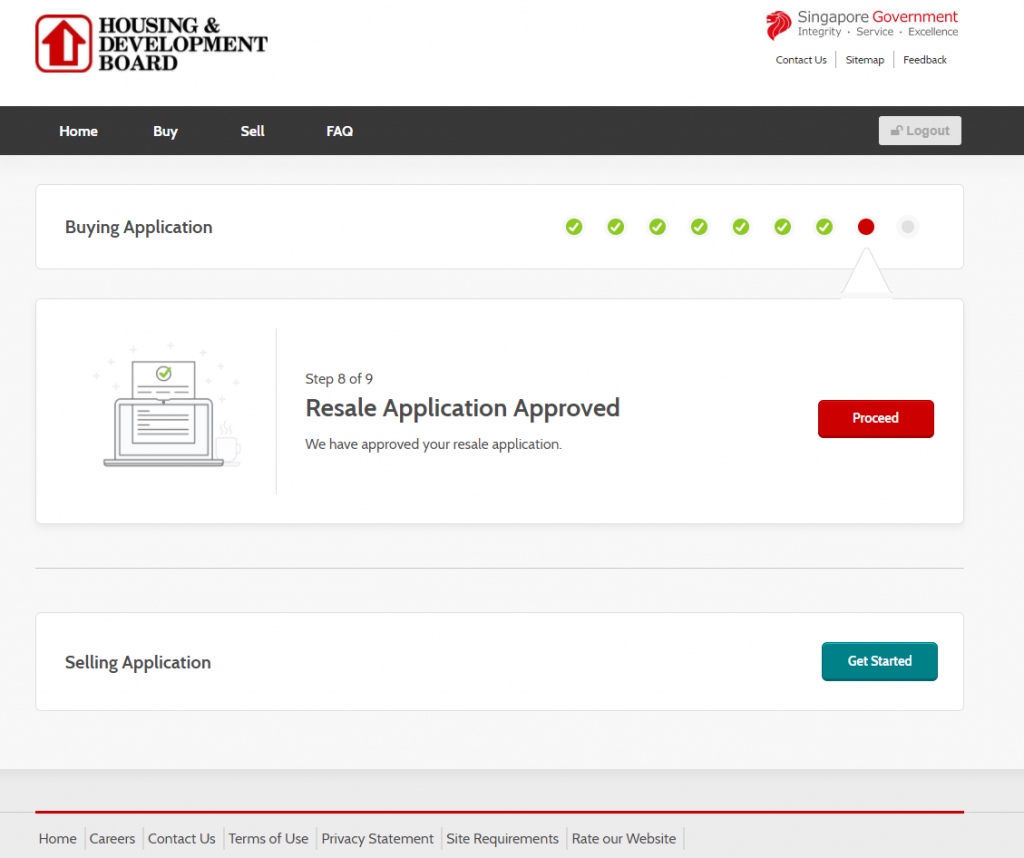

8. Wait for HDB’s approval

HDB will inform flat buyers and sellers once the application has been approved. The approval letter will be available on the HDB Resale Portal.

9. Attend completion appointment

Flats buyers and sellers must attend the Completion Appointment at HDB Hub to complete the resale transaction.

In summary, here are the steps for flat buyers and sellers:

Buying a flat is a huge financial commitment (you already know that!) and getting a second flat is no easier. There are many things to consider, so read on to make sure you have everything covered before putting your money down for your second home.

Computing your estimated sale proceeds

Do you know how much proceeds you might receive from the sale of your existing flat? As the cash proceeds will form part of your budget for your next flat, having a realistic estimate is crucial to helping you calculate the amount you can afford to spend. Simple math!

With information such as your outstanding mortgage loan, CPF funds used including interest, resale levy (if applicable), and some of the other payments due, you can use HDB’s Sale Proceeds Calculator to get a ballpark estimate of the cash proceeds from the sale of your flat!

Resale levy

You do not have to worry about the resale levy, if you plan on getting a resale flat on the open market next.

The resale levy applies to those who plan to buy a new flat from HDB, but have previously received some form of subsidy for their first flat – be it through the purchase of a flat from HDB, or a resale flat with the CPF housing grants.

As new HDB flats are sold at a subsidised price, the resale levy is put in place to ensure that there is a fair allocation of public housing subsidies between first-timers and second-timers.

Grants available

Second-timer home buyers can also be eligible for housing grants! If you are buying a resale flat that is within 4 km of where your parents/ child currently stay, you may be eligible to apply for the Proximity Housing Grant, which aims to help more families live close to each other for mutual care and support.

If you are intending to take a second HDB loan, do note that your loan amount will factor in your CPF and cash proceeds from the sale of your flat. This is to ensure that you do not over-borrow!

The commercial interest rate will be applied to your HDB housing loan if you plan to sell your current flat only after buying your next flat. The interest rate will be converted to the concessionary rate only after you have sold your current flat, and used the proceeds to repay your housing loan.

Contra Facility

Want to sell your existing HDB flat and buy another flat at the same time? Consider applying for the Contra Facility, which allows you to use the cash and CPF proceeds from the sale of your existing flat to purchase your next flat, concurrently.

The Contra Facility can help you reduce the cash outlay needed for your next flat, the mortgage loan amount needed and the subsequent monthly repayments. If you are buying a new flat, you can collect the keys to your new flat and renovate it, while selling your existing flat!

We hope this article has made financial planning for your second HDB flat less daunting. Follow us on Facebook for more useful information on buying a HDB flat and HDB living.

The post ‘My Resale Journey From West to East’ appeared first on the MoneySmart blog

This article was updated on 25 May 2021.

