Buying an HDB Flat? Here’s How to Decide Between HDB Loans and Bank Loans

HDB loans or bank loans? That’s probably what many first-time home owners are wondering, after deciding that they’re ready to take the plunge and buy an HDB flat. We’re here to break down the differences.

HDB Loan vs. Bank Loans:

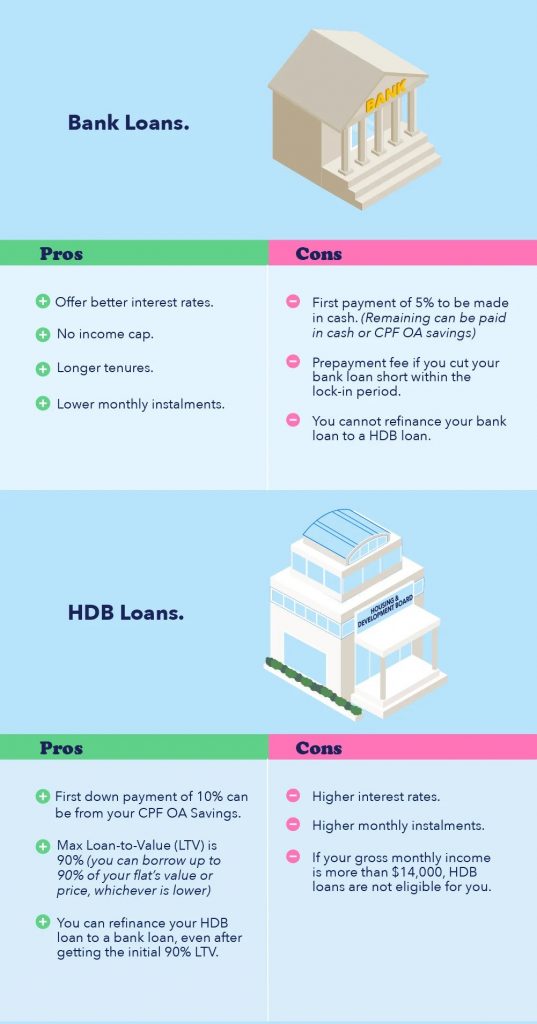

- HDB loans require a smaller cash outlay

- Interest rates of bank loans are highly variable, whereas HDB loan rates have not changed much as they are pegged to the CPF rate

- Bank loans are currently more affordable than HDB loans, at the prevailing interest rate

- You can switch from an HDB loan to a bank loan, but not the other way around

Downpayment

A huge advantage of taking an HDB loan is that you are able to fork out a smaller amount of cash for your downpayment.

The maximum loan-to-value (LTV) ratio for HDB loans is 90%. So you can borrow up to 90% of your flat’s value or price, whichever is lower. For the remaining downpayment of 10%, you can use a combination of cash or your CPF OA savings.

On the other hand, the maximum LTV ratio for bank loans is 75%. This translates to an extra 15% in downpayment as compared to an HDB loan. What’s more, 5% must be paid in cash for the downpayment, with the remaining 20% to be paid in cash and/or CPF OA savings.

Interest rates and monthly instalments

The interest rate for HDB loans is fixed at 0.1% above the prevailing CPF rate. With the current CPF rate at 2.5%, the interest rate for HDB loans is 2.6% per annum.

In contrast, depending on market conditions, bank loan rates are more variable. This applies to loan packages that are pegged to fixed interest rates as well. After a lock-in period of 2 to 5 years, these so-called fixed rate home loans follow a floating rate.

So technically, there is no perpetual fixed rate home loan in Singapore.

Bank loan interest rates are mainly determined by these three floating rate benchmarks:

- Singapore Interbank Offered Rate (SIBOR), which will be replaced by Singapore Overnight Rate Average (SORA) by the end of 2024

- Board Rate (BR)

- Fixed Deposit Home Rate (FHR)

Whether you’re taking a SIBOR, SORA, BR or FHR home loan, the interest rate is the prevailing rate plus the bank’s spread.

So “3M SIBOR + 0.75” means the interest rate is the prevailing three-month SIBOR rate, plus 0.75% charged by the bank (the spread). Every three months, when the SIBOR rate changes, the interest rate will be changed to match the new rate.

This means that if you have a 1M SIBOR rate home loan, the loan repayment amount will change every month. If you have a 3M SIBOR rate home loan, the loan repayment amount will change every 3 months, and so forth.

Likewise, “BR + 0.5” means that the interest rate is the current board rate plus the bank’s spread of 0.5%. The difference is that the board rate is set entirely by the bank.

An FHR home loan is pegged to the bank’s fixed deposit rates, so it’s pretty similar to a BR home loan as the rate is essentially determined by the bank.

Why are bank loans more affordable?

The historical interest rate for bank home loans is between 3% to 4% per annum. This is more expensive than HDB loans.

However, due to the Global Financial Crisis in 2008, bank interest rates have remained low for around 10 years. Currently, bank loans are around 1.8% per annum, as opposed to HDB’s 2.6%.