Conversations around public housing usually revolve around affordability, value, and financing. Beyond the dollars and cents, it’s hard to get a tangible sense of what owning a flat means to people, and the significance of having a home to call their own.

We spoke to different homeowners, specifically those who had bought resale flats, to get their thoughts about their home and flat buying journey. In the first of our 3-part series, we speak to Mr Ismail, who has lived on both sides of the island.

About The Flat

Owner: Mr Ismail bin Hamid, 41, Married with 4 kids

Location

Tampines

Flat Price

$410,000 (after $20,000 Proximity Housing Grant)

Year of Purchase

2018

Flat Type & Size

4-room flat/ 104 sqm

Remaining Length of Lease

63 years (as of Apr 2019)

Monthly mortgage amount & loan tenure

Nil (fully paid after selling previous flat)

Monthly mortgage amount & loan tenure

About $38,000

MoneySmart (MS): Mr Ismail, this is an amazing looking house. Tell us a little bit about why you chose to buy a flat here.

Mr Ismail: Tampines has been my home for the past 7 years. This flat is located 2 blocks away from where I grew up in, so this is a neighbourhood I am very familiar with. In fact, one of my primary school classmates still lives in the next block with his own family!

When I was growing up, there was only Bedok Interchange. There was no Tampines Interchange, and the Downtown Line certainly didn’t exist at that time, so you can imagine that getting around was very different from how it is now.

MS: Tell us a bit about your housing journey.

Mr Ismail: After I got married, my wife and I moved to Bukit Batok, which was near her family. It was a very different area from where I grew up, so that was something new. We then moved to a resale flat in Bukit Panjang. With convenience and proximity to family being a key consideration, we decided not to wait for a suitable BTO flat. At that time, the only available BTO flats were in Sengkang and Punggol, so we chose to buy a resale flat.

Due to family circumstances, we eventually moved back to the East, a few streets away from where we are currently staying now.

MoneySmart Tip: Interested flat buyers can get information on upcoming BTO projects 3 months before sales exercises for better planning. In the meantime, you can visit HDB InfoWEB for details on the upcoming BTO sales exercise.

MS: We also understand that you moved from a 5-room to a 4-room flat?

Mr Ismail: We felt that it was a much better idea to move to a 4-room flat because there was a lot of unused space in our previous 5-room flat. Even though we have four kids (aged 12, 9, 8, and 3), we felt that this current place suits our needs perfectly.

As you can see, the amenities around this place are great for our kids. We also considered the fact that there was a park that was very accessible and our kids wouldn’t have to cross any major roads to get there.

At this point, Mr Ismail’s wife also chimes in, highlighting the fact that the 4-room flat is much easier to clean than their previous home. They also managed to completely pay off their housing loan after moving, but more on that later.

MS: Tell us about your home buying process. Did you engage an agent or do it on your own?

Mr Ismail: We decided to go with an agent, and the reason was that our housing agent was also my friend from reservist! He also helped us to sell our previous home. I would say when it comes to engaging an agent, it definitely helps to have someone who knows his stuff.

It was an easy decision to buy our current home because we knew what we wanted, and the opportunity presented itself. I would say our only regret is that we missed out on a flat that is near the newly built Our Tampines Hub. There was nothing there at that point in time and we had no idea they were going to build an integrated community hub there!

MoneySmart Tip: Besides going through an agent, buyers and sellers can use the HDB Resale Portal to perform their own resale transactions. The portal will guide you on the buying journey and help you track the progress of your transaction. The resale process takes approximately 8 weeks to complete from the date of HDB’s acceptance of the resale application.

MS: How did you plan your finances? What were your goals or considerations?

Mr Ismail: For me, I chose to pay off this flat fully. I know it might seem a little “old school”, but we believe that we should just keep our money in CPF and use that for retirement.

For our previous homes, we also chose to take a loan from HDB. My wife works in a bank, so we understand that there are benefits and risks to taking a bank loan, and we ultimately settled on getting an HDB loan. Now that we’ve paid off this flat, we don’t have to worry about a mortgage anymore, and we can focus on planning for retirement.

MS: And what sort of grants did you get for your home?

Mr Ismail: At the start when we got our first place after we got married, we were eligible for a grant for first time buyers, and of course we were aware that we could get $20,000 in Proximity Housing Grant for this flat as we were moving near my parents.

MS: Your home looks really nice and comfortable. Did you have to renovate it a lot, and how much did you spend?

Mr Ismail: We spent about $38,000 on our renovations. We did have to do quite a bit of work, which included your regular maintenance such as repainting the place and redoing the flooring and doors. The main issue with the place was that the wiring wasn’t done properly so we had to redo everything because they were crossed all over the place. The kitchen was also rather old so we gave it a refresh.

MS: Can you share with us some thoughts around owning a home in Singapore?

Mr Ismail: For me, I never intended to buy a flat to profit from it. I plan to stay here with my wife till we pass on. Some people talk about leases expiring, but my perspective is that you are probably not even going to be alive when that lease expires, so why worry about it? As for my children, they will probably move out and buy a flat of their own, so I am not too worried about what happens with the lease.

There are many things that might change in the future which you have no idea about, so you plan for what you can. Other than that, I feel blessed to be able to say that I own a home, which is more than what many other people in other developed countries can say.

MS: Any other words of advice for homebuyers?

Mr Ismail: Go with what you are comfortable with. At the end of the day, you can overthink, but when you step into a neighbourhood, just ask yourself whether you feel like you belong there . Are you comfortable with the place and its surroundings? Is it a place you feel your children can grow up in?

Convenience is another factor. It might be more important for you to be near a supermarket than an MRT station. Whatever the case, understanding your needs is important. Small inconveniences can become a big deal over the course of a few years.