The lower interest rates translate to lower monthly instalments

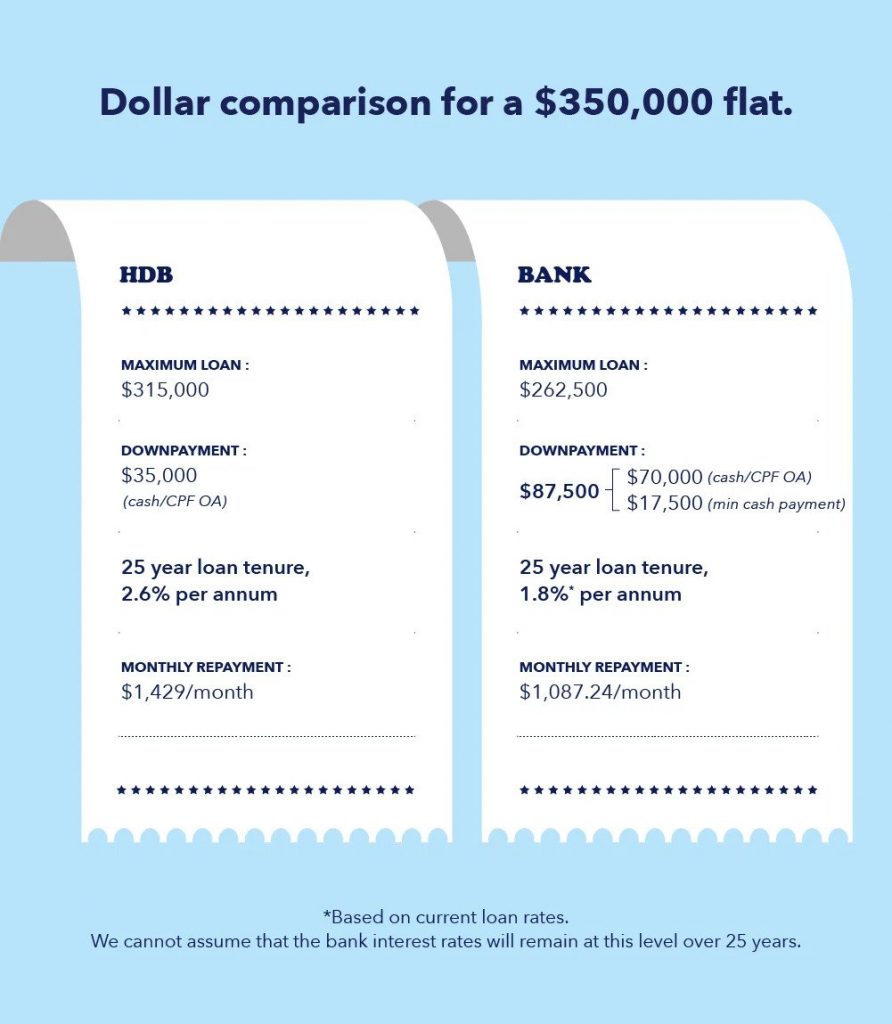

If the flat is priced at $350,000, the maximum loan quantum for an HDB loan, based on an LTV of 90%, is S$315,000 and downpayment is S$35,000. If you’re taking a 25-year loan tenure, the monthly repayments will be $1,429.

In contrast, if you’re taking a bank loan with an LTV of 75%, the loan quantum will be S$262,500. And the downpayment will be S$87,500.

On a 25-year loan tenure, assuming an interest rate of 1.8% per annum*, the monthly repayments will be cheaper at S$1,087.24.

*This is based on current, typical loan rates. We cannot assume that the bank interest rates will remain at this level over 25 years.

Income cap

Whether you’re buying a BTO or resale flat, HDB loans come with stricter eligibility criteria, including income ceiling. If your gross monthly household income is more than S$14,000, you won’t be eligible for an HDB loan.

Conversely, bank loans don’t have an income cap, so it’s suitable for those with a higher income.

Tenure

HDB loans are capped at 25 years, while bank loans for HDB flats have a longer maximum loan tenure of 30 years. (However, the LTV will be reduced to 55% if the loan tenure exceeds 25 years.)

Having a longer tenure can be a good thing, as it allows you to lower your monthly repayments and spread it out. On the other hand, it also means paying a higher interest.

Refinancing

You can refinance your HDB loan into a bank loan (subject to the bank’s approval), even after getting the initial 90% LTV. By taking a home loan with a lower interest rate, you can reduce your monthly repayments.

However, you can’t refinance your bank loan into an HDB loan. What you can do is reprice it with the same bank or switch to another bank to refinance it.

Early repayment

Another good thing about HDB loans is that they don’t have an early repayment penalty. So you can pay it off earlier, such as through partial capital repayment to reduce your financial commitments.

But if you’re taking a bank loan, it’s better not to pay it off early. The bank will charge a prepayment fee if you cut short your bank loan within the lock-in period, since they earn from the interest.

Which is better?

If you’re on a tight budget, HDB loan should be considered first, as the cash outlay is smaller. The fixed interest rate also gives you a better idea of how much you’re paying monthly for your home loan. If you find the interest is too high, you can always refinance from an HDB loan to a bank loan later, but not the other way around.

If you intend to upgrade fast (e.g. sell the flat and buy a new home, such as a private property, as soon as you can), you may want to consider a bank loan, or quickly refinance into a bank loan from an HDB loan. This could reduce monthly repayments, and minimise the interest eating into any resale gains.

Speaking to a mortgage broker can also help you better understand more about suitable home loans.

Looking to embark on your home ownership journey? From the types of CPF housing grants to a guide on using the HDB Flat Portal to purchase your HDB flat, read here to find out more!

This article was adapted from 99.co, Singapore’s fastest growing property platform for information like resale HDBs for sale and rent in Singapore. Check out the original article here.

Source: mynicehome.gov.sg